ESCT should benefit when investors less risk averse

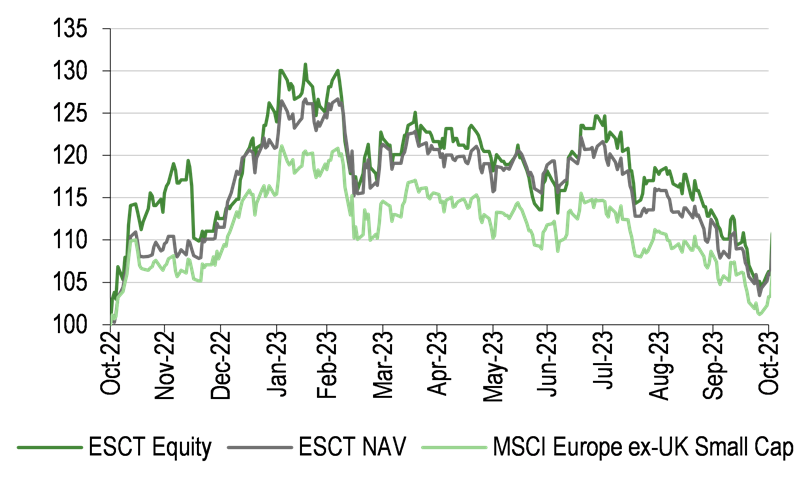

ECST is a good route through which to participate in a recovery in European small-cap stocks. Any capital upside should be enhanced by a relatively high c 15% level of gearing. The trust has definitely proved its worth, with outperformance versus its benchmark, and best in sector NAV total returns, over the last one, three, five and 10 years.

ESCT’s upside/downside capture analysis

The trust’s upside/downside capture is shown in Exhibit 1. With an upside capture of 114%, this suggests that ESCT is likely to outperform in months of rising share prices, while its downside capture of 110% implies it will underperform, but to a modestly lesser degree in periods of share price weakness. The step-up in the downside capture between Q417 and Q120 reflects a sustained period of underperformance, which has been more than made back (see front-page chart).

Exhibit 1: ESCT’s upside/downside capture

|

|

Source: Refinitiv, Edison Investment Research. Note: Cumulative upside/downside capture calculated as the geometric average NAV total return (TR) of the fund during months with positive/negative reference index TRs, divided by the geometric average reference index TR during these months. A 100% upside/downside indicates that the fund’s TR was in line with the reference index’s during months with positive/negative returns. Data points for the initial 12 months have been omitted in the exhibit due to the limited number of observations used to calculate the cumulative upside/downside capture ratios.

|

ESCT’s portfolio of high-quality, attractively valued securities is diversified by stages in a company’s life cycle:

■

Early cycle – improving or forecast improvement in return on invested capital (ROIC) with strong (typically above 10%) sales growth (c 5% of the fund at end-September).

■

Quality growth – consistent ROIC above the cost of capital and above-GDP growth organically or via mergers and acquisitions (c 38%).

■

Mature – consistent ROIC at or around the cost of capital (c 24%).

■

Turnarounds – ROIC below the cost of capital, or significantly below industry peers, with forecast ROIC improvement (c 33%).

Exhibit 2: ESCT’s portfolio metrics (at 30 September 2023)

|

ESCT |

MSCI Europe ex UK Small Cap Index |

Dividend yield forecast (%) |

3.7 |

3.7 |

P/E forecast (x) |

10.6 |

11.2 |

Return on equity (%) |

14.7 |

12.3 |

Three-year historical EPS growth (%) |

21.3 |

17.3 |

Next 12 months forecast EPS growth (%) |

15.6 |

21.3 |

Net debt/EBITDA (x)* |

1.5 |

1.8 |

Source: ESCT. Note: *Data at 31 March 2023.

Compared with its benchmark, the trust’s portfolio has a lower forward P/E multiple and a higher return on equity. It has a lower forecast earnings growth and less leverage.

Portfolio is geared to an economic recovery

A direct comparison between ESCT’s sector exposure and that of its benchmark, the MSCI Europe ex UK Small Cap Index, is not possible as the classifications differ. However, broadly, the fund is geared to an economic recovery with overweight positions in industrials, consumer discretionary and IT, while its underweight positions include the healthcare and consumer staples sectors, both of which are defensive.

Exhibit 3: Portfolio geographic (left) and sector (right) exposure (at 30 September 2023)

|

and sector (right) exposure (at 30 September 2023)")

|

and sector (right) exposure (at 30 September 2023)")

|

Source: ESCT, Edison Investment Research

|

Exhibit 3: Portfolio geographic (left) and sector (right) exposure (at 30 September 2023)

|

|

|

Source: ESCT, Edison Investment Research

|

Exhibits 3 and 4 illustrate ESCT’s geographic and sector breakdowns. Looking at the trust’s changes in geographic exposure in the 12 months to end-September 2023, there was a larger weighting to Germany (+3.7pp) with a lower allocation to ‘other countries’; this cannot be quantified as Norway was not broken out separately at the end of September 2022.

The largest changes in terms of sector exposures were higher weightings in consumer services (+2.2pp) and real estate (+2.1pp) with a lower exposure to consumer goods (-3.9pp). Overall, ECST’s portfolio structure has not changed markedly over the year to 30 September 2023.

