“Edison is the go-to for a new investor to get full understanding of the investment case and business. Edison’s distribution reaches investors that we want to connect with directly.”

The IMF forecasts global GDP growth will slow from 3.4% to 2.9% in 2023, with Europe (excluding the UK) forecast to grow at 0.7%. Recent economic activity surveys paint a slightly more positive picture, but generally, more muted market expectations for returns are arguably fully reflected in valuations. While economic activity might be expected to be a key driver of stock market returns, studies have not found there to be meaningful correlation between regional economic growth and shareholder total returns. Europe can suffer from a perception of being low growth, however this is often not the reality at the corporate level, with the region being home to industry global leaders. Investors do not need to be positive about the outlook for the European economy to invest in the region; stocks can do well regardless of the direction of the domestic economy. Specifically, Europe is at the forefront of investment and development in the secular long-term growth themes of energy transition, efficiency and security, which has come into sharp focus since Russia’s invasion of Ukraine. For this note, Europe is defined as continental Europe ex UK.

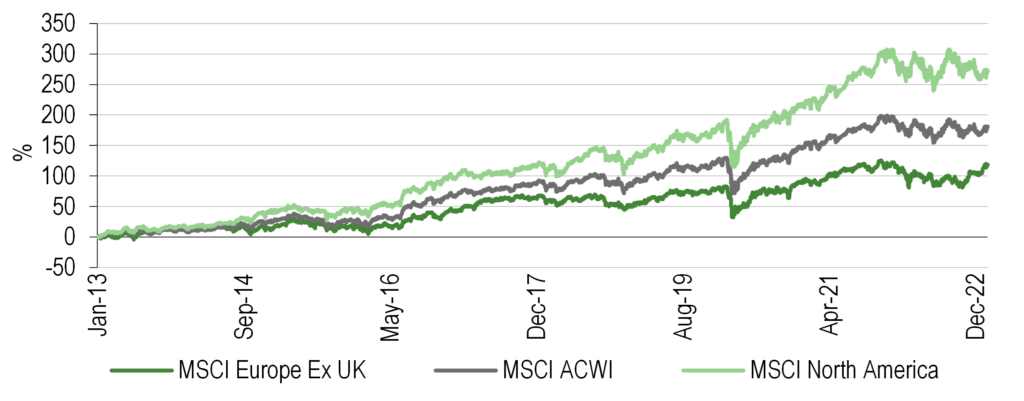

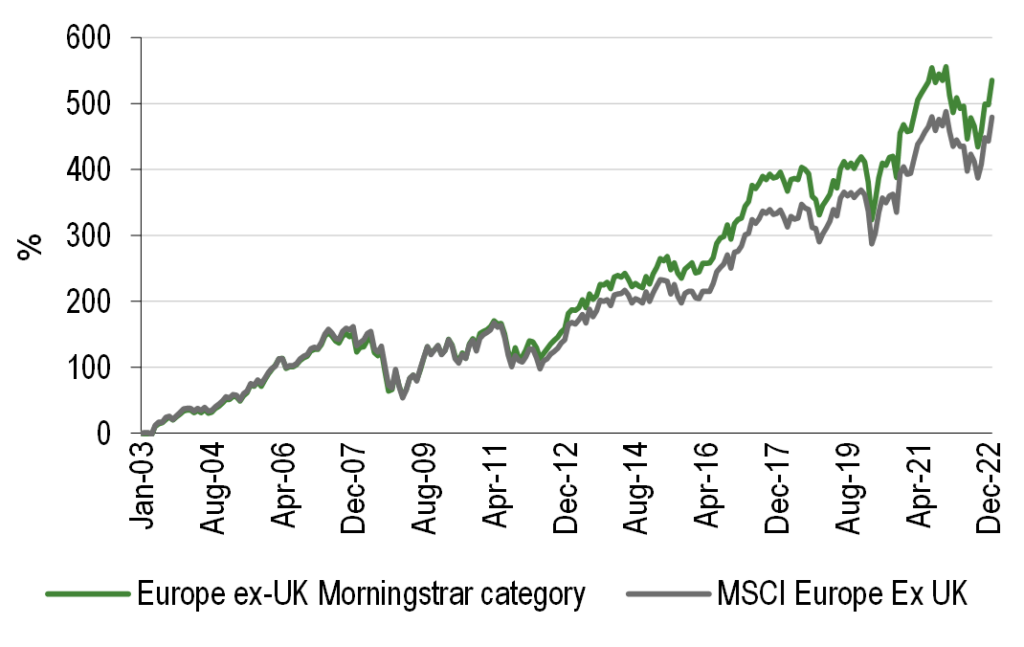

European market returns have lagged global and US returns

Source: Morningstar. Note: Total returns in pound sterling.

