2022 – a year of two parts

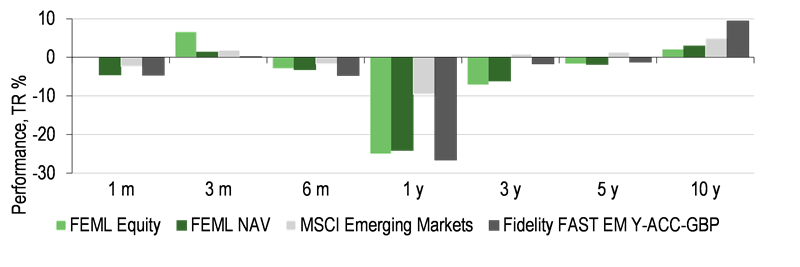

Last year was a challenging one for FEML. Formerly known as Genesis Emerging Markets, the investment company was transferred to Fidelity in October 2021, less than six months before Russia invaded Ukraine. The invasion had significant implications for the emerging market universe, and Chris Tennant, co-manager of the portfolio, highlighted that 2022 was a ‘year of two parts’ for FEML. The first half was dominated by the ‘black swan’ event of the Russian invasion, as well as negative news flow from China arising from strict lockdowns and heightened regulatory scrutiny. By contrast, an abrupt improvement in sentiment was evident from the autumn after the Federal Reserve indicated it would ease its pace of interest rate hikes and China started to reopen the economy and bring its zero-COVID policy to an end. This resulted in emerging market equities outperforming their developed market counterparts over the final quarter of the year.

FEML’s overall weakness in 2022 can be attributed to its underperformance relative to the index in Q1, which was outsized and unprecedented. In normal times FEML should do well in down markets, given its quality emphasis, but the Russian invasion of Ukraine and subsequent cessation of trading of Russian equities meant that all Russian equities were marked to zero. As a result, the portfolio’s overweight exposure to Russia at the start of the war caused performance for the calendar year to be dominated by the impact of the war in Ukraine. It is worth pointing out that FEML’s ability to hedge was beneficial and allowed Price and Tennant to offset some of the losses, with the portfolio making use of a Russian index short to reduce country risk. Following the invasion, Price and Tennant focused on adding breadth to the portfolio, which is illustrated by an increase in the portfolio’s holdings count.

Cognisant of the importance of value in this environment, Price and Tennant also started to look for attributes such as shorter duration and high dividends on a highly selective basis, including in areas such as banking and energy. The portfolio managers stress that the search for value does not compromise on quality attributes, and they continue to focus on high ROE businesses with strong balance sheets.

The end of the year was dominated by the reopening of China’s economy and the easing of regulatory headwinds in the country. Price and Tennant are cautiously optimistic on China and increased their positioning to an overweight relative to the benchmark towards the end of the year, to reflect their view that after a particularly challenging 2022, a sustained change in sentiment has scope to influence returns significantly. They point out that Chinese companies are trading on very low multiples and, as a result of the COVID lockdowns, households in the country have meaningful excess savings, which gives them the ability and capacity to spend. Price and Tennant anticipate a cyclical recovery, with changes in regulation, as well as the improving backdrop for the Chinese consumer, also likely to prove supportive. Towards the end of the period, the portfolio managers initiated an index future on the Hang Seng Index to rapidly gain exposure to the rallying Chinese market.

Using Fidelity’s local presence to unearth hidden gems

The managers point out that one of the key benefits of the closed ended structure is the ability to invest in companies further down the market cap spectrum. Price and Tennant initiated positions in a number of mid-cap stocks over the year. These include Brazilian IT services company Cielo, which produces hardware systems for processing card payments, and TBC Bank, the largest banking group in Georgia. These positions bolster the portfolio’s mid-cap exposure, which already includes names like Eicher Motors, an Indian motorbike company positively exposed to the growing trend of paying a premium for quality products and brands in India through its Royal Enfield brand. We think these positions indicate how FEML is successfully utilising Fidelity’s research resources and local presence to identify smaller-cap names that have been underappreciated by the market.

