bp plc is a client of Edison Group. Edison Group produced and distributed this content. Edison Group does not hold any position in bp plc.

In our initial analysis (which you can find here), we established that bp’s ‘fundamental strategic update’ is predicated on financial discipline. The headline targets are ambitious and, if achieved, will create growth in free cash flow.

But is the underlying plan to deliver credible?

This second analysis interrogates the core mechanics of management’s plan. We assess whether the company’s cost-cutting initiatives are plausible, how bp expects to meet the debt reduction targets and what is implied by having a focus on capital efficiency. Finally, we put these plans in the context of the company’s current market valuation.

Interrogating the cost savings

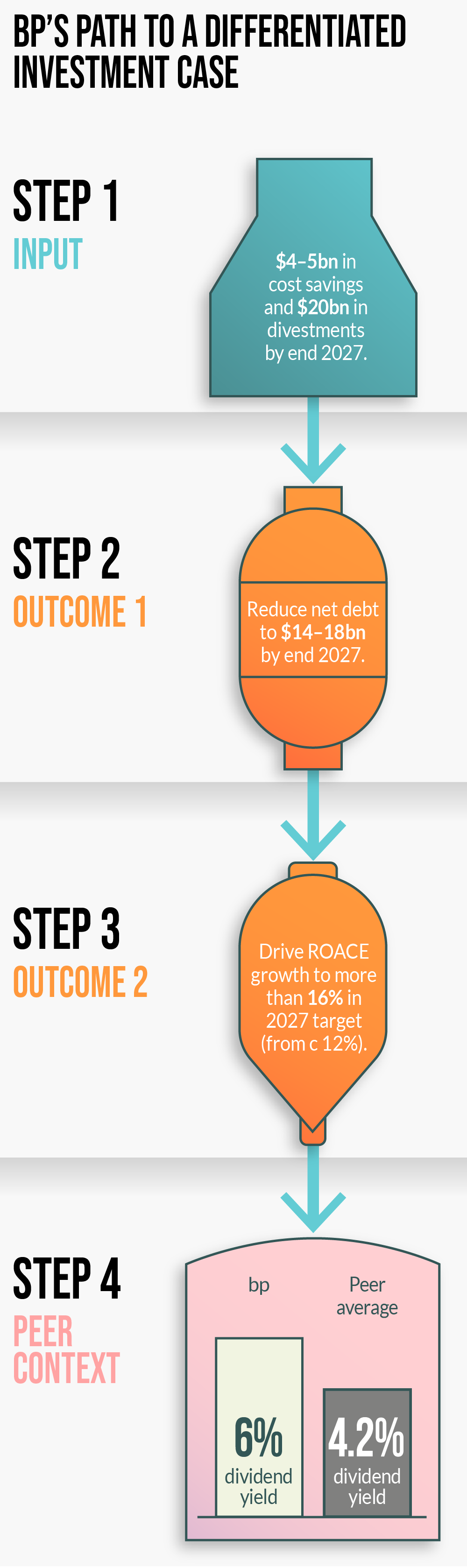

Management has put a program in place which is intended to deliver $4–5bn in structural cost reductions by the end of 2027, relative to a 2023 baseline. This is arguably a key self-help component of bp’s investment case, as it is less dependent on commodity prices than internal targets. The credibility of this ambitious figure rests on the successful execution of several complex, multi-year initiatives.

According to bp’s publicly available plans, a substantial portion of these savings are targeted in the downstream business, including c $1.5bn from the Customers division and more than $500m from the Products division. Within the Customers division, the plans detail three main savings levers:

- Operating model: streamlining the organization by reducing interfaces, eliminating duplication and moving roles to business and technology hubs.

- Digital and automation: driving frontline efficiencies through the deployment of common operating systems and automation in stores.

- Supply chain: materially consolidating the supplier base to standardize processes and drive economies of scale. While the company reported that it had already delivered $1.7bn in savings as of mid-2025, investors will likely monitor ongoing progress closely, as large-scale cost reduction programs are notoriously complex to execute.

De-risking via debt reduction

The cost-saving program is a critical component of a broader strategy to strengthen the balance sheet. bp also has a primary target to reduce net debt to a range of $14–18bn by end 2027, down from $26.0bn in mid-2025.

This planned deleveraging is designed to be achieved through a combination of cost savings and a significant $20bn divestment program.

This signals an intent to achieve an acceleration of high grading its portfolio of assets. A stronger balance sheet is a critical de-risking factor for management’s investment case, providing a greater safety buffer for the dividend and increasing resilience to commodity price volatility.

While it is Edison’s opinion that the plan stacks up in theory, it is worth remembering that unlocking the value is not a done deal – the timing and ultimate value received from large-scale divestments are subject to market conditions and successful negotiations.

A new focus: Capital efficiency

The bp board’s intentions on cost and debt are part of a wider strategic direction towards concentrating on capital efficiency, a shift that appears to be a reflection of the company’s stated goal of being ‘very efficient with your capital investment – not chasing too many projects’.

The key metric for measuring this efficiency is return on average capital employed (ROACE). bp is targeting a group-wide ROACE of more than 16% in 2027, a significant increase from the c 12% level in 2024.

Achieving this requires a challenging dual mandate: the numerator (earnings) must grow, while the denominator (capital employed) is managed with discipline. It requires a clear management focus on not just growing the business, but on growing the profitability of every dollar invested.

The differentiator: A question of valuation

This focus on the use of capital is particularly relevant given the company’s valuation relative to its peers. This presents a classic value-investing question: Is the current valuation discount a reflection of past underperformance that the new plan will correct, or does it reflect the market’s skepticism about the company’s ability to execute its ambitious turnaround?

As of 2 September 2025, our analysis concluded that bp currently trades at a discount to the sector average. Furthermore, its dividend yield of approximately 6% (based on consensus estimates for FY26) is higher than the peer average. A bull case for the stock assumes that consistent delivery against its new financial framework will be the catalyst for a potential re-rating of the stock over time.

In conclusion

bp’s strategy is heavily reliant on its own heavy lifting, a self-help story of internal improvement. The plan to deliver $4–5bn in cost savings is a central pillar, providing the means for both debt reduction and a targeted increase in capital efficiency, as measured by ROACE. This disciplined approach appears, on paper, to be achievable. For investors, the combination of a discounted valuation and a clear, metrics-driven plan for financial improvement presents the foundations to form a bullish investment case.

However, the plan’s credibility rests on execution. The targets are ambitious, and the market appears to have adopted a ‘wait-and-see’ approach. The ultimate question, which we will explore in our final analysis, is how this financial discipline is designed to translate into tangible shareholder returns and whether the early proof points are strong enough to build conviction.

To analyze bp’s dividend and buyback program in detail and review the key metrics on our investor scorecard, read our final report.

Forward-looking targets are based on current expectations and planning assumptions. Actual results may differ materially based on various factors including but not limited to commodity prices, operational performance, regulatory changes, and global economic conditions.

Shareholder distributions, including dividends and share buybacks, are subject to the discretion of the board and may vary based on factors including, but not limited to commodity prices, cash flow generation, balance sheet considerations, and general business conditions. Past distributions are not indicative of future distributions.