Key takeaways

There are tentative signs of recovery in European economic activity but further downward corporate earnings revisions could still come through. Arguably, current valuations reflect investor pessimism.

Europe is home to some world-class companies with geographically diversified earnings, whose prospects are arguably largely unrelated to their European domicile.

Europe is out of favour with the investment community as evidenced via fund flows and investment trust discounts. As economic and earnings visibility improves, there is scope for this to be reversed, driving a virtuous circle for future returns in the asset class.

Changes are afoot within the European equity market, with a more diversified overall mix of industries, less financials and more technology and healthcare.

Europe is at the forefront, through the NextGenerationEU policy of long-term secular support, of the transition to renewable and greener forms of energy.

European active managers have a generally good record of outperforming indices, which may limit the penetration and efficacy of the use of passive investment strategies.

Light at the end of the tunnel?

The risks to economic growth are numerous and include an escalation of the war in Ukraine, further consumer weakness, trade friction between China and the West and central bank policy errors. The war in Ukraine has affected investor sentiment towards Europe, given its effect on energy costs. Within Europe, the Eurozone Composite Purchasing Managers’ Index (PMI, incorporating services activity and manufacturing output) has been below 50 (indicating contraction) since June 2022. The ‘flash’ for January 2023 saw a very modest increase of 0.4% from the December figure of 49.3 to 50.2, indicating a tentative first expansion of economic activity for seven months. This compares with the global composite survey of 48.2 in December, which was the fifth successive month of contraction (up from 48 in November, which was the 29-month low, and one of the weakest readings for over 15 years). While the global ‘flash’ was not available at the time of writing, there is some evidence that the eurozone is faring better in terms of economic activity than other parts of the global economy. January also saw the largest monthly increase in the eurozone PMI composite business expectations index since June 2020, while supply chain stress has abated due to less demand for materials given the weakening outlook for growth. Fidelity European Trust (FEV) portfolio manager Marcel Stötzel believes that although 2022 was a poor year for European equities, corporate profitability in 2023 and consensus estimates regarding earnings per share are likely to come under significant pressure as adverse macroeconomic conditions bite. He believes 2023 could be another difficult year, with some defensiveness likely to be found in companies with balance sheet strength and pricing power, with aerospace and defence, software and luxury goods favoured subsectors. However, Stefan Gries at BlackRock Greater Europe (BRGE) notes that despite a slowing European economy, corporate balance sheets are in better shape compared with previous downturns, following a decade of deleveraging. A higher-than-average savings rate provides a partial cushion as household incomes are squeezed.

