“Edison is the go-to for a new investor to get full understanding of the investment case and business. Edison’s distribution reaches investors that we want to connect with directly.”

Join us for investment knowledge across your choice of sectors and equities.

To continue reading, log in or create a free account below.

Close

Close

Close

Create An Account

If you have an account with us, please click the sign in button below.

UK housebuilders

Industrials

UK housebuilders

Depressed valuations imply upside potential

Companies mentioned in this report

Barratt Developments (BDEV.L) Bellway (BWY.L) Berkeley Group (BKG.L) Cairn Homes (CRN.L) Crest Nicholson (CRST.L) Empiric Student Property (ESP.L) Glenveagh Properties (GLV.L) Grainger (GRI.L) Henry Boot (BOOT.L) Inland Homes (INL.L)

Kier Group (KIE.L) MJ Gleeson (GLE.L) Morgan Sindall (MGNS.L) Persimmon (PSN.L) Redrow (RDW.L) Springfield Properties (SPR.L) Taylor Wimpey (TW.L) Unite Group (UTG.L) Vistry Group (VTY.L) Watkin Jones (WJG.L)

The mini-budget in September highlighted an already well-known problem: rising house prices have made traditional home ownership increasingly unaffordable and increasing interest rates will make it harder still. Affordability is still very stretched, but we believe interest rates may peak at lower levels than the rate curve suggests, which means the sector may not suffer as badly as the current low price-to-book ratios of housebuilders suggest and there is significant upside potential in share prices.

Affordability and interest cost issues abating

Rising salaries and modestly declining house prices should take some pressure off the elevated affordability ratios, implying a slightly more favourable housing market than was feared last autumn. Furthermore, inflation expectations have fallen and this is now firmly reflected in mortgage rates. With funding costs declining and the mortgage market remaining competitive, additional declines in mortgage rates are likely, further easing market pressures.

Removal of government support less of an issue

The government’s main house buyer support tool, Help to Buy, has been phased out despite its popularity with new buyers and housebuilders. In its place, several alternative schemes have sprung up that are more restrictive, as well as new support packages funded by housebuilders that are designed to aid buyers. These include discounts to selling prices, cash contributions and part-exchange schemes. Collectively, it would appear that the hole in the market left by the demise of Help to Buy is likely to have less of an effect than first feared, in our opinion.

Sector cost pressures beginning to ease

Labour and material costs have begun to ease as energy prices fall and demand weakens. Furthermore, the costs of introducing the government’s Future Homes Standard are likely to be absorbed by the housebuilder as the initiative becomes widely implemented. Other costs, such as the Residential Property Developer Tax and remediation for cladding issues, will be a drag. The industry has been aware of these costs for several years, which will be reflected in the value that housebuilders attach to land. It therefore follows that although margins and returns are likely to be hit in the short term, the sector should eventually revert to higher returns on equity, which will be reflected in higher share prices in the longer term.

Value to be recognised in the sector

The headwinds discussed above and the lack of consumer confidence are a real issue for the housebuilding sector despite the demand for housing far exceeding supply. That said, almost every housebuilder has suffered reduced demand in Q4, which is reflected in sales as well as in new buyer enquiries and housebuilders’ much-reduced activity in the land market. The extent that these issues are reflected in valuations remains in question. Our preferred measure in these kinds of markets is the price to book ratio as it is a fairer reflection of the underlying real value in a share price. Currently, every stock in our housebuilding universe is trading at a significant discount to book value and, on average, at levels rarely seen in the last 10 years. To us this implies an attractive entry point to the sector for investors searching for value.

Overview of the UK housing market

We believe that the low valuations ascribed to the housebuilding sector by the market reflect the potential for the housing market to be depressed for an extended period of time. However, underlying demand has not gone away and, although interest rates are higher and affordability is stretched, mortgage rates are now falling and higher wages and lower house prices are relieving some of the tension. With this in mind, housebuilders have universally witnessed some recovery in demand in the early weeks of 2023, implying material upside in share prices if a recovery can be sustained.

The UK population has risen every year since 1978 and is expected to rise every year for the next 30 years. To house greater numbers of people, the UK needs to increase its housing stock. In the last 15 years, the number of homes in the UK has risen by around three million. The government’s policy in general is supportive of this outcome, but has fallen short on targets for the sector to deliver 300,000 units per year. It can therefore be argued that the market is undersupplied, which implies underlying demand for the new dwellings built by the various suppliers of additional volume. It also implies that house prices will trend upwards as demand outstrips supply. Although this has been the case for many periods, the recent increases in the Bank of England base rate have pushed up mortgage rates, which, in the short term at least, has led to a c 4% decline in house prices. It remains to be seen whether this trend continues.