This team’s ability to uncover local gems has been made harder in recent years given that pandemic restrictions limited the team’s ability to travel in 2020 and 2021. Price and Tennant point out that the easing of these measures in 2022 allowed the emerging markets team at Fidelity to resume company visits, something that has greatly enhanced their ability to establish conviction in the investment theses of companies. Over the course of 2022, the investment team visited a number of countries, including Brazil, South Africa, Saudi Arabia, Indonesia and India. The managers point to the South Africa trip as being particularly productive in helping them carry out due diligence on several companies of interest. This included ABSA Bank, a retail-focused large South African bank. Having completed due diligence locally, the team formed a stronger conviction that the business presented an attractive investment opportunity and initiated a position in the company.

Over the past few years, the emerging market asset class has de-rated significantly, particularly compared to developed markets. While the managers are aware that earnings downgrades in certain industries could still come, and that some companies will be particularly vulnerable to higher costs and a recession, the team believes that much of this potentially negative impact on businesses is already reflected in the price. As such, they are cautiously optimistic about 2023. Price and Tennant acknowledge that the portfolio has faced a series of headwinds over the past six months but point out that they have remained focused on what they do best and have been active in repositioning the portfolio as the period has unfolded. The managers believe that the market will gradually accept that the age of free money is over, and while this volatility persists, they will continue to cast the net wide and look for opportunities in areas of the market that offer quality at an attractive price.

Current portfolio positioning

At 31 December 2022, the portfolio’s included 97 long and 70 short positions. As described in our initiation report, Fidelity’s team can build a higher gross long exposure as part of its long/short strategy, with net exposure targeted at a neutral c 100–110%.

FEML’s geographical split is shown in Exhibit 1. Fidelity’s high-conviction approach results in significant concentration in the top three countries at c 64%: China (c 20% and c 34% if we include Hong Kong), India (c 19%) and South Africa (c 11%). While Hong Kong, Kazakhstan, India and South Africa are overweight, Taiwan is underweight the MSCI EM Index.

Exhibit 1: Portfolio breakdown by geography at 31 December 2022

Country |

Portfolio weight |

Benchmark* |

Active weight vs benchmark* |

China |

20.4 |

32.3 |

(12.0) |

India |

19.2 |

14.4 |

4.8 |

Hong Kong |

13.2 |

0.0 |

13.2 |

South Africa |

11.2 |

3.7 |

7.5 |

Taiwan |

8.9 |

13.8 |

(5.0) |

Brazil |

6.8 |

5.5 |

1.3 |

Kazakhstan |

5.1 |

0.0 |

5.1 |

Peru |

4.8 |

0.3 |

4.5 |

Canada |

4.2 |

0.0 |

4.2 |

France |

3.6 |

0.0 |

3.6 |

Other countries |

16.1 |

16.6 |

(0.5) |

Total country exposure** |

113.3 |

100.0 |

|

Other index / unclassified |

(15.4) |

0.0 |

|

Total equity exposure |

97.9 |

100.0 |

|

Source: Fidelity International, Edison Investment Research. Note: *MSCI EM Index. At 31 December 2022. **From the factsheet. The portfolio’s long-short structure means that net equity exposure does not always sum to 100%.

Exhibit 2 illustrates FEML’s portfolio by sector. The cyclical information technology, financials, materials and industrials sectors combined represent 73.1% of the portfolio, although this is largely a function of bottom-up stock picking and is indicative of where the portfolio managers find the most attractive opportunities to buy quality stocks trading at a reasonable price. Communication services is the largest sector underweight position relative to the benchmark at 9.3pp (at 31 December 2022). The exposure to commodity-related areas of the market is one area of conviction, given the view that rising demand for renewable energy and a scarcity of supply should boost demand over time.

