“Edison is the go-to for a new investor to get full understanding of the investment case and business. Edison’s distribution reaches investors that we want to connect with directly.”

Join us for investment knowledge across your choice of sectors and equities.

To continue reading, log in or create a free account below.

Close

Close

Close

Create An Account

If you have an account with us, please click the sign in button below.

Decarbonising the built environment – Steel and cement in focus

Energy & Resources

Decarbonising the built environment – Steel and cement in focus

This report is the second in our series on decarbonising the built environment. While our first report focused on building materials, this report tackles two of the sector’s most critical and emissions-intensive inputs: cement and steel. Together, these materials account for approximately 16% of global CO2 emissions and sit at the heart of modern construction. They are also difficult to decarbonise as their respective production processes are heat intensive, assets are long lived and margins are typically thin. Regulation, customers and capital are increasingly pushing for lower-carbon materials and new technologies are emerging, including clinker substitution and carbon capture in cement, and greater scrap use, electrification and hydrogen-based routes in steel. The investment cycle will mean that the transition takes time, but materials producers will need to adapt.

the key emissions sources in cement and steel production;

the viability and scalability of decarbonisation levers, including green hydrogen, clinker substitution, electrification and carbon capture;

the evolving regulatory and policy landscape in Europe and the UK;

the capital requirements and potential investment implications across both sectors; and

selected company strategies, including Vicat, Hoffmann Green Cement Technologies and Tata Steel.

The built environment accounts for approximately 37–41% of global greenhouse gas emissions, split between operational and embodied carbon. Of the latter, cement and steel dominate. Cement alone contributes c 4–8% of global CO2, while steel adds 7–10%.

Both sectors are hard-to-abate, meaning technical switches are not simple. Challenges include high heat requirements, entrenched legacy assets, fine margins and relatively low product differentiation. However, materials producers will need to adapt. In the UK, building regulations are tightening around embodied emissions. In Europe, the Carbon Border Adjustment Mechanism (CBAM) has entered its 2026 compliance phase, intended to narrow the gap between domestic and imported carbon costs.

This report considers both supply-side decarbonisation pathways, such as carbon capture, usage and storage (CCUS), green hydrogen and energy efficiency, and demand-side levers, such as reduced material use, clinker substitution and steel circularity. It also includes profiles of selected producers and the main targets and projects they have set out publicly.

Context

Introduction

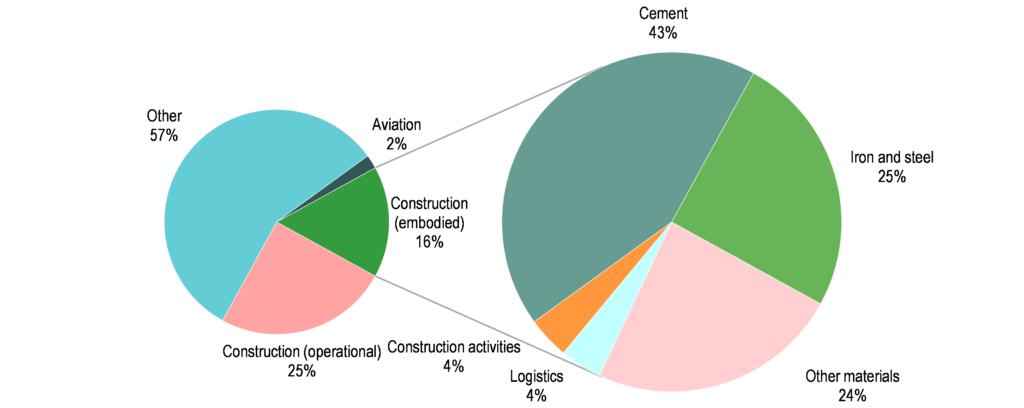

In 2020, the sourcing and manufacturing of materials accounted for approximately 92% of global embodied carbon emissions in the construction industry (ie the carbon emitted during the production of these building materials), according to a 2023 Shell report. Cement was the largest contributor at 43%, followed by steel at 25%, and other materials such as glass, timber and aluminium collectively accounted for 24%.

It is unsurprising that cement and steel are so dominant, as both materials are core to modern construction (notably steel-reinforced concrete usage in high-rise dwellings). The decarbonisation of the steel and cement industries is, therefore, at the forefront of the construction and materials sector due to their high energy intensity and long asset lifetimes. However, it is important not to overlook emissions attributed to logistics and general construction activities, which accounted for 8% of the embodied carbon emissions in 2020, primarily due to on-site equipment usage. Addressing all areas across the construction and materials value chain is essential to achieve the industry’s net-zero goals by 2050.

Exhibit 1: Global CO2 emissions (2020) – embodied construction CO2 emissions (2020)

Source: International Energy Agency, Shell, Edison Investment Research

Cement

Emissions breakdown and pathways

Given the scale of cement emissions (c 7–8% of global CO2), low-carbon cement and concrete pathways are a necessary part of the decarbonisation of the built environment. In practice, the main methods of achieving decarbonisation include:

Sustainable energy sources: reducing fossil fuel use in heat and power, including greater use of alternative fuels and lower-carbon electricity where available.

