“Edison is the go-to for a new investor to get full understanding of the investment case and business. Edison’s distribution reaches investors that we want to connect with directly.”

Where can investors find long-term, inflation-linked income with minimal correlation to economic cycles, backed by government funding and demographic tailwinds? The answer lies in an overlooked corner of the UK market: critical social infrastructure.

What is critical social infrastructure?

Critical social infrastructure refers to the essential facilities, services and systems that support community wellbeing, social cohesion and quality of life. These are distinct from economic infrastructure (such as transport or utilities) and focus on the social fabric of communities. There is a chronic need for investment in infrastructure of all kinds in the UK, and for most other countries too, and private capital is crucial in making this happen.

Within the health and social care sectors, the strong need for investment is driven by demographic trends, the obsolescence of existing facilities and the desire to improve outcomes for all stakeholders. This includes providing more, better and efficient services for the individuals and communities that rely on them and those who work to deliver them. In many cases, investment generates better outcomes at lower costs, an attractive proposition where government funding is involved.

Social impact investors may seek to invest in real estate investment trusts (REITs), which specifically provide investors with exposure to critical social infrastructure. These can be differentiated by a specialism in its chosen segment. For example:

Primary Health Properties (PHP), which recently acquired Assura, is the leading investor in doctors’ surgeries and medical centres in the UK, and it is growing in Ireland;

Target Healthcare REIT (THRL) invests in high-quality residential care and nursing homes. Properties are let to established operators whose residents are primarily privately funded residents; and

Social Housing REIT (SOHO), which owns purpose-built or specially adapted properties that deliver specialised supported housing (SSH), providing community-based homes for some of the most vulnerable members of society (individuals who may have mental health issues, learning difficulties or physical disabilities).

These REITs own the property that supports the provision of care and support, albeit they do not provide those services. Although each REIT is different, they all benefit from similar demographic and structural trends, offer long-term income to investors (with little or no direct exposure to wider economic conditions) and deliver important social benefits.

What drives demand?

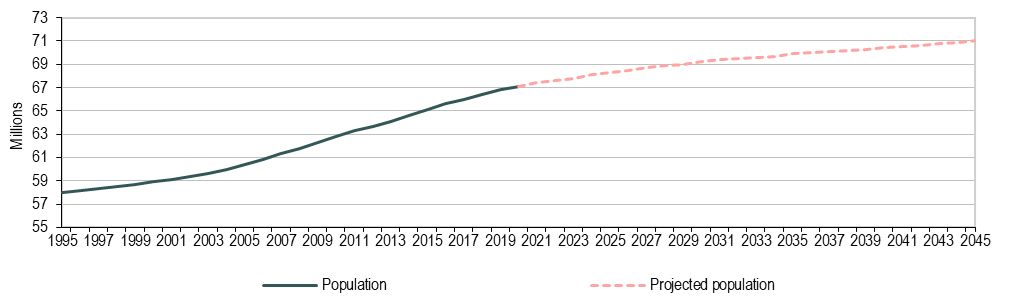

The UK population is growing, and people are living longer, often with complex care needs. Between 2025 to 2050, the overall UK population is projected to grow by 12% (Office for National Statistics, ONS) and the number of people aged 85 and over is forecast to double from 1.78 million in 2020 to 3.61 million by 2050 (ONS). The pressure that this creates for more and better health and social care facilities is not something that can be met by the UK government alone and highlights the need for private capital, presenting a significant opportunity for listed REITs in the sector.

The challenges faced by the NHS were starkly presented in Lord Darzi’s independent investigation report in September 2024, which concluded that the NHS is in a dire condition, requiring not just more funding but a major change in the way it operates. This is reflected the NHS’s 10-year plan which, at its heart, focuses on modern, integrated, local primary healthcare facilities that can better serve patients, with an extended range of medical procedures and preventative services, available locally. This should reduce pressure on hospitals and cost significantly less. Treatment in primary care can be up to 10 times less expensive than hospital treatment but there are too few GPs and up to 50% of the primary care estate is inadequate to support the enlarged range of diagnostic, treatment and preventative care that is required. This creates a clear opportunity for PHP as it owns GP surgeries and primary care centres across the UK and Ireland.

