Our March update note went through the H120 results, which were provisionally released as a trading update, before formal publication in April due to the disruption to markets as the COVID-19 lockdowns came into force. These showed a robust set of figures, with sales of the group’s data products well ahead: 27% on an underlying basis. The results from Data Services, principally Omnibus, were less impressive, with revenue up 3% (7% underlying). This period included difficult trading in the Nordics business, a tougher comparison in Asia-Pacific (there was an election benefit in the prior period) and a more difficult German market.

Continued growth in the proportion of higher-margin project work in Custom Research helped propel adjusted operating profit to £8.0m, representing an operating margin of 23.6% in H120 from 22.0% in the comparative period.

Exhibit 10: Long-term growth record and forecasts

|

|

Source: YouGov accounts, Edison Investment Research

|

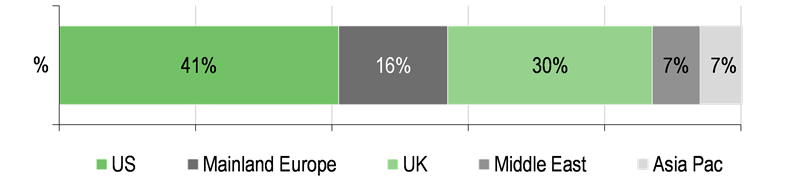

The group continued to expand in the US (47% of H1 operating profit before central costs), where interest in the presidential elections should build over H220 and H121.

At the time of the publication in March, we applied a 10% revenue reduction for the remainder of the forecast year. The only further adjustments we have made at this point are to reflect the implementation of IFRS 16, which we omitted to do at the time and which boosts EBITDA but makes little difference lower down the income statement.

YouGov has an enviable long-term record of revenue and EBITDA growth, which has been predominantly achieved through organic means. From FY10–FY19, revenue has more than trebled (a CAGR of 13.4%) and operating profit margin increased from 8.9% to 13.5% as the business has scaled up, investing in product and improving operational efficiency. For H120, the operating margin was 14.8% from 12.6% in H119.

With multi-year syndicated Plan & Track subscriptions, dashboards incorporated into client workflows and a growing proportion of Custom Research being in large-scale tracking studies, the level of recurring and repeatable business continues to build (although this is not a proportion disclosed as such). At the half-year results, management referred to a newly-signed strategic multi-year contract with a major German-based financial institution – obviously significant enough to warrant a specific mention.

Exhibit 11: Revenue progression

|

|

Source: Company accounts, Edison Investment Research

|

In the short term, margin growth is constrained by the need to invest in technology and panel but also in sales and marketing. The new five-year plan, though, includes a target to double adjusted operating margin. There are several keys to driving the operating margins forward, but at the core, it is all about engineering the data and integrating and delivering it through the universal platform outlined above. This is particularly true of the custom business, increasingly using the syndicated data already available within the YouGov Cube. Having one analytics system, Crunch, also greatly increases the efficiency in the system. The emphasis now is on managing the client relationships more effectively, with global key account management.

We have now restated our FY18 and FY19 numbers for the implementation of IFRS 16, which adds £3.1m to EBITDA. The adjustment to normalised PBT is just £0.1m.

FY20e, FY21e estimates contingent on the impact of COVID-19

The only change to our FY20 numbers at this stage reflects the IFRS 16 application. We made a cautionary 10% reduction to our H220 revenue estimate on publication of the interim results. We have now published our provisional FY21e estimates, which assume a relatively cautious 8% top-line progression. We have built in further improvement in adjusted operating profit margin from 13.9% to 16.0% in FY21e as the benefits of the Centres of Excellence and the increased added value within Custom Research take effect.

As indicated within the sensitivities section above, we can see that the pandemic is likely to have been both positive and negative repercussions. On the plus side, the need for quick and reliable gauging of public mood and attitudes will have stimulated some demand. However, some commercial clients may have rescheduled, reconfigured or postponed work as they reappraised the scale and timing of their marketing spend. New business may have been more difficult to procure and payment terms may have extended.

YouGov has a particularly strong record of cash conversion. The group quotes its cash conversion against adjusted EBITDA, so using the figures restated for IFRS 16 implementation for FY19 and FY18, this gives a conversion rate of 111% and 113% respectively. At the half year, the figure was 93%, up from 69% in H119.