Cleaner clinker production: process and kiln upgrades that reduce energy intensity and improve heat efficiency.

Clinker reduction: reducing the clinker factor through supplementary cementitious materials (SCMs) and new binders, without compromising performance.

CCUS: addressing process emissions that cannot be avoided through fuel switching or efficiency.

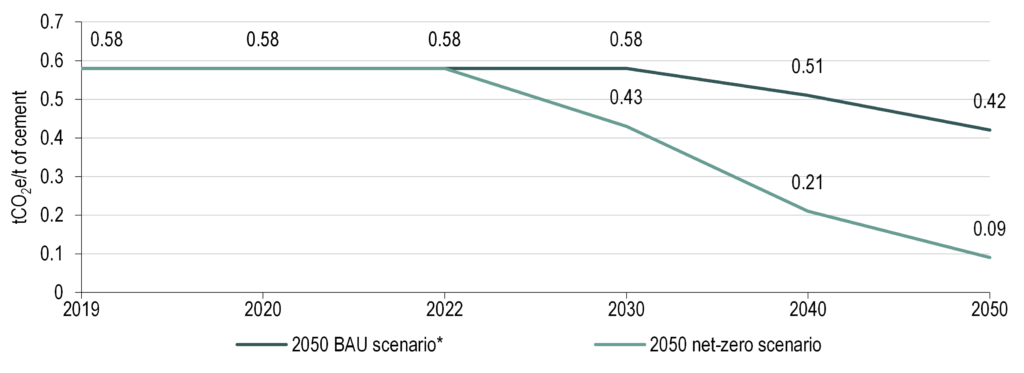

The cement industry’s stated energy transition goals are to reduce emissions intensity by c 25% by 2030 and achieve net zero by 2050 (source: Global Cement and Concrete Association). Progress to date has been slow. The World Economic Forum’s cement tracker notes that absolute CO2 emissions declined by less than 1% over the last four years, even as global production increased. If the sector’s targets are to be met, it will need to adopt proven measures now (eg clinker reduction, fuels, efficiency), while building a credible route for the harder, residual emissions, most obviously through CCUS.

Exhibit 2: Emissions intensity trajectory, net-zero versus business-as-usual scenario

Source: The World Economic Forum, Edison Investment Research. Note: *BAU, business as usual. tCO2, tonnes of carbon dioxide.

Infrastructure and capital required for net-zero 2050

Cement emissions can be split into two broad categories:

Energy-related emissions from fuels and electricity used in kiln heating, grinding and wider plant operations.

Process emissions from limestone calcination during clinker production, which releases CO2 as part of the chemical reaction.

Around 60–70% of cement’s CO2 footprint is typically associated with calcination during clinker production, with the remaining 30–40% linked to the energy required to reach high kiln temperatures (c 1,450°C). The main decarbonisation options are:

Clinker substitution: reducing the clinker factor through SCMs such as fly ash, slag and calcined clays. The availability of some SCMs is tightening as coal generation declines and some industrial by-products become scarcer.

Alternative fuels: substituting coal with waste-derived fuels or biomass. In Europe, substitution rates can exceed 40% in some markets.

CCUS: the most direct route to tackling process emissions from calcination, but it is constrained by cost, permitting and the need for shared CO2 transport and storage infrastructure.

Electrification: the technology is still in early stages for high-heat processes, with feasibility likely to depend on power prices and grid capacity.

New chemistries and materials: new binders and concrete additives are being developed but scaling requires standards, certification and consistent performance data.

These represent a range of options, probably deployable at different times. Early options are likely to be clinker reduction, alternative fuels and efficiency, while longer-dated solutions are developed for the residual emissions, most obviously through CCUS and the infrastructure that supports it.