Exhibit 4: Portfolio geographic and sector exposure (% unless stated)

Geography |

Portfolio end-Sep 2023 |

Portfolio end-Sep 2022 |

Change (pp) |

|

Sector |

Portfolio end-Sep 2023 |

Portfolio end-Sep 2022 |

Change (pp) |

Germany |

17.6 |

13.9 |

3.7 |

|

Industrials |

39.1 |

38.3 |

0.8 |

France |

13.6 |

15.0 |

(1.4) |

|

Consumer services |

12.3 |

10.1 |

2.2 |

Sweden |

11.6 |

9.8 |

1.8 |

|

Technology |

10.5 |

11.2 |

(0.7) |

Italy |

9.7 |

9.6 |

0.1 |

|

Core financials |

7.5 |

8.8 |

(1.3) |

Netherlands |

9.6 |

8.3 |

1.3 |

|

Consumer goods |

7.3 |

11.2 |

(3.9) |

Switzerland |

8.8 |

8.2 |

0.6 |

|

Basic materials |

6.5 |

5.2 |

1.3 |

Spain |

5.6 |

6.5 |

(0.9) |

|

Financial services |

5.2 |

6.6 |

(1.4) |

Belgium |

4.2 |

4.3 |

(0.1) |

|

Energy |

4.1 |

3.6 |

0.5 |

Norway |

3.0 |

N/S |

N/A |

|

Healthcare |

3.1 |

2.3 |

0.8 |

Finland |

2.7 |

4.2 |

(1.5) |

|

Real estate |

3.1 |

1.0 |

2.1 |

Other |

13.6 |

20.0 |

(6.4) |

|

Utilities |

0.7 |

1.7 |

(1.0) |

|

|

|

|

|

Telecoms |

0.5 |

0.0 |

0.5 |

|

100.0 |

100.0 |

|

|

|

100.0 |

100.0 |

|

Source: ESCT, Edison Investment Research. Note: Numbers subject to rounding. N/S is not stated separately.

Recent portfolio activity

In September 2023, Soitec re-entered the portfolio. It is a leading provider of silicon-on-insulator wafers for the semiconductor industry. The manager considered that the company had become attractively valued following a period of share price weakness. However, he is mindful that other areas of the industry look overvalued given expected earnings downgrades. The holding in Meyer Burger Technology was sold, as its business remains under pressure despite the company’s position as the only Europe-based manufacturer of solar cells and modules.

Merlin Properties, a Spanish real estate company, was added to the portfolio in August 2023 as Spanish inflation has declined more than in other Western European economies. This could benefit the office sector by a reduction in vacancy rates. Merlin is also building out its data centres, which could become an income generator in 2024. Sales included Barco (a Belgian screen manufacturer) and HusCompagniet (a Danish homebuilder).

In July 2023, the manager initiated a position in Borregaard, which is a biochemicals producer, as he believes that some speciality cellulose prices will normalise this year. The CTS Eventim (German concert ticket platform) position was sold to lock in profits.

Potential for European small-cap recovery

Over the last three years, European small-cap stocks have given back some of their long-term outperformance versus their large-cap peers (Exhibit 5). Longer-term data from ESCT show that in the prior two decades, European small-cap stocks outperformed in 14 out of 20 years, and in one of the six years where they lagged the performance differential to large-cap European stocks was negligible. Investors have had significant issues to grapple with in recent years including the global COVID-19 pandemic, war in Ukraine and now in the Middle East, rising inflation, higher interest rates and the increased risk of recession, so it is unsurprising that there have been higher risk aversion and lower appetite for small-cap stocks. Also, rising oil prices have been beneficial for energy stocks, while higher interest rates have boosted bank net interest margins. Both energy and bank stocks have greater representation in large-cap rather than small-cap indices.

History shows that stock markets move in cycles, so when there is less volatility, investors are likely to move back down the capitalisation spectrum in search for higher growth opportunities. European small-cap stocks benefit from global GDP growth, generally have strong balance sheets and are more likely to be bid for than larger companies, while the investment universe is larger and less well covered, offering the potential for undervalued securities.

Exhibit 5: Performance of MSCI Europe ex UK small- vs large-cap indices (last 10 years)

|

")

|

Source: Refinitiv, Edison Investment Research

|

European small caps are attractively valued

The MSCI Europe ex UK Small Cap Index is trading on an 11x forward P/E multiple, which according to the data in Exhibit 6 has proved to be a favourable entry point for future returns. Since 2007, data from JHI show that European small-cap stocks have traded at an average 16% premium to large-cap stocks, due to their higher growth potential, and only moved to a discount in H123; in mid-September 2023 the discount was 5%.

Exhibit 6: MSCI Europe ex UK Small Cap Index returns following 11x forward P/E (%)

Date index hit 11x P/E |

Subsequent three-year return |

Subsequent five-year return |

4 July 2008 |

10.6 |

28.4 |

26 September 2008 |

8.1 |

78.4 |

5 August 2011 |

69.0 |

108.2 |

18 May 2012 |

109.3 |

135.8 |

Average |

49.3 |

87.7 |

Beckett opines that the price paid for a share really matters and says that the period of free money since the global financial crisis is over. While the manager expects inflation and interest rates to come down, he suggests that interest rates will not be zero and could settle in the 3–4% range, so company valuations will be more important in the next 10 years than they were in the last decade.

The catalyst for a European small-cap rally

While investors have been concerned about a recession, which has negatively affected the performance of European small-cap stocks, the manager suggests that if there is no hard recession, these stocks should outperform. He adds that European small-cap stocks tend to outperform once purchasing manager indices have troughed, which looks likely. Beckett suggests that a European economic hard landing would imply mass unemployment, which he considers unlikely due to demographic trends and signs of real wage growth. As inflation moderates, the manager believes that economic confidence will increase, leading to higher demand for European small-cap stocks.