The growing level of subscription-based income is also increasing the deferred element of those annual subscriptions, benefiting the working capital position. The group continues to invest in its software and in its panel. FY19 was a higher year for capital expenditure, with £12.2m spent mostly on software and panel. £7.7m was spent in H120, split £4.2m on panel investment and £3.5m on software. For the full year, we have pencilled in a spend of £15.0m, with £16.5m for FY21e. Ensuring the panel is an appropriate size and appropriate in its constituents is crucial to be able to deliver the timely and robust data in each territory, so there is a need for higher levels of spend when moving into new geographies, or ahead of specific events, such as the US presidential elections.

Strategic acquisitions have also been on the agenda. To date, these have incurred modest upfront costs. SMG Insight, now YouGov Sport, had performed so well that management accelerated the completion. £7.4m of deferred consideration was paid in H120. There is now an expected total of £13.2m of deferred consideration payable in respect of future earn-outs attached to acquisitions. We have £8.6m identified for payments in our FY21e cash flow.

In normal years, the group pays only a final dividend, in December. A decision on a payment for FY20 is therefore still some way off and the world may look very different by then. Given the strength of the balance sheet, we are assuming that there will be a dividend, but that it will be at the same level as FY19 (4.0p), rising to 5.0p in FY21e.

As at the half year, the balance sheet had £27.2m of cash (there is no debt), down from £37.9m at the year end. During those six months, the group spent £7.4m on deferred consideration for acquisitions, the £3.5m of software and £4.2m on building panel referred to above.

Under IFRS 16, the group’s lease liabilities are now shown on the face of the balance sheet. These totalled £9.8m at end January, of which £2.5m were short term and £7.3m were longer term. Even if these are considered as debt, the net cash position remained very healthy at £17.4m

Our modelling indicates a cash balance of around £33.9m at end FY20e (a net £24.1m on an IFRS 16 basis), and around £30.9m for the following year post the acquisition spend of £8.6m and £16.5m of capex that we have pencilled in. We do emphasise, though, that there is a far higher degree of uncertainty over our projections than normal.