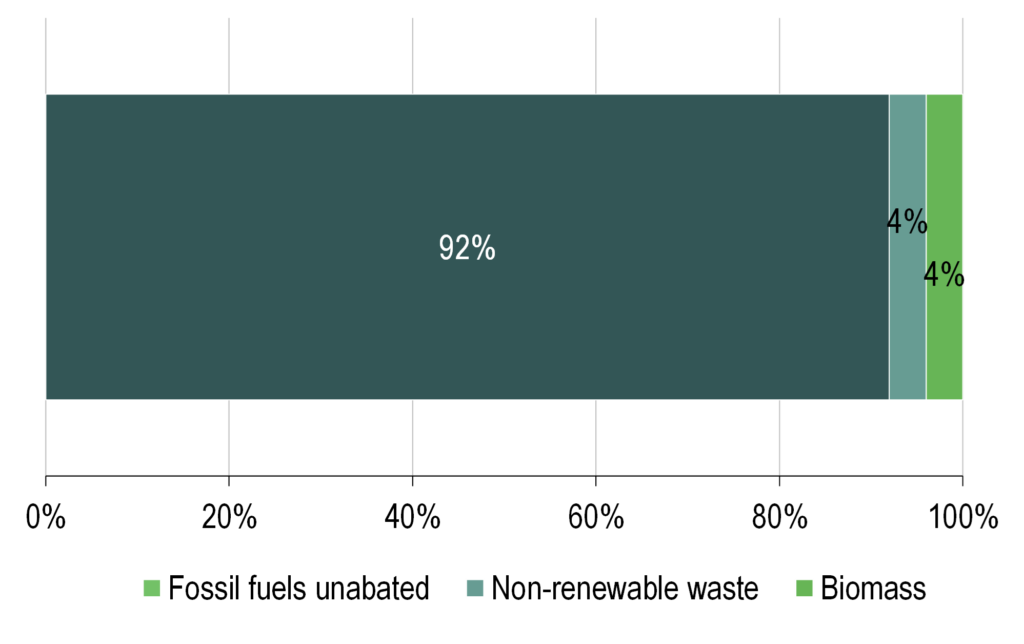

Exhibit 3: 2020 cement production fuel mix

Source: The World Economic Forum, Edison Investment Research

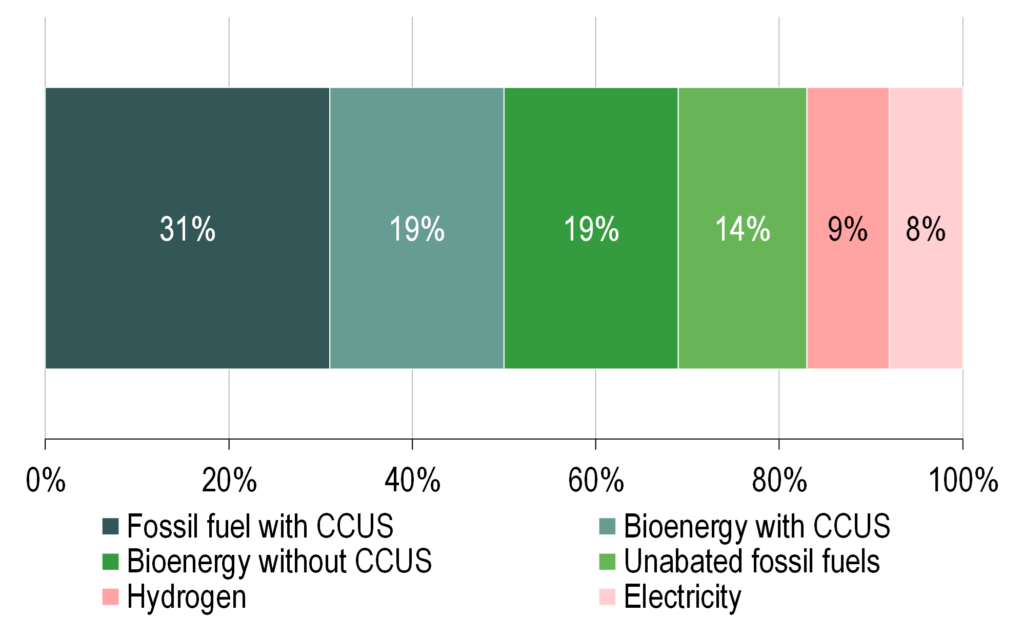

Exhibit 4: 2050 cement production fuel mix (net-zero scenario)

Source: The World Economic Forum, Edison Investment Research

Policy and investment landscape

The cement sector operates within a tightening regulatory framework. The fourth phase of the EU Emissions Trading System (ETS) is already applying increasing carbon costs. The UK ETS, though less mature, may converge with EU pricing over time. Meanwhile, the EU’s CBAM has entered its 2026 compliance phase and is intended to price embedded carbon on imports, narrowing the gap for European producers facing higher decarbonisation costs.

Public finance will also be important. Europe’s Innovation Fund is expected to reach around €40bn by 2030 (depending on the carbon price), supporting industrial decarbonisation including cement CCUS projects. In the UK, government support through the Industrial Energy Transformation Fund and the Net Zero Hydrogen Fund could accelerate fuel switching and early electrification pilots.

Risks do remain and public resistance to carbon capture and storage (CCS) infrastructure, permitting delays and uncertainty around green product standards could all slow progress. Importantly, clarity around long-term carbon pricing and Scope 3 Standard accounting rules will be essential for cement producers to demonstrate their progress to investors.