Sentiment towards European equities remains downbeat

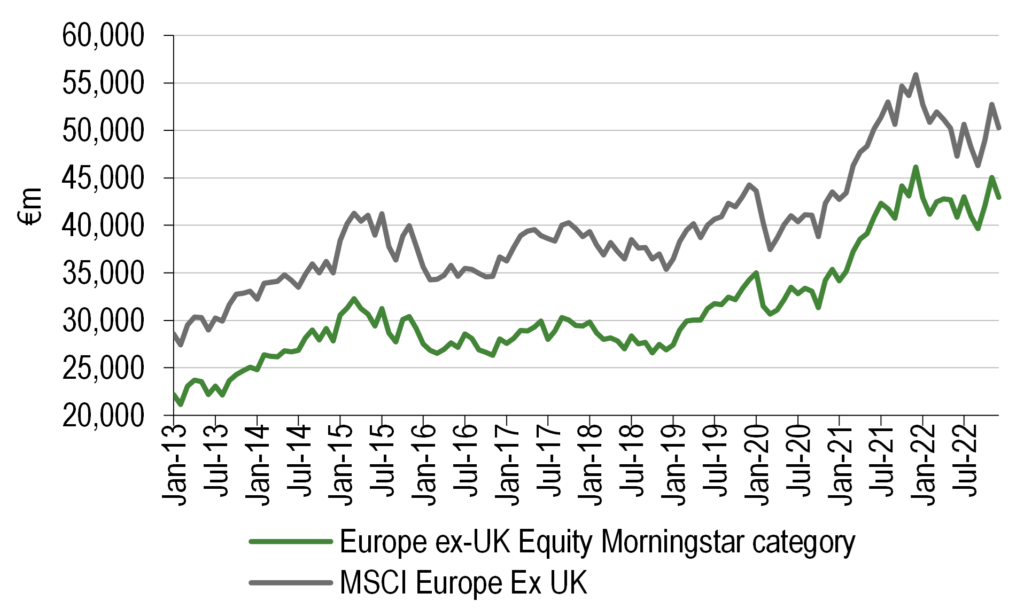

As an asset class, European equities remain unloved, with persistent fund outflows over the last five years (Exhibit 1) and wider discounts on European investment companies when compared with those positioned globally (Exhibit 2). In addition, sentiment surveys, such as the Bank of America’s fund manager survey, show investor pessimism towards European equities.

Exhibit 1: Weak fund flows for European equities

Source: Morningstar. Note: Estimated net (global) monthly fund flows.

Exhibit 2: European Investment Trust discounts are wider

Source: Morningstar. Note: Unweighted average discounts

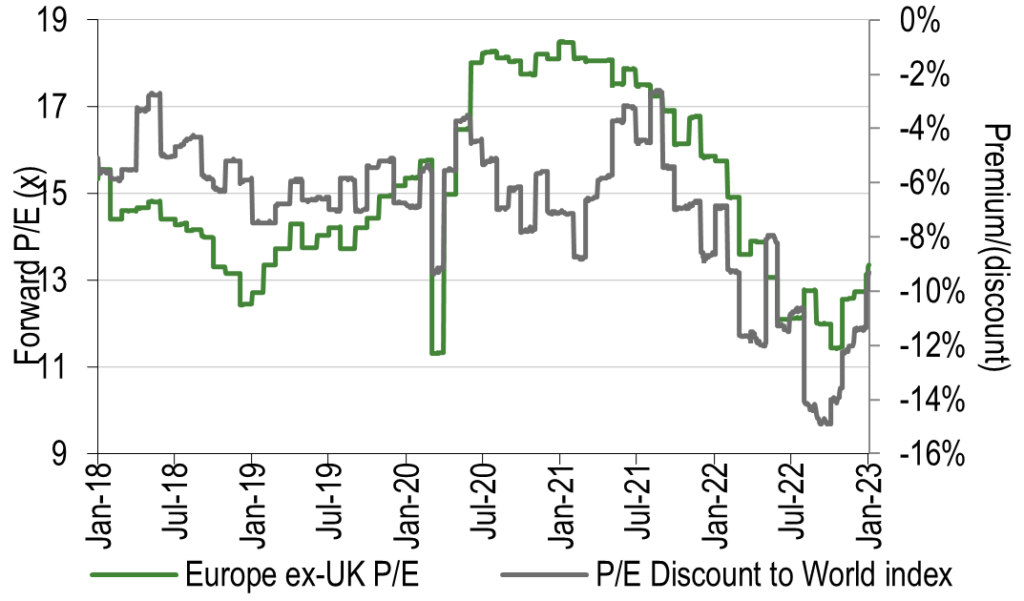

Valuation support for European equities

Exhibit 3: Europe offering value versus global comparators

Forward Europe ex UK price to earnings ratio versus global equities

Valuation metrics of Datastream indices (as 24 January 2023)

Last

High

Low

10-year average

Last as % of average

Europe ex UK

P/E 12 months forward (x)

13.4

18.5

11.2

14.6

91.7

Price to book (x)

1.8

2.1

1.3

1.7

105.8

Dividend yield (%)