Exhibit 12: Financial summary

|

£'000s |

|

2018 |

2019 |

2020e |

2021e |

Year end 31 July |

|

|

IFRS |

IFRS |

IFRS |

IFRS |

PROFIT & LOSS |

|

|

|

|

|

|

Revenue |

|

|

116,559 |

136,487 |

147,000 |

159,000 |

Cost of Sales |

|

|

(21,495) |

(24,206) |

(24,748) |

(27,098) |

Gross Profit |

|

|

95,064 |

112,281 |

122,251 |

131,903 |

EBITDA |

|

|

20,907 |

31,698 |

32,041 |

36,120 |

Operating Profit (before amort. and except.) |

|

|

12,650 |

18,492 |

21,657 |

25,511 |

Intangible Amortisation |

|

|

(7,026) |

(8,809) |

(8,809) |

(8,809) |

Share based payments |

|

|

(3,571) |

(2,401) |

(1,250) |

(1,250) |

Exceptionals |

|

|

(892) |

1,529 |

0 |

0 |

Other |

|

|

66 |

200 |

0 |

0 |

Operating Profit |

|

|

11,824 |

20,221 |

21,657 |

25,511 |

Net Interest |

|

|

(51) |

(665) |

154 |

137 |

Profit Before Tax (norm) |

|

|

16,302 |

20,428 |

23,062 |

26,898 |

Profit Before Tax (FRS 3) |

|

|

11,773 |

19,356 |

21,812 |

25,648 |

Tax |

|

|

(3,615) |

(5,086) |

(5,638) |

(6,657) |

Profit After Tax (norm) |

|

|

12,687 |

15,342 |

17,424 |

20,241 |

Profit After Tax (FRS 3) |

|

|

8,158 |

14,270 |

14,924 |

17,741 |

|

|

|

|

|

|

|

Average Number of Shares Outstanding (m) |

|

|

105.4 |

105.4 |

107.1 |

108.4 |

EPS - normalised (p) |

|

|

10.8 |

13.8 |

15.4 |

17.2 |

EPS - FRS 3 (p) |

|

|

7.7 |

14.1 |

13.9 |

16.4 |

Dividend per share (p) |

|

|

3.0 |

4.0 |

4.0 |

5.0 |

|

|

|

|

|

|

|

Gross Margin (%) |

|

|

81.6 |

82.3 |

83.2 |

83.0 |

EBITDA Margin (%) |

|

|

17.9 |

23.2 |

21.8 |

22.7 |

Operating Margin (before GW and except) (%) |

|

|

10.9 |

13.5 |

14.7 |

16.0 |

|

|

|

|

|

|

|

BALANCE SHEET |

|

|

|

|

|

|

Fixed Assets |

|

|

78,019 |

108,534 |

121,683 |

120,380 |

Intangible Assets |

|

|

65,357 |

82,374 |

90,013 |

90,204 |

Tangible Assets |

|

|

12,471 |

26,160 |

31,670 |

30,176 |

Investments |

|

|

191 |

0 |

0 |

0 |

Current Assets |

|

|

66,735 |

72,581 |

71,121 |

71,123 |

Stocks |

|

|

0 |

0 |

0 |

0 |

Debtors |

|

|

34,672 |

33,726 |

36,324 |

39,289 |

Cash |

|

|

30,621 |

37,925 |

33,867 |

30,904 |

Current Liabilities |

|

|

(41,445) |

(48,504) |

(48,797) |

(52,318) |

Creditors |

|

|

(41,445) |

(48,504) |

(48,797) |

(52,318) |

Short term borrowings |

|

|

0 |

0 |

0 |

0 |

Long Term Liabilities |

|

|

(11,238) |

(14,060) |

(14,060) |

(14,060) |

Long term borrowings |

|

|

0 |

0 |

0 |

0 |

Other long term liabilities |

|

|

(11,238) |

(14,060) |

(14,060) |

(14,060) |

Net Assets |

|

|

92,071 |

118,551 |

129,947 |

125,125 |

|

|

|

|

|

|

|

CASH FLOW |

|

|

|

|

|

|

Operating Cash Flow |

|

|

23,617 |

35,230 |

27,890 |

32,019 |

Net Interest |

|

|

22 |

183 |

154 |

137 |

Tax |

|

|

(5,501) |

(4,520) |

(3,651) |

(4,936) |

Capex |

|

|

(8,181) |

(12,166) |

(15,000) |

(16,500) |

Acquisitions/disposals |

|

|

(885) |

(6,583) |

(7,448) |

(8,600) |

Financing |

|

|

259 |

(3,652) |

(1,500) |

0 |

Dividends |

|

|

(2,106) |

(3,327) |

(4,504) |

(5,084) |

Net Cash Flow |

|

|

7,225 |

5,165 |

(4,058) |

(2,964) |

Opening net debt/(cash) |

|

|

(23,219) |

(30,621) |

(37,925) |

(33,867) |

HP finance leases initiated |

|

|

0 |

0 |

0 |

0 |

Other |

|

|

177 |

2,138 |

0 |

0 |

Closing net debt/(cash) |

|

|

(30,621) |

(37,925) |

(33,867) |

(30,903) |

Source: Company accounts, Edison Investment Research. Note: FY19 restated for IFRS16, FY18 and FY19 restated for change in treatment of amortisation and share-based payments.

Contact details |

Revenue by geography |

50 Featherstone Street

London

EC1Y 8RT

UK

+44 (0)20 7012 6000

www.yougov.co.uk |

|

Contact details |

50 Featherstone Street

London

EC1Y 8RT

UK

+44 (0)20 7012 6000

www.yougov.co.uk |

Revenue by geography |

|

Management team |

|

Chairman: Roger Parry |

CEO: Stephan Shakespeare |

Appointed as chair of YouGov in 2007, Roger is chair of Oxford Metrics and an NED of Uber UK. He was previously chair of Future Publishing, Johnston Press and Shakespeare’s Globe Trust, a consultant with McKinsey, CEO of More Group and CEO of Clear Channel Intl. Roger is a Visiting Fellow of Oxford University. |