Steel

Primary versus secondary steel and emissions profiles

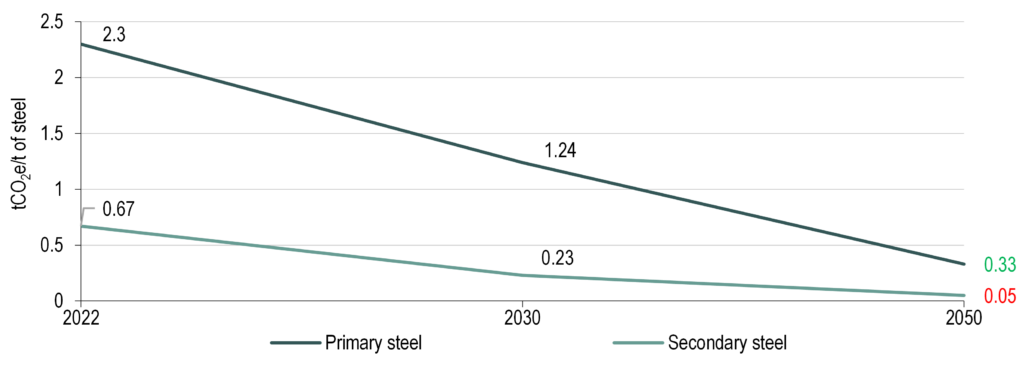

Exhibit 5: Emissions intensity trajectory for primary and secondary steel

Source: The World Economic Forum, Edison Investment Research. Note: Red number is the net-zero scenario and green number is the business-as-usual scenario. tCO2 is tonnes of carbon dioxide.