While rising life expectancy is good news, the downside is that most people will spend the last 15 years of their life with some ill health and c 10% of people over 80 have care needs that make it difficult for them to live at home. The Alzheimer’s Society projects that the number of people in the UK with some form of dementia will rise from just under 1 million in 2025 to 1.4 million in 2040. Despite all this, the number of available beds in care and nursing homes has declined over the past 20 years. This only partly reflects an increase in the provision of home care and is explained by new homes entering the sector being offset by the withdrawal of obsolete and inadequate stock; a process that has further to go. THRL’s investment strategy is focused on modern, high-quality, ESG-compliant residential facilities. 84% of its homes have been purpose built since 2010, compared with just 14% for the market, and 100% of its rooms offer full en-suite wet room facilities. Not only are they appealing to residents, but they also support operators in providing better, more efficient and more effective care. As a result, c 80% of the fees earned by THRL’s tenant operators are privately funded or topped up by families or friends, which is less than half the reliance on local authority funding than the market average of c 40%.

For SOHO, demand comes from people with disabilities who need care throughout their lives and are living longer. Some 1.3 million people in England live with a learning disability and the demand for supported housing from this population is projected to rise 33% between 2023 and 2040 (National Housing Federation, NHF). Additionally, as parents age, alternative accommodation is required, with an estimated 167,329 additional supported housing units needed in England by 2040 (NHF). SOHO fills that demand by providing SSH. These, however, are not care homes. A typical SOHO property comprises self-contained flats within one purpose-built building, with full-time care providers providing tailored levels of care and support. Residents live independently in their own homes, some even going out to work, with a care package included to meet their needs. Around 95% of the portfolio is let to approved providers overseen by the Regulator of Social Housing.

Exhibit 1: UK population estimates and projections

Source: ONS. Note: Estimates from mid-1995 to mid-2020 and projections to mid-2045.

How does the funding work?

The demand for health and social care services is non-discretionary and uncorrelated with general economic conditions and, given the essential nature of these services, the properties owned by PHP, THRL and SOHO are fully let on long leases. The leases are ‘triple net’, meaning that tenants are responsible for maintaining and insuring the properties, allowing gross rental income to pass through to earnings. All three of the listed REITs benefit from a supportive demographic tailwind and positive demand-supply characteristics. Key differentiating factors are their differing lease characteristics, especially in respect to rent reviews, as well as tenant quality and the certainty of rent collection (tenant covenant).

PHP has the stand-out tenant covenant, with typically c 90% of rental income paid by governments in the UK and Ireland. In the UK, this is either paid directly by the NHS or indirectly by GP practices, which claim reimbursement from the NHS. The non-NHS share of rents is slightly lower, pending the intended sale of private hospital assets acquired with Assura. On a combined basis, including Assura, the remaining unexpired lease length is 10–11 years. The exceptional quality of PHP’s income supports a higher level of gearing than is typically seen in the wider REIT sector, within a range of 40–50%, which, along with a low-cost ratio, supports profitability.

While PHP has no problem in collecting rents and has delivered consistent earnings and dividend growth, rental income growth has been muted. The good news is that this is accelerating; a trend that should continue. Around two-thirds of rents are reviewed on an open market basis and must be agreed with a district valuer. Over many years, these rents increased modestly, falling behind the rising costs of land and building, which rose materially with inflation. The effect was that the development of new facilities stalled. In H125, completed reviews (including fixed and inflation indexed) were at an average 3.0% per year, with open market reviews again accelerating to 2.3% per year. The rents agreed on new developments are key to setting a more positive tone for open market reviews and a growing recognition that rents must rise (by as much as 20–30%) for much-needed new developments to become viable, suggests the acceleration will continue.

THRL has significant visibility of organic contracted rental growth. All rents are indexed to retail price index inflation (typically capped to a maximum c 4% per year and floored to a minimum c 2%), with a long average remaining lease length of c 26 years. Across the market, care home operators have faced significant challenges in recent years, such as the COVID-19 pandemic, which was quickly followed by inflationary cost pressures. Sector occupancy has recovered from the pandemic and fees have increased significantly. For THRL, this is reflected in average home-level rent cover (a measure of the affordability of rents) of 1.9x, which is the highest level achieved since it launched. The cap on rent increases as inflation spike has benefited near-term affordability and should act to sustain income growth over the long-term.