Exhibit 2: Portfolio breakdown by sector at 31 December 2022

Industry |

Portfolio weight |

Benchmark* |

Active weight vs benchmark* |

Financials |

33.1 |

22.1 |

11.0 |

Information technology |

21.0 |

18.6 |

2.4 |

Consumer discretionary |

17.7 |

14.1 |

3.6 |

Materials |

10.5 |

8.9 |

1.6 |

Consumer staples |

10.2 |

6.4 |

3.8 |

Energy |

8.7 |

4.9 |

3.8 |

Industrials |

8.5 |

6.1 |

2.4 |

Communication services |

0.6 |

9.9 |

(9.3) |

Healthcare |

(0.1) |

4.1 |

(4.2) |

Real estate |

(1.3) |

1.9 |

(3.2) |

Utilities |

(1.6) |

3.0 |

(4.6) |

Total sector exposure** |

107.2 |

100.0 |

|

Other index / unclassified |

(9.3) |

0.0 |

|

Total equity exposure |

97.9 |

100.0 |

|

Source: Fidelity International, Edison Investment Research. Note: *MSCI EM Index. At 31 December 2022. **From the factsheet. The portfolio’s long-short structure means that net equity exposure does not always sum to 100%.

Exhibit 3 lists FEML’s top 10 overweight positions versus the benchmark (at 31 December 2022). As the table illustrates, the active weight of the top 10 overweight stocks versus the benchmark is 38%.

Exhibit 3: Top 10 overweight positions (at 31 December 2022)

Company |

Country |

Sector |

Fund (%) |

Index* (%) |

Difference (%) |

TSMC |

Taiwan |

Information technology |

8.2 |

5.7 |

2.5 |

HDFC Bank |

India |

Financials |

7.6 |

0.0 |

7.6 |

Kaspi |

Kazakhstan |

Financials |

5.1 |

0.0 |

5.1 |

AIA Group |

Hong Kong |

Financials |

4.7 |

0.0 |

4.7 |

Naspers |

South Africa |

Consumer discretionary |

4.5 |

0.6 |

3.9 |

Alibaba |

China |

Consumer discretionary |

4.5 |

2.6 |

1.9 |

China Mengniu Dairy |

China |

Consumer staples |

3.7 |

0.2 |

3.5 |

TotalEnergies |

France |

Energy |

3.6 |

0.0 |

3.6 |

Infosys |

India |

Information technology |

3.6 |

1.0 |

2.6 |

ICICI Bank |

India |

Financials |

3.5 |

0.9 |

2.6 |

Top 10 (% of portfolio) |

|

|

49.0 |

11.0 |

38.0 |

Source: Fidelity International, Edison Investment Research. Note: *MSCI EM Index.

Key portfolio additions and new buys over the last 12 months

The managers added positions in energy companies over 2022, including French oil major TotalEnergies. The fourth largest global oil major, the company has a low-cost upstream portfolio with volumes tilted to conventional on and offshore oil in the likes of West Africa and the Middle East. The team expects the company to achieve strong returns, supported by attractive dividends and share buybacks.

The managers adjusted their exposure to China over the year in response to the rapidly changing policy landscape. They actively reduced their China exposure during Q3 to reflect the uncertainty facing the country, given prolonged lockdowns and the regulatory headwinds facing the property and tech sectors. As visibility started to improve following the National Congress of the Chinese Communist Party in October, and it appeared that Beijing was starting to ease restrictions they started to add to China, and continued to do so after it became clear that the country was abandoning its zero-COVID policy. Price and Tennant made additions across a series of names including internet stocks, re-opening plays and small allocations to real estate-related businesses. They also utilised a futures position on the Hang Seng Index to scale up exposure at pace.

The team’s indirect China exposure includes a position in Naspers, a global consumer internet industry operator listed in South Africa, that acts as a proxy for its holding in Chinese internet media and services company, Tencent. In terms of direct exposure, the managers also own Alibaba, a position they added to towards the end of 2022 in light of its attractive valuations (its EV/sales multiple hit the lowest level on record last autumn) and the company’s continued commitment to share buybacks. FEML’s exposure to the Chinese internet sector is limited but increasing and represents an area of the market where the team is increasingly finding opportunities as regulatory headwinds ease and the Chinese economy reopens. The managers started adding to their position in Trip.com during Q422, as part of the team’s strategy to increase its exposure to China as the economy reopens and the zero COVID policy comes to an end.