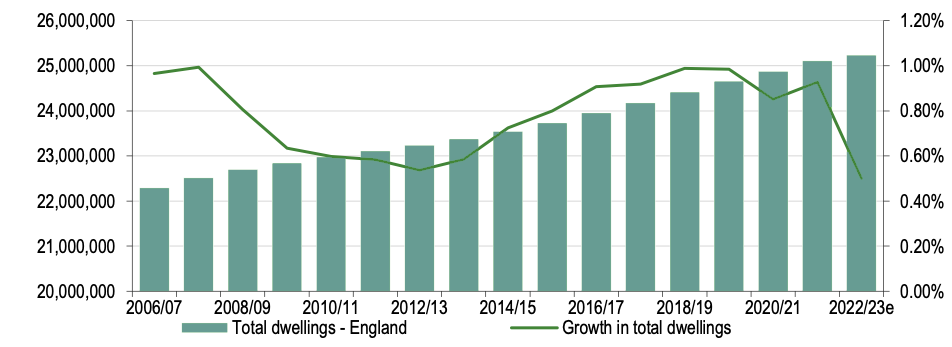

The number of homes in England has increased every year to satisfy growing demand from a growing population. The same trends exist in Scotland, where Springfield Properties operates, and in the Republic of Ireland, where Cairn Homes and Glenveagh Properties are among the market leaders. According to the UK government, the absolute number of dwellings rose from c 22.2 million homes in 2006/07, to just over 25 million in 2021/22. This implies an average growth rate of 0.8% pa. For the year to March 2023, we estimate that the growth rate will moderate as housebuilders have slowed output after demand fell away in the autumn.

Exhibit 1: Total number of dwellings England and annual growth (right-hand side)

Source: Department for Levelling Up, Housing and Communities, Edison Investment Research

For many years, the UK government had a target of building 300,000 new homes annually by the mid-2020s, but this has not been achieved. The target imposed mandatory housebuilding targets on local councils that were deemed not to be objective. As a result, the target is now advisory rather than mandatory.

In 2021/22, there were 238,490 new homes added to the overall housing stock. Exhibit 2 below shows the various sources of new housing in England. By far the biggest contributor to the overall housing stock is new houses, with around 50% of the total built by the quoted sector, including larger names such as Barratt Developments, Persimmon and Taylor Wimpey and some more modest-sized contributors such as Crest Nicholson, MJ Gleeson and Vistry Group. Other contributions to overall volume come from buildings converted from office to residential use, and from conversions of larger homes into flats. These additions were offset by a total of 5,680 demolitions, which implied a net total increase of 232,810 dwellings.

Exhibit 2: Net additional dwellings and source

Source: Department for Levelling Up, Housing and Communities

Until the last few months of 2022, house prices in the UK had rarely declined at any point in the last 30 years, with the notable exception of 2008/09 when house prices fell by nearly a quarter over an 18-month period, from an average of around £194k to £158k. The main reasons for this almost unstoppable trend are numerous, but the two main drivers are market undersupply and, until recently, declining or low interest rates. The hiatus in the markets in September 2022 triggered the recent decline, which saw the average house price fall from £294k in August to £282k in January, with the latter figure just £29 lower than in December, potentially suggesting that declining prices may be short lived. The £12k fall in prices from August to January mentioned above represents a fall of 4%.

Across the UK, the annual change in overall prices slowed from a peak of +12.5% in June, to just +1.9% in January. The shape of the slowdown was the same in every region, including London, and in every country of the British Isles. The elevated level of the price of housing, now coupled with higher interest rates, has added to the issues of affordability that are discussed below.

Exhibit 3: Halifax UK average house price-30 yrs

Source: Refinitiv

Exhibit 4: Halifax UK average house price inflation-30yrs

Source: Refinitiv

Stretched affordability to show signs of easing

It has been well-known for many years that higher house prices rather than high interest rates have stretched affordability. Towards the end of 2022, the sharp increase in mortgage rates compounded an already tight situation. However, in the early months of 2023, the Bank of England has signalled that the base rate may have peaked and that inflation is likely to fall materially this year. Coupled with rising salaries and modesty declining house prices, this should take some of the pressure off the affordability ratios, implying a housing market that is more accessible to potential buyers than was feared last autumn.

Higher mortgage rates to remain a headwind in 2023–24

While the news on mortgage rates is mildly constructive, affordability is likely to remain a headwind. Using data from Nationwide’s most recent (January 2023) Affordability Report, we illustrate below how mortgage servicing costs for first-time buyers are currently well above long-term averages across the UK.