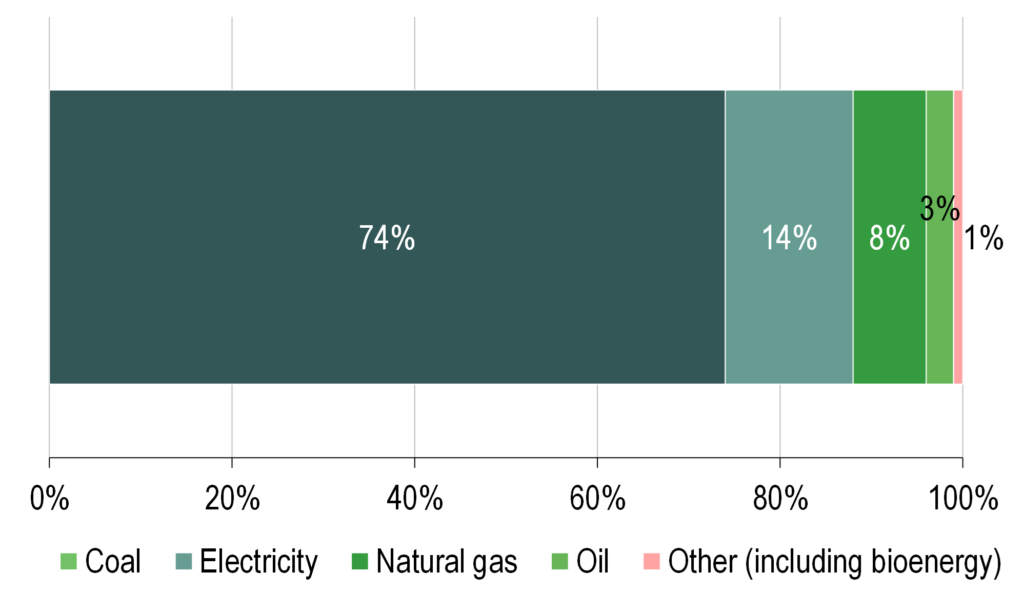

Exhibit 6: 2021 steel production fuel mix

Source: The World Economic Forum, Edison Investment Research

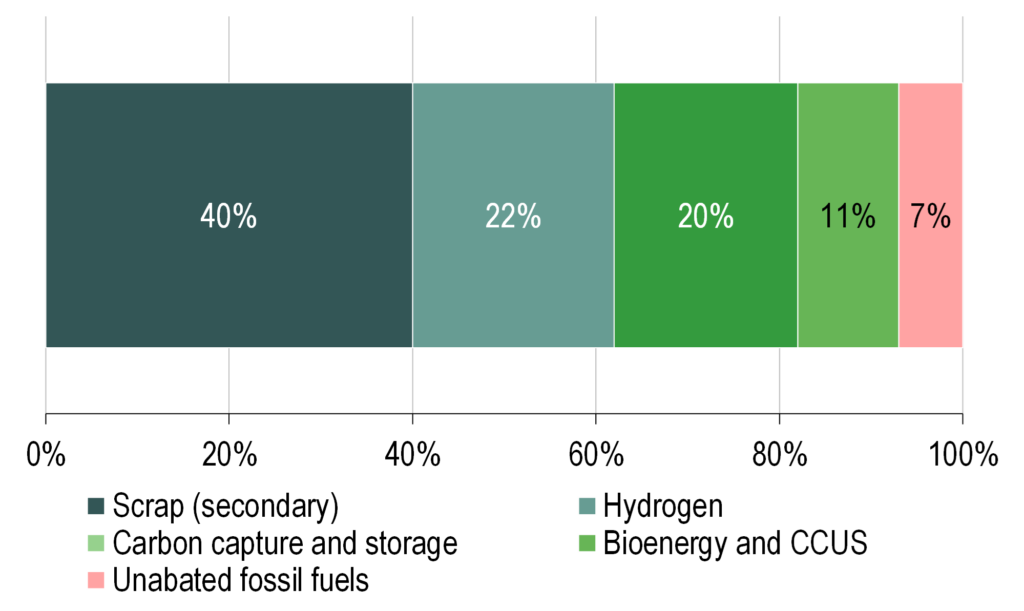

Exhibit 7: 2050 estimated steel production fuel mix

Source: The World Economic Forum, Edison Investment Research

Like cement, steel is a key global challenge in decarbonising building materials, accounting for c 7–9% of global CO2 emissions. It is an inherently high-emissions industry at present. Global crude steel production totalled 1.9Gt in 2025, of which China accounted for 961Mt (just over half). Steel demand is expected to grow over time but the pace and shape of that growth matters, particularly given the sector’s long-lived assets.

Steel is produced from primary sources (iron ore, which is principally iron oxide minerals) and the remelting of scrap steel. Remelting scrap steel in electric arc furnaces (EAFs) is far lower in emissions, particularly if green power is used. Iron ore needs reduction from an oxide to a metallic state and the common method for doing this is using coking coal, where the carbon content produces carbon dioxide. EAFs account for c 29% of global steel production but this method is limited by scrap availability (c 75–80% of steel is recycled). Steel is also often used in very long-life applications (such as construction), which means scrap steel is not readily available for use (in China, secondary steelmaking accounts for just 10% of the total). Using scrap to decarbonise steelmaking globally is, therefore, not possible.

Primary steelmaking (ie from iron ore) needs decarbonising. One possibility is to use CCS alongside traditional blast furnace operations. CCS is a viable route and relatively cost effective, but it does require storage solutions for CO2 that are near steel plants and are cost effective.

Another alternative is to avoid CO2 entirely at the source of iron production. This can be done by substituting hydrogen as the reduction agent or, in chemical terms, from carbon-based reductants (2Fe2O3 + 3C → 4Fe + 3CO2) to hydrogen reductants (Fe2O3 + 3H2 → 2Fe + 3H2O, FeO +H2 → Fe + H2O). This requires direct reduced iron (DRI) technology, which is proven using natural gas and produces metallic feed that can supplement scrap in EAFs. Green steel will be more expensive to produce and will, therefore, require a combination of catalysts, including direct subsidies, a green steel premium and border measures to support the competitiveness of higher-cost production methods against imports from higher-emissions producers. Adoption of this looks possible, but it is a slow process that is more likely to accelerate during the 2030s. Consumers will ultimately bear much of the cost, although steel is a relatively low-value product ($500–1,000/t). A green steel premium in the order of $100/t could be sufficient to incentivise change, with a relatively modest impact on the total cost of many end-products.

There do not appear to be many pure vehicles for investing in green steel. The adoption process appears to be slow, led mainly by incumbent steelmakers and dependent on policy initiatives that mostly take effect next decade.

As set out above, the key decarbonisation question is how quickly the sector can shift from blast furnace-basic oxygen furnace (BF-BOF) towards scrap-EAF and DRI-EAF routes, and what that implies for power, hydrogen and scrap. Primary methods involve BFs and BOFs using iron ore and coking coal. They emits c 1.8–2.2t CO2 per tonne of steel and accounts for c 70% of global production. Secondary methods include EAFs, which melt scrap steel. If powered by renewable energy, emissions can fall below 0.4t CO2 per tonne of steel. However, scrap availability and quality are limiting factors.

The decarbonisation of primary steel hinges on several pathways:

CCUS retrofits to existing blast furnaces.

Hydrogen-based DRI technology followed by EAF processing. This is the leading long-term pathway to near-zero steel.

Biomass can be used as a reductant. It is viable in some geographies but limited by feedstock availability.

Efficiency upgrades such as burden mix optimisation, smart fuel injection and off-gas reuse could cut emissions by 10–20%.

The EU has emerged as the testbed for green steel. Companies like SSAB, ArcelorMittal and Tata Steel are piloting hydrogen-DRI projects. However, capital costs are high and some estimates for green steel are up to €300bn in Europe alone to meet 2050 targets. Success will depend on renewable electricity access, hydrogen cost curves and consumer willingness to pay green premiums.

Transition technologies

The technology pathway for steel decarbonisation is developing around three main routes:

Hydrogen-based DRI technology and EAFs: this is one of the most credible routes to near-zero steel. Iron ore is reduced using hydrogen, not coal, producing water instead of CO2. The DRI is then melted in an EAF. European companies such as SSAB, Stegra and ArcelorMittal are pioneering these projects. However, hydrogen supply, electrolyser capacity and green power costs remain bottlenecks.

Scrap-EAF scaling: secondary steel from scrap is inherently lower-carbon. However, supply of high-grade scrap is tight, especially for flat products like automotive steel. Blending with DRI (from hydrogen or gas) is a pragmatic interim solution.