Looking to India, the team also initiated a position in ICICI Bank over the year, which is the second largest private sector bank in India. The bank has seen the quality of its assets improve in the last few years, such that it now rivals high-quality peers such as HDFC Bank, as it has built a strong balance sheet and delivered strong returns. The managers believe that the bank has access to good levers for growth and has strong margins. Its valuation is also attractive, particularly for a bank that they expect can deliver strong levels of growth and returns on equity.

Other new positions included Credicorp, the dominant financial services franchise in Peru, Southern Copper, a mining company in Peru and Mexico, and South African leading domestic food retailer Shoprite, which is outpacing rivals with its digital offering and improving its high-end offering, according to the managers.

Top portfolio sells and reductions over the last 12 months

Among the key exits during the last 12 months was Zhejiang Sanhua, a Chinese thermal control components maker. Overall, the managers say this has been a good position for the portfolio, but as the valuation increased, the team decided to exit the position. The portfolio managers also saw rising competitive intensity and some risk that a competitor would take some of Sanhua’s market share.

The position in copper miner First Quantum Minerals remains a core holding in the portfolio, but was trimmed given the weaker macroeconomic environment. The team’s conviction in copper remains high, despite the fact that recessionary concerns, rising interest rates and issues in the Chinese property sector have weighed on metals over the year.

The team also trimmed its holding in MTN Group, the second largest mobile operator in South Africa and one of the largest across the continent. Over the past few years, the company has benefited from a reduction in competitive intensity in its core South African and Nigerian telecoms markets, with revenues growing following a long period of no growth. During 2022, the team started to reduce the position, in part to take profits but also due to concerns about the weakening macroeconomic environment in Ghana and Nigeria.

Positions in two semiconductor giants, Samsung Electronics and TSMC, were also trimmed to reflect the fact that the tech hardware sector has been impacted by worries about consumer discretionary spending. As a result, the managers actively adapted position sizes through the course of the year. Despite this, valuations look attractive, and Samsung Electronics and TSMC are both leading players in the semiconductor and memory industries, with strong competitive advantages.

Examples of engagement with portfolio companies

Fidelity has been a signatory of the United Nations Principles for Responsible Investment since 2012 and submits an annual report detailing how it incorporates environmental, social and governance (ESG) into its investment analysis. Fidelity has its own proprietary ESG ratings framework, where its fundamental research analysts carry out an assessment both of how a company performs on various ESG metrics, and its direction of travel on sustainability issues. The ESG integration process at Fidelity involves active engagement with investee companies, with the benefits of Fidelity’s local presence playing an important role here. We present three examples of engagements with the portfolio’s holdings below.

First Quantum Minerals is a Canada-listed copper miner with core assets in Zambia and Panama. The managers are positive about the long-term prospects of copper given supply constraints for the metal, which benefits from the move towards greener energy and electric vehicles. Fidelity had multiple ESG-focused meetings over the course of the last year with First Quantum Minerals. The topics discussed included the company’s policies on biodiversity, waste management, water usage, carbon emissions (including coal exposure) and community management. One area of concern was the company’s Sese coal-fired power project in Botswana. In August 2022, First Quantum Minerals confirmed that this project will be closed: four units are already closed and the last one will be closed by end 2023. More broadly, the company provided details of its energy transition plan, which is for a 30% reduction in emissions by 2025 on an absolute basis, a 50% reduction by 2030 on an absolute basis and a 50% reduction in the carbon intensity of its copper mining operations. During these meetings, Fidelity noted that there is strong involvement from First Quantum’s board and CEO on ESG issues, which increased the investment team’s conviction in the stock.

BOC Aviation is an aircraft lessor that is 70% owned by Bank of China. Fidelity started engaging with the company in 2021. Around that time, BOC Aviation witnessed a downgrade in one of its third-party ESG ratings due to a lack of independent management oversight, transactions due to state controls and the risk of a skills shortage. The company had published its first ESG report for 2020 and had plans to disclose its materiality framework with some of the top issues in its 2021 report. The report did not include climate change statements/risk assessment and the company had no plans to do this. Fidelity recommended that BOC Aviation improve its disclosure and reporting related to various ESG metrics including the disclosure of a dedicated ESG team for external engagements and alignment with certificates, remuneration linkage to ESG key performance indicators, and more public disclosure on targets and tangible progress via investor calls, press releases, process refinement for minority shareholder protection and one-to-one meetings.