Exhibit 5: Nationwide first-time buyer mortgage payments as a % of take-home pay

Source: Refinitiv, Edison Investment Research

On a positive note, in the absence of a fall in house prices, a mortgage rate of c 5.75% would be required for these affordability measures to challenge the highs seen in 2007. As explained below, we believe that this is highly unlikely. Clearly, in this context, any fall in house prices would be considered an additional support to affordability. Although there will undoubtedly be a squeeze in mortgage servicing ability over 2023–24, this could possibly be mitigated by a more rapid fall in policy rates and/or reductions in food and energy prices for people with disposable income.–

Capital values are a longer-term issue

House pricing and mortgage access, rather than mortgage affordability, are likely to remain the binding constraint for buyers over the medium to long term and can be considered a structural issue. As illustrated below, data suggest that although affordability measures appear unlikely to challenge recent peaks in the least affordable region of the UK (invariably London) or the most affordable region (usually the North of England), the average price to earnings ratio is only just coming off new highs and currently sits some 15% above the UK 20-year average multiple.

Exhibit 6: Nationwide UK house price-to-earnings ratio (x)

Source: Refinitiv, Edison Investment Research

More importantly, the absolute level of price to income multiples will likely continue to pose the most significant constraint in accessing mortgage finance in the UK. Here, the current reading of 6.6x and 20-year average of 5.8x lie well above the 4.5x that lenders are typically willing to offer. Thus, prospective first-time buyers are frequently left in the position of having to find a sizeable deposit. This is often supported by gifts, loans or inheritances from friends or family, but such wealth transfers – particularly if funded from residential equity release – cannot be considered a long-term solution. Ultimately, the issue of chronic undersupply will need to be addressed, although in the short term this very lack of supply is conditioning current market median expectations of a 5–10% fall in house prices over 2023–24 and a return to moderate growth over the medium to long term.

UK interest rates: The calm after the storm

Unhelpful headlines in the autumn predicting a deep recession in the UK have given way to far less apocalyptic expectations, especially after the Office for National Statistics reported zero rather than negative GDP growth in Q422. Even before this announcement, the overnight index swap curve had been moderating steadily since September as inflation expectations have fallen and this is now firmly reflected in mortgage rates, where both two-year and five-year fixed 75% LTV products have seen pricing decline by c 100bp. With funding costs declining and the mortgage market remaining competitive, additional declines in mortgage rates are likely, further easing market pressures.

Policy rates close to peak: Enjoy the ride down

Although UK interest rates have been highly topical in recent months, much has been taken out of context and widely misreported. Media attention has arguably focused on projections based on market measures of assumed policy rates, such as overnight index swap forward contracts. Such data was then typically presented as a formal Bank of England forecast on rates and the broader UK economy. This ultimately gave rise to highly misleading headlines such as ‘Bank of England expects UK to fall into longest ever recession’, assuming that policy rates would hit c 6%.

A more careful reading of the Bank of England’s Inflation Report in November 2022 suggested that if interest rates followed such a path, the UK would not only fall into a deep economic slump, but inflation would also quickly fall to zero. This is well below the Bank of England’s 2% inflation target and a reasonable inference would therefore be that the market’s expectations were inappropriately high. Indeed, as illustrated below, market expectations have since moderated significantly.

Exhibit 7: Overnight index swap curve evolution (%)

Source: Refinitiv, Edison Investment Research

However, if we update this analysis to account for the Bank of England’s most recent (2 February) Inflation Report, market rates would still bring inflation to below its 2% target by Q224 – well within its forecast horizon – and continue to drive inflation further below target thereafter. Moreover, the significant recession expectations have largely evaporated. This suggests that current rate expectations have scope to moderate further. Indeed, in unveiling the most recent Inflation Report, Bank of England Chief Economist Huw Pill said policymakers should ‘enguard against the possibility of doing too much’, presumably in an effort to nudge market rates down further.

It remains to be seen how these developments feed through to the mortgage offers available to buyers of UK residential property. As suggested above, the ground has shifted significantly in recent months and this is typically reflected with a delay in mortgage offers. However, there are already some signs that fixed-rate packages are again becoming more affordable, as shown below.

Exhibit 8: UK fixed-rate mortgage evolution (%)

Source: Refinitiv, Edison Investment Research

Given the lagging nature of the interest rate pass through, it is likely that, with policy rates at or near a peak and longer-dated funding costs still declining, the downward trend will continue. The UK mortgage market remains very competitive, lenders have been slow to pass rate hikes on to depositors and mortgage lending remains an efficient way of deploying risk capital.

Removal of support schemes less of an issue

The government’s main house buyer support tool, Help to Buy, had been in place since 2013, but has now been phased out because it was believed to distort the market and was poorly targeted. That said, it was very popular with both new house buyers and housebuilders and was well used. In its place, several alternative schemes have sprung up that are more restrictive than Help to Buy, as well as new support packages funded by the housebuilders that are designed to aid buyers. These include discounts to selling prices, cash contributions and part exchange schemes. Collectively, it would appear that the hole in the market left by the demise of Help to Buy is likely to have less of an effect than first feared, in our opinion.