CCUS retrofits for BF-BOF: while not zero-carbon, CCUS can deliver up to 60% emissions reductions. ArcelorMittal is piloting CCUS at several European sites, though technical and permitting hurdles remain significant.

It is possible that green hydrogen prices will need to fall as low as €1–2/kg to reach economic parity with traditional steelmaking. This, in turn, hinges on low-cost renewables and electrolyser scaling. The EU ETS’s prices, which could rise to over €100/t CO2 by 2030, will help close the cost gap.

In our view, it is likely that steel decarbonisation will favour:

vertically integrated producers with access to scrap or iron ore;

regions with cheap green electricity; and

customers willing to pay a green premium (eg automotive, consumer goods).

Europe is leading the transition, but investment decisions made this decade will define competitive dynamics for 2040 and beyond.

Hubs and value chain reconfiguration

Steel’s decarbonisation challenge is as much logistical as technological because green hydrogen and low-carbon power will not be equally available across geographies. As such, global supply chains will need to be reconfigured.

One response is the emergence of green steel hubs, which are locations optimised for hydrogen-based DRI production using cheap renewables and high-grade ore, often located near ports or in resource-rich regions. Europe will be a key consumer but not necessarily the cheapest place to make green iron. Hot briquetted iron exports from the Middle East, South America and Australia may increasingly supply European EAFs.

Steel has long been an industry where location in terms of strategy matters. In a decarbonising world, however, the following geographic factors could come into play:

Ore-rich, low-power-cost regions could become upstream producers (eg Saudi Arabia, Brazil, Western Australia).

Traditional integrated producers must reconfigure or risk becoming stranded assets.

Scrap-rich urban markets could gain value as circularity increases.

It is possible that the innovators may not be the current major players but new entrants that are able to navigate where carbon costs can be minimised.

Policy and investment landscape

Steel decarbonisation remains a major unresolved issue and a solution is being pushed by a combination of regulatory, financial and industrial policy initiatives. The EU ETS and the CBAM have already shifted incentives across the bloc. The CBAM is particularly impactful for steel, introducing embedded carbon pricing on iron and steel imports from 2026.

National support mechanisms also play a central role. In Germany, the climate and transformation fund is one option being used to support industrial decarbonisation, including hydrogen-related projects involving producers such as Salzgitter and ArcelorMittal. Sweden is aligning policy incentives with green production standards to accelerate Stegra’s buildout. In the UK, government support for the EAF transition at Port Talbot and CCUS clustering in Teesside represent early steps in a broader industrial transformation agenda.

This is relevant to investors as alignment with climate goals is a factor now being considered in lending and investment decisions. Firms that cannot show credible decarbonisation strategies risk facing a higher cost of capital or tighter funding conditions. In contrast, early movers can access funding such as green bonds, concessional capital and innovation subsidies.

What investors should watch

Cement and steel are globally important for net zero as they are large sources of emissions and difficult to abate. Investors that consider sustainability do need to appreciate the scale and importance of these industrial sectors. Decarbonisation will depend on three things: deployable technology, enabling infrastructure (power, hydrogen, CO2 transport and storage) and policy frameworks that help producers with higher costs.

For cement, firms commercialising zero-clinker products or CCUS-integrated kilns could benefit from early regulatory approvals or consumer preferences for green materials. For steel, players that secure access to green hydrogen and renewables, and integrate them through hydrogen-DRI and EAF pathways, are positioned to capture any emerging green product pricing premiums, particularly in automotive, construction and packaging markets.

Investors should look for companies that have:

credible transition plans with interim targets and funded capex pipelines;

exposure to industrial clusters with clear infrastructure plans;

a feedstock advantage (scrap access, iron ore or a secure DRI supply); and

balance sheet flexibility to navigate carbon pricing and policy cycles.

Company showcase: Cement

Breedon Group (LSE: BREE): Breedon’s decarbonisation focus is mainly operational, given its footprint in cement, aggregates, asphalt and ready-mix. The group has set out a pathway to net zero by 2050 from a 2022 baseline and has Science Based Targets initiative (SBTi)-verified near-term targets for 2030. In cement, Breedon’s Hope Cement Works is a partner in the Peak Cluster CCUS project, which is intended to enable CO2 capture and transport from industrial sites in the Peak District area. Alongside this, Breedon highlights levers such as fuel switching, efficiency and product optimisation, and it markets lower-carbon concrete and block products that can incorporate recycled or secondary aggregates. Targets: Breedon has SBTi-verified 2030 targets and a net-zero 2050 target across the value chain.

Cemex (BMV: CEMEXCPO): Cemex’s Future in Action programme frames its decarbonisation agenda around lower-clinker products, operational efficiency and partnerships, alongside longer-dated options, such as carbon capture. In the UK, Cemex has been developing a carbon upcycling pilot at its Rugby cement plant to convert captured CO2 into a cement additive, backed by public innovation funding. Through Cemex Ventures, the group has also invested in Synhelion, which is developing solar heat applications relevant to high-temperature industrial processes. Cemex has published 2030 climate targets, including a 40% reduction in direct CO2 emissions versus a 1990 baseline, alongside a net-zero ambition for 2050. It is a founding member of the First Movers Coalition. Targets: Cemex has published 2030 climate targets and a net-zero 2050 ambition under its Future in Action programme.