Stephan co-founded YouGov in 2000. One of the pioneers of internet research, he has been the driving force behind YouGov’s innovation-led strategy. He was chair of the Data Strategy Board for the Department for Business, Innovation and Skills 2012–13 and led the Shakespeare Review of Public Sector Information. He is a commissioner for the Social Metrics Commission, and an Affiliated Researcher at the Bennett Institute for Public Policy, Cambridge University, where his work is focused on the public dimensions of globalisation and tracking attitudes to public policy. |

CFO: Alex McIntosh |

COO: Sundip Chahal |

Alex has been with YouGov since 2007, initially as corporate finance manager within the finance team, focusing on planning, budgeting and corporate development. He became chief strategy officer in 2011 and played a leading role in the development of YouGov’s strategic plans and data product developments. Alex also held the role of CEO of YouGov’s UK business from 2015 to 2016. He previously worked in corporate finance advising a wide range of companies and first worked with YouGov in 2005 while at Grant Thornton, assisting with the group’s IPO on AIM. |

Sunny has been with YouGov since 2005, becoming COO in 2014. He initially joined YouGov’s UK business as BrandIndex Sales Director, becoming MD of Data Products in 2008. In 2009 he was appointed as COO of MENA, relocating to Dubai to oversee the expansion of YouGov’s core online services across the Middle East, North Africa and Asia. In 2010 he was promoted to CEO of YouGov MENA. Sunny previously worked at Ipsos and Research International. |

Management team |

Chairman: Roger Parry |

Appointed as chair of YouGov in 2007, Roger is chair of Oxford Metrics and an NED of Uber UK. He was previously chair of Future Publishing, Johnston Press and Shakespeare’s Globe Trust, a consultant with McKinsey, CEO of More Group and CEO of Clear Channel Intl. Roger is a Visiting Fellow of Oxford University. |

CEO: Stephan Shakespeare |

Stephan co-founded YouGov in 2000. One of the pioneers of internet research, he has been the driving force behind YouGov’s innovation-led strategy. He was chair of the Data Strategy Board for the Department for Business, Innovation and Skills 2012–13 and led the Shakespeare Review of Public Sector Information. He is a commissioner for the Social Metrics Commission, and an Affiliated Researcher at the Bennett Institute for Public Policy, Cambridge University, where his work is focused on the public dimensions of globalisation and tracking attitudes to public policy. |

CFO: Alex McIntosh |

Alex has been with YouGov since 2007, initially as corporate finance manager within the finance team, focusing on planning, budgeting and corporate development. He became chief strategy officer in 2011 and played a leading role in the development of YouGov’s strategic plans and data product developments. Alex also held the role of CEO of YouGov’s UK business from 2015 to 2016. He previously worked in corporate finance advising a wide range of companies and first worked with YouGov in 2005 while at Grant Thornton, assisting with the group’s IPO on AIM. |

COO: Sundip Chahal |

Sunny has been with YouGov since 2005, becoming COO in 2014. He initially joined YouGov’s UK business as BrandIndex Sales Director, becoming MD of Data Products in 2008. In 2009 he was appointed as COO of MENA, relocating to Dubai to oversee the expansion of YouGov’s core online services across the Middle East, North Africa and Asia. In 2010 he was promoted to CEO of YouGov MENA. Sunny previously worked at Ipsos and Research International. |

Principal shareholders |

(%) |

LionTrust Asset Managers |

14.95 |

BlackRock |

9.87 |

Aberdeen Standard |

8.49 |

Octopus Inv |

7.98 |

T Rowe Price Global Investors |

7.13 |

Stephan & Rosamunde Shakespeare |

6.89 |

Kabouter Management |

5.14 |

Investec Wealth & Inv |

4.95 |

Charles Stanley |

4.36 |

Baillie Gifford |

3.69 |

|

|

General disclaimer and copyright This report has been commissioned by YouGov and prepared and issued by Edison, in consideration of a fee payable by YouGov. Edison Investment Research standard fees are £49,500 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2020 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument. New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

General disclaimer and copyright This report has been commissioned by YouGov and prepared and issued by Edison, in consideration of a fee payable by YouGov. Edison Investment Research standard fees are £49,500 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2020 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument. New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|