Expiry of government schemes

The UK government had two house purchase schemes for first-time buyers, one of which has expired and the other is due to expire by the end of 2023. The first of these was the Help to Buy equity loan scheme, which accounted for 46% and 19% of Taylor Wimpey’s sales in 2020 and 2021, respectively. The scheme allowed customers to purchase a new-build home with just a 5% deposit and with an additional 20% as a five-year, interest-free equity loan. The rest of the purchase cost could then be financed with a 75% LTV mortgage. In London, the equity loan limit was 40%, implying a potential loan requirement of 55%. New applications for this scheme closed on 31 October 2022, with no plans for it to be extended or replaced.

The Mortgage Guarantee Scheme will expire on 31 December. This scheme enabled banks to offer 95% LTV mortgages to first-time buyers, provided they had a deposit of 5%. It was announced to support a new generation of homeowners during the COVID-19 pandemic, when there was a reduced availability of high LTV mortgage products, particularly for prospective homebuyers with 5% deposits. The scheme was implemented only on UK properties with a purchase value of £600,000 or less.

It is important to note that there will be a range of alternative support options available to prospective new home buyers after the withdrawal of the schemes mentioned above. These include the Deposit Unlock scheme, First Homes initiative and shared ownership. According to Savills, if these three schemes realise their potential during the three years following the official end of Help to Buy they will combined have the ability to support the delivery of 50,000 homes per year. However, this represents a c 30% reduction in the estimated 72,000 new home sales each year supported by the combined Help to Buy and shared ownership schemes. It is worth adding a caveat to these figures: some users of the Help to Buy scheme did not need to use it, or bought larger homes than they would have done because it was possible to do so. This is likely to have caused some distortion in the market.

The replacement support schemes mentioned above are outlined below.

Deposit Unlock scheme

The Deposit Unlock scheme was created by the Home Builders Federation alongside reinsurance broker Gallagher Re. It enables buyers to obtain new homes with only a 5% deposit, which replicates one of the fundamental selling points of Help to Buy. It makes buying a new home easier than purchasing an existing property for those with a 5% deposit, thereby enabling new-builds to retain some competitive advantage.

Under the scheme, mortgage lenders are protected by a mortgage guarantee, which is funded by the housebuilder and covers 35% of the property value. The scheme has the potential to continue to help a substantial proportion of customers to buy new homes.

First Homes – government offering

First Homes was launched by the government in June 2021. It helps first-time buyers get on the property ladder as a property is purchased after applying a typical discount of 30–50% on the typical market rate for the local area (local authorities set the discount rate). The scheme is part of a wider government commitment to deliver one million new homes by 2024.

The property must be valued below £250,000 (£420,000 in London) after applying the discount and the scheme is only available to households with a combined income of less than £80,000 a year (£90,000 in London). The buyer must be able to pay a deposit of at least 5% of the discounted purchase price. When the house is sold, it must be sold to another eligible purchaser, and with the same discount to the market price at the time of selling.

Shared ownership

Under a typical shared ownership scheme, buyers purchase an initial stake in the property and rent the remainder at a discount. Before Help to Buy, initial stakes of more than 50% were common, but, due to competition with Help to Buy, lower initial stakes started to dominate (initial stakes of 10% are now allowed on some homes). The current programme is set to run from 2021 to 2026 and is funded through the Affordable Homes Programme.

In addition to the initiatives mentioned above, many housebuilders have introduced their own schemes to encourage people to commit to buying a house. For example, Barratt Developments is currently offering a contribution of up to £30,000 (£1,000 for every £20,000 of the purchase price) to first-time buyers and home movers on selected properties. This could be a mortgage or deposit contribution, or money towards moving or running costs.

MJ Gleeson is currently offering £250/month towards mortgage costs, or up to £3,000 towards a deposit or a similar figure towards options and extras. Again, this offer only applies to selected plots. Part-exchange is also an increasing feature of the housing market, with many housebuilders offering this feature on selected plots. The clear advantage here is that it removes the stress of selling an existing home from the vendor because the housebuilder handles the sale process, with the vendor remaining in their existing property until the new build is ready, thus securing a sale, with a minimum amount of stress for the vendor/new house buyer.

Cost inflation and other costs unlikely to derail sector

Material and labour cost inflation has been elevated for the last 18 months as the cost of energy rose and demand remained high. However, both of these factors are now easing, which should reduce pressure on housebuilders’ margins to a degree. In addition, over the last few years, the sector has been hit with a series of measures that will, in most cases, result in a drag on profitability, at least in the short to medium term. That said, the costs of introducing the Future Homes Standard are likely to be absorbed as they become standardised. Other costs, such as the Residential Property Developer Tax (RPDT) and remediation for cladding issues, will be a drag. The former is a tax on profits, but the costs of the latter have largely been provided for already, so the expenses of remediation are likely to be a negative for cash flow, rather than profitability.