2.8

4.4

2.1

3.0

93.3

Return on equity (%)

13.1

13.5

5.2

9.3

140.9

World

P/E 12 months forward (x)

14.7

19.9

12.4

15.4

95.5

Price to book (x)

2.2

2.5

1.5

1.9

115.8

Dividend yield (%)

2.4

3.4

1.8

2.4

100.0

Return on equity (%)

13.5

14.0

7.3

11.0

122.7

Source: Refinitiv, Edison Investment Research

Gries believes that the European stock market is attractively valued and corporate and consumer balance sheets in better shape now than they were heading into the last recession. There has been a decade of deleveraging, so debt levels look manageable and interest coverage is considerably higher than at the time of the global financial crisis in 2008. Likewise, European Assets Trust (EAT) fund manager Sam Cosh notes that European equity market valuations still look very supportive, especially against the US market. John Bennett, portfolio manager of Henderson European Focus Trust (HEFT), believes that the war in Ukraine is fully priced in (unless the conflict escalates significantly) and, with a strengthening currency versus the US dollar, investors are starting to take notice of the returns from the asset class.

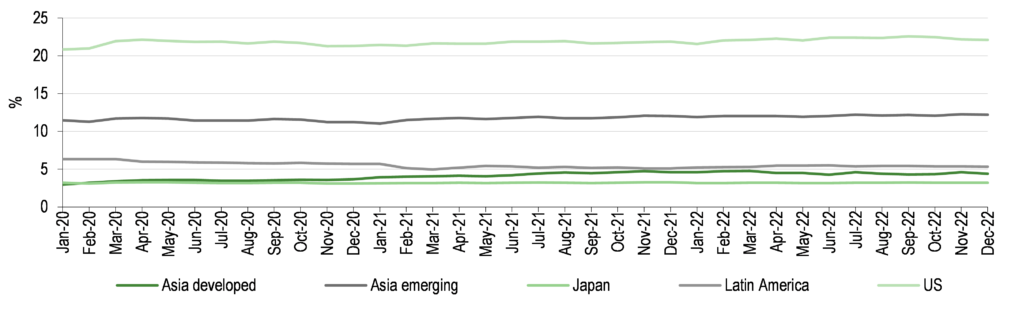

European equities: More than a play on domestic Europe

Exhibit 4: Underlying earnings exposure from the MSCI Europe ex UK Index

Source: Morningstar

Buying European equities is not purely a view on domestic-based earnings as many European companies, from LVMH to Nestlé, have substantial overseas earnings not reliant on the strength of European economic growth. This is a key point for Alexander Darwall, fund manager of European Opportunities Trust (EOT), whose investment process seeks global winners (domiciled in Europe), not those solely reliant on European growth. According to Morningstar, as a percentage eurozone earnings represent around 30% of the MSCI Europe ex UK Index. This leaves substantial scope for overseas earnings exposure, with around 20% earnings exposure to the United States, and a similar weighting to Asian and Latin American earnings. This provides the optionality for overseas and emerging markets growth from a portfolio of well-managed developed market equities.

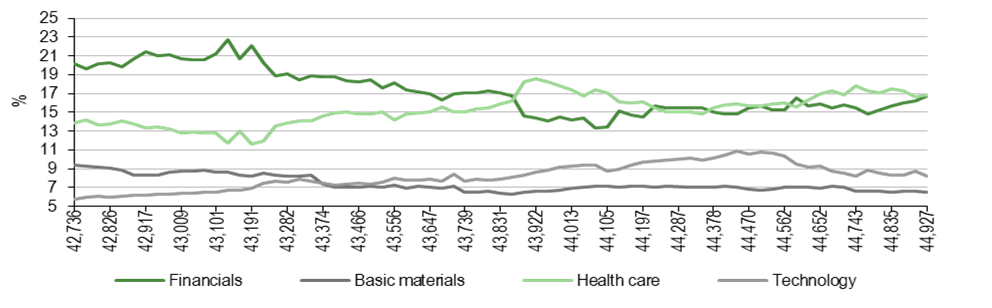

The changing face of the European market

As shown in Exhibit 5, sector weightings within the broad European market have changed over time from being dominated by arguably lower-growth sectors such as financials to a broader, more diversified sector balance with healthcare stocks, such as Novo Nordisk, and other higher-growth sectors, including technology names such as ASML for example, becoming more prominent.