Investing in newly developed homes is an important element of THRL’s strategy of building and sustaining a high-quality, future-proof portfolio. It takes time for a newly completed home, which is handed over to the tenant, to build occupancy and reach a ‘stabilised’ level of profitability. This is especially true when targeting privately funded residents and the process can take three years or more. Positively, when issues do arise, high-quality assets in the right locations, with positive demand/supply characteristics and prevailing rental levels that are sustainable, will always be attractive to existing or alternative tenants.

Exhibit 2: Mount Court, a supported living house

Source: THRL

The SSH provided by SOHO is a specific type of social housing which is ultimately, but not directly, funded by the UK government. Crucially, it is very different from accommodation for the homeless, the focus of the failed HomeREIT and other types of shorter-term, low-care-need accommodation, such as that for asylum seekers. This is due to HomeREIT’s investments in low-value existing housing for people who would otherwise be homeless, leased to community interest companies (CICs) with little or no trading history. These CICs were unregulated, unlike the registered providers overseen by the Regulator of Social Housing that SOHO works with. The funding relied on housing benefit claims that were often disputed or rejected by local authorities, as properties did not meet the required standards for exempt accommodation. When CICs failed to collect housing benefit or chose not to pay rent, HomeREIT had no recourse to financially robust counterparties. The combination of unregulated tenants, poor-quality assets and an unreliable funding chain led to the collapse of the model. Amid the shocking developments at HomeREIT, the market seemed to lose sight of the fact that, when it is working well, SSH delivers both social benefits and attractive, sustainable cash flows for investors like SOHO. Typical of the sector, SOHO has a long average remaining lease length of 23 years, with all lease payments being inflation linked (mostly to the consumer price index), reviewed annually, and mostly uncapped. The government has pledged to increase social housing benefit, the underlying source of funding, by CPI plus 1% annually over the next 10 years.

But things do not always function smoothly and the weak link is the approved providers that lease the properties from SOHO. To meet the criteria for SSH, these properties must all be significantly adapted to support a high level of third-party care over very long periods. When this is the case, the rent costs of residents are met by the government through housing benefit awards and distributed by local authorities to the approved provider tenants. These approved providers, or housing associations, are regulated by the Regulator of Social Housing. Hence, while government provides funding for SSH, the rent is paid to provider who then pays SOHO.

SOHO has not been immune from tenant problems but, under its new investment manager, Atrato Group, it is making significant progress with some legacy tenant issues, resulting in improved rent collection and a resumption of dividend growth. As with THRL, the best way to mitigate inevitable tenant challenges is a focus on good-quality, well-located properties, let on affordable rents. Atrato’s review of SOHO’s portfolio indicates that mostly all properties are suitable for long-term occupation and use of SSH, which underpins the re-tenanting that has taken place or is underway, and Atrato has committed to taking a more proactive approach to resolving issues as they arise. In addition, Atrato is exploring options to develop lease structuring solutions that would further reduce lessee risk by effectively ring-fencing the rents received by lessees in respect of SOHO properties. This will not happen overnight but, if successful, the proposed measures would greatly enhance the attractiveness of SOHO and the sector more generally to investors and other capital providers and would likely increase the much-needed new housing supply.

Edison’s Insight

Specialist REITs investing in critical social infrastructure offer investors a range of risk: return options for gaining exposure to a structurally supported sector; With significant opportunities for growth, a target of sustainable long-term income and dividend growth and property yields stabilising, REITs like PHP, SOHO and THRL have good potential for capital growth. At a time of heightened economic and political uncertainty, the lack of correlation of the critical social infrastructure sector to the broader economy may well prove attractive.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping us understand which section of the website you find more interesting and useful. See our Cookie Policy for more information.

Strictly necessary and functional

These cookies are used to deliver our website and content. Strictly necessary cookies relate to our hosting environment, and functional cookies are used to facilitate social logins, social sharing and rich-media content embeds.

Advertising

Advertising Cookies collect information about your browsing habits such as the pages you visit and links you follow. These audience insights are used to make our website more relevant.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Performance

Performance Cookies collect anonymous information designed to help us improve the site and respond to the needs of our audiences. We use this information to make our site faster, more relevant and improve the navigation for all users.

Please enable Strictly Necessary Cookies first so that we can save your preferences!