Materials mixed, but falling overall

At the component level, building material inflation presents a very mixed picture. While some processed items, such as paint and insulating materials, still exhibit high levels of price inflation, others like structural steel and wood have seen either significant disinflation or outright deflation. However, on a weighted basis, residential building material inflation is now tracking down towards 10% year-on-year, having peaked at more than 24% in June 2022, as shown below.

Exhibit 9: Selected building material inflation year-on-year (%)

Source: Office for National Statistics, Edison Investment Research

While any further extrapolation of these deflationary trends should be treated with caution, it is clear that much of historical price inflation has been driven by a combination of lingering supply chain problems arising from the COVID-19 pandemic and the specific disruption to European energy supplies. However, it is notable that efforts to mitigate supply chain issues remain a focus throughout the private sector, while Dutch Title Transfer Facility gas prices – a reasonable proxy for European wholesale energy prices – continue to track down for winter 2023/24 contracts.

Wage pressures appear contained

Aside from material input costs, it is also worth considering wage pricing within the construction sector. As the chart below suggests, prior to the 2020–21 COVID-19 disruption, construction sector workers generally enjoyed wage rises above the broader private sector average and also above inflation. By H222 however, construction sector wage inflation has been contained to c 5% versus the 7%+ seen within the private sector, perhaps being conditioned by previous inflation-busting wage increases.

Exhibit 10: UK year-on-year wage inflation (%)

Source: Office for National Statistics, Edison Investment Research

This moderation in construction sector wages comes despite sector employment c 200k lower than pre-pandemic levels and the support the sector has seen through elevated levels of activity in both refurbishment and public sector projects. Under these conditions, we feel that it is reasonable to assume that wage pressures within the private residential segment for new-build properties is also largely contained.

Extra costs from the introduction of the Future Homes Standard

Government policy continues to have a significant impact on the design and materials used in houses, mainly brought about through the Future Homes Standard (FHS) and changes in building regulations. The FHS is focused on the ‘future-proofing’ of new-build homes with low carbon heating and world-leading levels of energy efficiency by 2025, which will contribute to the larger goal of achieving net zero emissions by 2050. The first FHS consultation was set in two parts: Part L (Conservation of fuel and power) and Part F (Ventilation). The expectation is that the average home built will produce 75–80% less carbon emissions in use than one built to previous requirements through high fabric standards and low- carbon heating systems; these will force companies to implement a variety of installations into new builds including air source heat pumps (ASHPs, which can convert a single KW of electricity into 3KW of heat energy, making them extremely energy efficient), triple glazing and standards for walls, floors and roofs that significantly limit heat loss. Interim amendments to building regulations (Part L and F) came into force on the 15 June 2022, which require new homes to deliver savings of 31% compared to existing standards. This uplift is intended to lay the foundations for successful implementation of the FHS in 2025. Developments that had already received planning permission prior to 15 June 2022 are able to remain under 2013 set regulations, but will need to have commenced construction by June 2023 or else they will have to comply to the new regulations.

The majority of the largest UK housebuilders have started implementing the new standards:

Bellway has built an experimental eco-house with the aim of testing zero-carbon technologies for new properties from 2025. It is examining the effectiveness of a range of installations including double/triple glazing, solar energy storage, heat recovery from wastewater and the installation of ASHPs.

Redrow has piloted its first gas-free, low-carbon home, which uses Wondrwall’s AI-powered home automation, intelligent heating with solar electricity panels and a smart energy management system. Combined, these have the ability to achieve fuel savings of 33–50%.

Barratt has launched its first ASHP development at Delamare Park, with homes on the development further benefiting from enhanced insulation. Additionally, the group has completed its zero-carbon concept home, the ‘Zed house’, which goes beyond the FHS by reducing carbon emissions by 125% relative to current standards.

MJ Gleeson plans to install ASHPs in all new homes built from June 2023; (it installed its first ASHP in a detached home in September 2021, which showed improved efficiency of 293% compared to 94% with a gas boiler).

The FHS creates an opportunity for the UK housebuilder sector to be a prominent driver in the green agenda, although with only two years until 2025 the relevant companies will need to continue innovating rapidly. These companies will face a lot of pressure to prepare supply chains and develop new technologies to comply with the stringent energy efficiency requirements for new homes. Undoubtedly this will incur higher build costs, putting pressure on land values. According to a survey of UK housebuilders, there will be additional costs in meeting the revised Part L requirements to 2025 of 3–7%, for those reported as being in the ‘in progress’ stage of preparation. We would expect these additional costs to substantially decrease in the long term as volumes rise with increased market adoption.