Heidelberg Materials (XETRA: HEI): A first mover in industrial-scale CCUS, Heidelberg Materials brought Brevik CCS in Norway into operation in June 2025. The plant is designed to capture around 400,000t CO2 per year and is part of Norway’s Longship CCS chain. The company is also advancing project Leilac-2, which aims to capture CO2 from clinker production with minimal disruption. Beyond CCUS, Heidelberg Materials is using digital systems to support efficiency and clinker substitution and its 2030 CO2 reduction targets have been validated by the SBTi. Targets: Heidelberg Materials has publicly stated 2030 carbon reduction targets (validated by the SBTi under its 1.5°C framework) and a net-zero 2050 ambition.

Hoffmann Green Cement Technologies (PAR: ALHGR): Hoffmann Green markets 0% clinker cements, including H-P2A and H-EVA, and positions its approach around low-energy, cold manufacturing routes versus traditional clinker-based cement. The company operates two production units at Bournezeau, France, powered by a solar tracker park and has disclosed plans for a third factory in the Auvergne-Rhône-Alpes region with construction scheduled for 2027–28, which it states would take total production capacity to around 1.0Mtpa. Hoffmann Green has also reported increasing commercial volumes in 2025 and continues to announce partnerships and certifications as it seeks to broaden market acceptance. Targets: Hoffmann Green Cement’s strategy is to contribute to carbon neutrality by 2050 and publishes product-level decarbonisation claims for its clinker-free cements.

Holcim (SIX: HOLN): As the world’s largest cement company, Holcim has committed to invest CHF2bn in carbon capture technologies by 2030. Its ECOPact low-carbon concrete range includes mixes that can deliver up to 90% lower embodied carbon, depending on specification and baseline. Holcim is developing its Carbon2Business CCUS project at Lägerdorf in Germany, targeting capture of more than 1.2Mt CO2 per year and net-zero cement production from 2029, supported by an EU Innovation Fund grant. Elsewhere, Holcim has partnered with Carbon Clean on a CCUS pilot at its Carboneras plant in Spain and has participated in a US carbon capture feasibility study at its Portland cement plant in Colorado with Svante and Oxy Low Carbon Ventures (subsidiary of Occidental Petroleum Corporation). In parallel, its subsidiary Geocycle operates a waste co-processing platform that supports fuel and raw material substitution in cement plants. Targets: Holcim has publicly stated 2030 and 2050 climate targets, which have been validated by the SBTi.

Vicat (PAR: VCT): Vicat’s decarbonisation work at Montalieu-Vercieu, France, includes a mix of fuel switching and carbon capture development. The group’s Meteor programme aims to increase alternative fuel substitution at the site and it has also launched the Vicat Advanced Industrial Alliance CCUS project at Montalieu-Vercieu, targeting c 1.2Mt CO2 per year, subject to permitting and investment decisions. Vicat is also involved in the Hynovi project with Hynamics (a subsidiary of EDF Group), which links low-carbon hydrogen with captured CO2 to produce e-methanol. Alongside these projects, Vicat positions efficiency measures and its circular economy offer as part of its wider approach. Targets: Vicat has a stated ambition of net-zero emissions by 2050 and has published 2030 CO2 reduction targets for the group.

Company showcase: Steel

ArcelorMittal (AMS: MT): The world’s second-largest steelmaker, ArcelorMittal has set out a European decarbonisation plan targeting a 35% CO2 reduction by 2030 and an ambition to be carbon neutral by 2050. It has previously indicated that delivering its 2030 emissions reduction programme implies investment of c $10bn. Flagship European projects include hydrogen-based DRI development at Hamburg, Germany, and carbon capture pilots at sites including Ghent, Belgium, and Dunkirk, France. The group is also progressing a phased shift towards EAF capacity where policy support and infrastructure allow, alongside work on smart carbon technology and customer offtake discussions for lower-carbon steel. Targets: ArcelorMittal has stated a 35% CO2 reduction target by 2030 and an ambition to be carbon neutral by 2050.

Liberty Steel Group (private company, part of GFG Alliance): Liberty’s GREENSTEEL’s strategy is centred on scrap-based EAF steelmaking, alongside renewables and hydrogen where available. In the UK, Liberty’s speciality steel unit in South Yorkshire includes the Rotherham EAF, which has been described as the UK’s largest, although operations and the ownership structure have been disrupted by prolonged financial stress and subsequent government intervention in 2025. In Australia, Liberty has set out plans to develop a lower-carbon pathway at Whyalla, based on an integrated DRI-EAF route intended to transition towards green hydrogen over time, subject to infrastructure and financing. Targets: As a private company, Liberty does not publish the same standardised 2030 and 2050 targets as listed peers, although it has previously stated a carbon neutral by 2030 ambition under its GREENSTEEL strategy.