Exhibit 5: Changing sector weightings within the European index

Source: Morningstar

Powerful secular tailwinds for sustainability in Europe

NextGenerationEU is the European Union’s €800bn funding programme to support economic recovery from the COVID-19 pandemic and transition to a greener, more resilient energy policy that reduces reliance on fossil fuels, especially those from Russia. According to the EU Global Leadership in Renewables (July 2021) survey, the eurozone has a strong position in terms of world market share, particularly in wind energy (67%), geothermal technologies (42%) and hydropower (39%).

Investment into renewable energy infrastructure, production and technology is a prominent trend across many European portfolios, including Henderson EuroTrust (HNE), where fund manager Jamie Ross addresses energy efficiency via ABB, while Metso provides exposure to materials used for electric vehicle (EV) development, such as lithium and cobalt. Lower down the market cap scale, smaller companies can often be integral to the technology required for the transition to clean energy and within the European Smaller Companies Trust (ESCT)there are investments in battery and energy storage, high-voltage cable suppliers, energy and transformation systems, associated infrastructure such as EV charging and green energy generators (wind and solar parks). These are via holdings such as NHOA, Manz, Energiekontor, Grenergy, KSB Group, Meyer Burger and TKH Group. Renewables have likewise been an area that JPMorgan European Discovery Trust (JEDT) and fund managers Ed Greaves and Francesco Conte have been playing, and the trust has exposure via French integrated renewable energy developer, storer and generator Neoen, Italian diversified renewable energy generation company ERG and Encavis, a German developer and operator of solar and wind parks. Meanwhile, Baillie Gifford European Growth Trust (BGEU) managers Stephen Paice and Chris Davies have added Nexans, a French cable manufacturer, whose products help build a more efficient and greener electricity grid. Alexander Darwall believes that Finnish Neste, which among other renewable-focused lines of business produces low-emission aviation fuel, is well positioned to benefit from the focus on more positive environmental outcomes. The European Assets Trust’s (EAT) exposure to energy transition is mainly within industrials holdings such as Hexpol, which provides materials for high-voltage cables, and Sdiptech, which owns Rolec, a manufacturer of EV chargers. Finally, John Bennett of HEFT is another manager with an eye on the energy transition, with holdings in Finnish forestry/paper company UPM-Kymmene Oyj, which is increasingly focused on renewables such as biofuels, while other holdings such as Shell and TotalEnergies have seen their proportion of sales from renewables increase, a trend likely to be multi-decade in duration.

Active can outperform passive in European equity markets

Passive investment vehicles such as index trackers and exchange traded funds (ETFs) have taken an increasing amount of market share from active managers over the last 20 years. This trend has been fuelled by the lower fees these funds charge and by the varying performance of active management (after fees) when compared with the indices that they use as a benchmark. In some cases, using trackers is a valid investment option; the efficacy of actively managed versus passive investment strategies is beyond the scope of this note, however there is some evidence that European equities is an area where active managers can outperform the mainstream index. Exhibit 6 illustrates this (but does not address the effects of survivorship bias where poorly performing or sub-scale funds are merged or wound up). Potential reasons for the outperformance of active over passive strategies in recent years are likely due to the strength of small-cap performance versus large cap (active managers tend to have a bias to smaller and mid-size companies – Exhibit 7) and the success of growth/momentum as a style, which has become the semi-consensual positioning in active strategies.

Exhibit 6: European funds can outperform indices

Source: Morningstar. Note: In pounds sterling.

Exhibit 7: Active strategies have a bias to small/mid-caps

Source: Morningstar. Note: Average market cap (euro)

General disclaimer and copyright This report has been prepared and issued by Edison. Edison Investment Research standard fees are £60,000 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison’s policies on personal dealing and conflicts of interest. Copyright: Copyright 2023 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for “wholesale clients” within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument.

New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “FPO”) (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the “publishers’ exclusion” from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person.