Residential Property Developer Tax

From 1 April 2022, the new RPDT of 4% was implemented to help fund the costs of cladding remediation works, mentioned in more detail later. This applies to operating profits (ie pre-tax and before interest) exceeding the annual allowance of £25m per year, arising from residential property development recognised in accounting periods ending on or after that date. The government intends for this policy to last for a decade, but it will consider extending the period if insufficient funds are raised.

For relevant companies, this brings the effective corporation tax rate up to 23% from April 2022 and up to 29% from April 2023 (when the main corporation tax rate is scheduled to increase to 25%). The RPDT is calculated using the same principles as UK corporation tax but with the following exclusions, which could be used to diminish RPDT profits:

Carried forward or surrendered losses derived from non-residential development activities including capital allowances or charges.

Interest and other financing costs.

This tax will dent future earnings of UK housebuilders and raise more than c £200m pa for the Treasury. Barratt Developments has stated that over the next 10 years it will be paying c £400m for the tax, representing just under 40% of its FY22 adjusted operating profit of £1.055bn.

However, it is not all doom and gloom for UK housebuilders. With the stamp duty cut, announced in the mini-budget, remaining in place until 31 March 2025, the resultant overall lower cost of purchasing a new home in the UK may drive demand. For first-time buyers, the threshold amount from which the stamp duty land tax (SDLT) is applicable to will rise from £300,000, to £425,000. The government is enabling first-time buyers to access this SDLT relief when buying any property valued at less than £625,000, an improvement compared to the previous £500,000. These measures enable a reduction of stamp duty bills in the UK for all movers by up to £2,500, with first-time buyers able to save up to £8,750.

These cuts may increase interest in the UK housing market and support first-time buyers in embarking on the property ladder, which could somewhat recover the earnings of UK housebuilders. Additionally, the Office for Budget Responsibility (OBR) has forecast that house prices will fall 9% between Q422 and Q324 due to higher mortgage rates and the wider economic downturn, which may ultimately improve buying activity. However, it is important to note that this will likely be more of a long-term (12–24 month) occurrence, as on a short-term basis the expectation of house price falls will likely dampen demand as prospective buyers will wait to buy until these price falls have occurred.

Cladding crisis: Largely affecting the valuation of the sector

A building safety repairs pledge has been developed by the government to address the tragic Grenfell Tower fire incident in 2017 that killed 72 people, which was partially blamed on developers’ use of combustible cladding. The 49 developers that as of 9 August had signed the agreement have committed to remediate crucial fire safety works in buildings exceeding 11 metres for which they have contributed to the development or refurbishment of over the last 30 years. This also includes an agreement to reimburse any funding received from government remediation programmes in relation to buildings that had a role in developing or refurbishing. The Department for Levelling Up, Housing and Communities (DLUHC) stated that this pledge should amount to a commitment of at least £2bn over the next 10 years.

In addition to this new developer pledge, the government has proposed an extension called the Building Safety Levy of c £3bn over the next 10 years, which is chargeable to UK developers when applying for planning permission on new residential projects. This will see the UK housebuilding industry contributing a combined total of c £5bn to address the building safety scandal.

Due to the complexity of the matter, the exact remediation works and number of buildings will take time to determine. Barratt Homes stated that it could take anywhere between five and seven years with a cost of £350–400m to fix all the fire safety issues on the entirety of its required buildings; according to its FY22 results, over £396m has been put aside for the remediation of existing buildings.

The pledge is in addition to the RPDT of 4% of pre-tax profit, which came into effect on 1 April 2022, mentioned above. We expect these necessary additional costs will if anything have only a minor impact on the volumes of houses built in the UK; UK housebuilders remain profitable businesses and reduced demand due to high property prices will have a larger impact on volumes. In addition, most of the cash associated with provisions for safety remediation work is yet to flow out, leading to a resultant drag on cash generation over the next few years.

Depressed valuations could recover materially

The depressed levels of share prices in the sector reflect the recessionary fears that pervade the market. However, we believe that over time, not only will markets begin to stabilise and then recover, but the housebuilder sector will eventually be able to offset higher costs via a combination of efficiencies, likely house price inflation and adjustments to the prices at which housebuilders are willing to buy new land. Therefore, currently depressed returns on equity could rise and the ascribed valuations should follow suit.

The UK housebuilder sector has been hit significantly by a cocktail of toxic pressures. As a homogeneous industry, almost all constituent companies have seen their share prices plummet having largely recovered from the sharp drop seen in March 2020, affected by the COVID-19 pandemic. However, they have since underperformed consistently and on average are down 25% in absolute terms over the last 12 months, versus the UK market up c 8%. Challenging times appear on the horizon as higher raw material and labour costs put pressure on margins and rising interest and living costs cause homebuyers to rethink a new purchase.