Salzgitter (XETRA: SZG): Salzgitter’s SALCOS programme is the group’s main transition route, built around a staged move from BF-BOF towards direct reduction and EAF steelmaking. The first stage includes a direct reduction plant, new EAF capacity and a 100MW electrolysis plant to supply hydrogen. Salzgitter has secured German federal and state funding for the initial build-out and has set out an ambition to complete the site transformation by the end of 2033, with emissions reductions of over 95% once fully implemented. Targets: Salzgitter has published near-term climate targets and a net-zero 2050 target for total CO2e emissions across the value chain.

SSAB (STO: SSAB-B): SSAB is progressing one of the more advanced transition programmes among European steelmakers through HYBRIT, its joint venture with LKAB and Vattenfall. The group has already made trial deliveries of fossil-free steel to the Volvo Group and is now executing a phased conversion of its Nordic production system. This includes the transformation of Oxelösund in Sweden (EAF-based production), a planned fossil-free mini-mill at Luleå in Sweden and a later project at Raahe in Finland, with timing linked to power and grid infrastructure as well as financing capacity. Targets: SSAB’s stated ambition is to largely eliminate CO2 emissions from its own operations by around 2030 and to be fossil-free by 2045.

Stegra (formerly H2 Green Steel, private company): Stegra is developing a large greenfield steel plant at Boden in northern Sweden, designed to integrate hydrogen electrolysis, DRI and EAF steelmaking on one site, supplied by renewable electricity. The company has secured large-scale project financing (including EU Innovation Fund support) and has stated an initial production plan of around 2.5Mtpa of steel, with start-up targeted in 2026. Commercially, it has announced multi-year offtake agreements with industrial customers including Mercedes-Benz, Scania and Electrolux. Targets: As a private company, Stegra does not publish the same standardised 2030 and 2050 emissions targets as listed peers. Its public disclosures focus on project start-up timing and planned capacity.

Tata Steel (NSE: TATASTEEL): Tata Steel is pursuing two decarbonisation tracks in Europe. In the UK, it has agreed a £1.25bn investment package (including up to £500m of UK government support) to build a new 3.2Mtpa EAF at Port Talbot, with commissioning targeted for late 2027 or early 2028. In the Netherlands, Tata Steel Nederland’s green steel plan is structured around replacing one BF route with DRI-EAF, designed to run initially on natural gas and later switch to biomethane and hydrogen as supply and economics allow, with CCS also positioned as an interim lever for residual emissions. Targets: Tata Steel’s European businesses have published 2030 CO2 reduction goals and an ambition to be CO2-neutral by 2045 (with the exact baselines and metrics varying by business unit).

voestalpine (VIE: VOE): voestalpine’s greentec steel programme is its main decarbonisation pathway, combining near-term electrification with longer-term process change. The group has approved the installation of one EAF at each of its Linz and Donawitz sites in Austria, at a cost of c €1.5bn, with both scheduled to enter operation in 2027, initially running in a hybrid configuration alongside existing assets. voestalpine has also been involved in hydrogen pilot work at Linz, including a 6MW green hydrogen facility as it tests how hydrogen could integrate into steelmaking over time. Targets: voestalpine has stated an ambition to reach net zero CO2 emissions by 2050, with interim reductions driven by the greentec steel conversion programme.

Redesigning immunity: The next frontier in immuno-oncology

Immuno-oncology (IO) has transformed cancer treatment, shifting the paradigm from cytotoxic and targeted therapies to immune-driven disease control (harnessing the body’s own immune system). Immune checkpoint inhibitors (ICIs), CAR-T cell therapies and cancer vaccines have produced durable responses in defined patient populations; however, the first wave of IO is approaching clinical and commercial saturation. ICI response rates remain limited to c 20–40% in solid tumours, while CAR-T therapies, despite curative potential in haematological malignancies, are restricted by high cost, complex manufacturing, immune-related toxicities and lower efficacy in solid tumours. Earlier cancer vaccines also failed to show consistent benefit. These constraints are driving next-generation approaches, focused on platforms that actively programme immune responses, rather than simply releasing inhibitory checkpoints. This report examines key innovation vectors shaping the next phase for this sector.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping us understand which section of the website you find more interesting and useful. See our Cookie Policy for more information.

Strictly necessary and functional

These cookies are used to deliver our website and content. Strictly necessary cookies relate to our hosting environment, and functional cookies are used to facilitate social logins, social sharing and rich-media content embeds.

Advertising

Advertising Cookies collect information about your browsing habits such as the pages you visit and links you follow. These audience insights are used to make our website more relevant.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Performance

Performance Cookies collect anonymous information designed to help us improve the site and respond to the needs of our audiences. We use this information to make our site faster, more relevant and improve the navigation for all users.

Please enable Strictly Necessary Cookies first so that we can save your preferences!