Exhibit 11: Sector performance in recent periods

Absolute share performance (%)

Price (p/€c)

Ytd (%)

One month

Three months

Six months

12 months

Barratt Developments

467.2

17.7%

2.1%

18.1%

0.8%

-22.5%

Bellway

2165

13.5%

0.4%

9.1%

-3.1%

-26.0%

Berkeley Group Holdings

4173

10.6%

-3.8%

12.9%

5.4%

5.0%

Cairn Homes

0.96

10.4%

-2.7%

5.5%

-12.3%

-24.6%

Crest Nicholson Holdings

236

-0.3%

-5.1%

9.9%

-11.5%

-25.9%

Empiric Student Property

87.6

4.0%

-2.8%

-3.8%

-11.3%

-4.3%

Glenveagh Properties

0.99

14.1%

8.5%

5.9%

-10.7%

-19.6%

Grainger

253.6

0.6%

-3.6%

5.9%

-11.6%

-11.8%

Henry Boot

241.5

2.8%

3.2%

1.5%

-16.7%

-20.6%

Inland Homes

8.85

-62.3%

-51.5%

-52.2%

-71.9%

-82.5%

Kier Group

74.6

25.8%

15.3%

25.0%

-2.0%

-22.2%

MJ Gleeson

460

33.7%

10.0%

23.0%

-12.5%

-34.1%

Morgan Sindall Group

1684

10.1%

3.2%

8.8%

-7.9%

-22.4%

Persimmon

1431.5

17.6%

0.3%

10.8%

-16.0%

-40.6%

Redrow

511

12.6%

-1.8%

15.7%

-6.3%

-14.8%

Springfield Properties

92.5

23.3%

4.5%

1.6%

-30.2%

-38.3%

Taylor Wimpey

121.2

19.2%

3.6%

19.8%

1.8%

-18.5%

Unite Group

991.5

9.0%

-0.4%

5.1%

-13.9%

-1.0%

Vistry Group

785.5

25.6%

5.2%

24.7%

-8.2%

-22.3%

Watkin Jones

99.1

-1.3%

-12.3%

4.1%

-55.8%

-59.6%

MSCI UK market Index

2302.41

7.4%

2.1%

9.0%

6.6%

7.6%

Source: Refinitiv, Edison Investment Research Note: Prices as at 16 February 2023

According to Halifax, the average UK house price increased c 10% in the 12 months to September 2022, but had fallen c 4% by January 2023 to £282k, representing annual growth of c 2%. This will undoubtedly have a negative impact on the sector alongside the sudden acceleration in mortgage rate increases seen with the implementation of the mini-budget. The question remains as to when or if UK housebuilders valuations rise to more normalised multiples.

Exhibit 12: Price/book values over the last six years – seven of the largest UK housebuilders

Source: Refinitiv

Headwinds facing the housebuilding sector is not a new phenomenon. One only has to look at the global financial crisis for evidence of the effect of lower house prices and falling demand on a company’s share price, especially if there are concurrent questions raised about the long-term viability of an entity following ill-timed M&A. This was the case in 2008 when the share prices of some leading housebuilders plunged to very low levels. For example, the share price of Taylor Wimpey peaked at 386p in April 2007 and collapsed to just 6p 18 months later. The collapse was arguably justified at the time as balance sheets in some cases were very stretched following M&A activity.

However, the current situation is very different. While there are certainly question marks relating to the outlook for house prices, affordability and demand, it should be noted that the sector has proved to be resilient in the past and is likely to be so again in the future. For example, in the early 2000s, both Persimmon and Taylor Wimpey reported peak returns on equity (RoE) in 2004, of 25.6% and 17.6% respectively, before going on to report losses in 2008. However, roll the clock forward and the former generated an RoE in of 27.7% in 2018 and the latter 21% in 2016. Both figures being c 2–4pp higher than the previous peak.

In our opinion, there are many factors that have contributed to the improved peak RoE: cost efficiency, more efficient plotting, common house types and house price inflation to name a few. But housebuilders also have the ability to influence returns by managing land spend. For example, on any given piece of land, or individual plot, the housebuilder will have a very good idea of labour and material costs, and likely sales prices, and will therefore be able to work out the maximum price it can pay for the land in order to generate its required return.

Therefore, it is likely over a period of a few years that a housebuilder will be able to reflect higher costs from, for example, the Future Homes Standard or the RPDT, in the prices it is willing to pay for land via a residual sum calculation. On this basis it is entirely possible that each housebuilder should be able to make superior returns to those that are forecast for the near term, and potentially revisit the higher returns mentioned above.

Exhibit 13: Taylor Wimpey – P/NAV versus RoE

Source: Refinitiv, Edison Investment Research

Exhibit 14: Persimmon – P/NAV versus RoE

Source: Refinitiv, Edison Investment Research

The charts above give an indication of the potential upside in the share prices in this largely homogenous sector. In the case of Persimmon, consensus estimates suggest that in 2023 it will generate an RoE of 11.2%, less than half the level of its peak year of 27.7%, while it trades on price to book ratio of just 1.3x, a little over half its peak valuation of 2.4x. The implication here is that when the sector is able to demonstrate a path back towards peak returns, the valuation attributed to the shares would be considerably higher and somewhat closer to the 2.4x peak.

A similar situation exists with Taylor Wimpey. Consensus estimates that it will make an RoE of 8.3% in 2023, compared to a peak return of 21%. It currently trades on a price to book ratio of 1.0x, compared to 2.0x in 2016, suggesting that the share price could double if the market thought it was likely to revisit previous peak returns on equity. A similar situation exists for almost every stock in the sector.

These calculations assume that there are no, or only very modest, asset impairments. Barratt Developments recently stated that if house prices fell a further 5% (they are already down 4% according to Halifax)), it would need to impair the carrying value of its land bank by c £16.3m, or 0.5%. Given that the decline in house prices slowed to almost zero in January, it appears that the risks of widespread material asset impairments is dissipating and that book values are robust.

Exhibit 15: Housebuilding sector valuation

Company

Year end

Market cap (£)

Net cash/ (debt) (£m)

Price (p)

P/book (x)

ROE (%)

P/E (x)

Dividend yield (%)

FY

FY1e

FY2e

FY

FY1e

FY2e

Barratt Developments

Jun-23

4,663.1

996.2

467

0.8

11.9

5.7

6.9

11.7

7.9%

7.2%

5.1%

Bellway

Jul-23

2,680.9

378.5

2,165

0.7

11.2

5.1

6.6

11.0

6.5%

5.6%

3.9%

Berkeley Group

Apr-23

4,537.5

405.6

4,173

1.4

14.2

10.1

10.1

12.0

0.0%

4.4%

5.5%

Cairn Homes

Dec-22

589.3

(107.0)

86

1.0

10.4

17.8

8.7

7.3

5.3%

5.9%

9.5%

Crest Nicholson

Oct-23

608.0

232.0

236

0.7

6.7

5.6

10.6

12.0

4.9%

4.1%

3.5%

Empiric Student Property

Dec-22

530.0

(327.5)

88

N/A

3.1

53.1

26.3

20.2

2.9%

3.0%

3.9%

Glenveagh Properties

Dec-22

531.8

(18.9)

88

1.0

7.6

23.6

12.8

11.6

0.0%

7.5%

6.6%

Grainger

Sep-23

1,885.6

(1,395.3)

254

0.9

3.2

24.9

25.0

23.6

2.4%

2.5%

2.9%

Henry Boot

Dec-22

323.7

(19.6)

242

N/A

8.6

11.6

10.0

12.8

2.5%

2.8%

3.0%

Inland Homes

Sep-22

19.9

(100.2)

9

N/A

N/A

2.1

1.7

1.3

0.0%

0.0%

0.0%

Kier Group

Jun-23

333.9

24.3

75

N/A

17.9

4.5

4.0

3.6

0.0%

0.0%

5.5%

MJ Gleeson

Jun-23

269.1

16.2

460

0.9

9.1

5.9

11.1

10.8

3.9%

3.1%

3.1%

Morgan Sindall Group

Dec-22

799.6

308.8

1,684

1.6

22.2

7.7

7.4

7.5

5.5%

6.0%

6.1%

Persimmon

Dec-22

4,583.7

833.0

1,432

1.3

20.2

5.8

5.9

11.3

16.4%

12.9%

6.5%

Redrow

Jun-23

1,694.9

242.8

511

0.8

13.9

5.3

6.2

9.8

4.3%

6.0%

3.9%

Springfield Properties

May-23

109.9

(55.0)

93

0.8

15.4

6.1

6.5

6.4

6.7%

6.8%

7.2%

Taylor Wimpey

Dec-22

4,292.6

832.3

121

1.0

14.6

6.7

6.3

11.7

7.1%

7.9%

7.2%

Unite Group

Dec-22

3,979.8

(895.6)

992

1.1

4.3

35.9

24.3

22.1

2.2%

3.3%

3.6%

Vistry Group

Dec-22

2,723.0

179.4

786

0.7

11.4

6.3

5.8

9.1

7.6%

8.4%

5.8%

Watkin Jones

Sep-23

254.8

78.7

99

N/A

10.5

6.7

6.6

6.0

7.5%

7.6%

8.4%

Source: Refinitiv, Edison Investment Research Note: Prices as at 16 February 2023

General disclaimer and copyright This report has been prepared and issued by Edison. Edison Investment Research standard fees are £60,000 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison’s policies on personal dealing and conflicts of interest. Copyright: Copyright 2023 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for “wholesale clients” within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument.

New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “FPO”) (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person.