More recently, Fidelity also engaged with BOC’s management team to encourage it to keep improving disclosure, analyse risks relating to geopolitical uncertainty, take more proactive steps to control Scope 3 emissions and review diversity parameters, especially at board level. The management team is aiming to increase disclosure levels even more and intends to comply gradually with international ESG standards. More broadly, the management team was very responsive to Fidelity’s suggestions and will continue to engage/work on the issues in question.

Fidelity believes there has been a notable improvement in the company’s disclosures following the meetings and one of BOC Aviation’s third-party ESG ratings was upgraded in December 2022 due to improved governance.

OMV is an Austria-listed integrated oil company focused on the chemicals, upstream and refining and marketing segments. Fidelity’s engagement interactions commenced with OMV in October 2020 on a broad-based range of ESG topics. During the December 2022 meeting, Fidelity spoke to OMV about two employees who had been injured that year by the explosion of a crude distillation unit. The team also spoke about the target to reduce emissions by 30% by 2030 and to reach net zero by 2050, and expressed concerns about the current management’s accountability in reaching the targets. Fidelity discussed OMV’s reluctance to return excess cash in a subsidiary to shareholders, which negates the interests of minority shareholders. The chairman explained that health and safety is part of OMV’s remuneration framework, which Fidelity viewed as satisfactory in showing that the correct incentives are in place to minimise the risk of this type of safety incident reoccurring. On greenhouse gas emissions targets, the chairman said that OMV was allocating capex to low-carbon businesses that met internal rate of return thresholds and had clear competitive advantages. Fidelity’s team was satisfied with this response but decided that emissions reduction via disposal was an area to monitor going forward. However, Fidelity’s team was dissatisfied by the chairman’s response that the dividend policy had improved and will aim to have further discussions with the CEO or chairman or take a collective approach with other minority shareholders.

Fund profile: Capital growth and smart risk management

On 1 July 2021, FEML’s board announced the appointment of Fidelity as its manager. The previous manager was Genesis Investment Management (Genesis), which launched the company in July 1989.

FEML aims to achieve long-term capital growth from an actively managed portfolio primarily made up of securities and financial instruments providing exposure to EM companies, both listed and unlisted. Lead portfolio manager, Nick Price, supported by co-portfolio manager, Chris Tennant, employs an actively managed global growth equity strategy with additional investment tools, enhancing the long-only approach. These include a series of complementary strategies, relaxing the typical constraints of traditional long-only strategies to generate enhanced risk-adjusted returns. At least 80% of the company’s total assets (measured at the time of investment) are exposed to EM companies. The managers aim to maintain a diversified portfolio of a minimum of 75 holdings (comprising a mixture of long and short exposures) in companies listed in or operating across at least 15 countries. Gearing is permitted either through borrowing of up to 10% of NAV and/or by entering into derivative positions (both long and short), which have the effect of gearing, to enhance performance.

The appointment of Fidelity took effect on 4 October 2021, following shareholder approval at the extraordinary general meeting on 1 October.

Given extremely high commonality, the FAST Emerging Markets fund is used to illustrate FEML’s investment strategy. The following features differentiate FEML from FAST Emerging Markets:

■

FEML has more flexibility in its investment mandate, such as the ability to invest in unlisted stocks. It is likely to have slightly different portfolio weightings because of its liquidity profile. However, these are very marginal.

■

There are no retail share classes for FAST Emerging Markets and it is not marketed to retail investors in the UK or overseas. Fidelity looks to market FEML to both institutional and retail investors.

The company is managed by Nick Price and Chris Tennant, with the support of Fidelity’s wider EM portfolio management team and 59 (as at 31 December 2022) equity research analysts responsible for the coverage of emerging market stocks. Both managers tap into the expertise of the EM debt team at Fidelity.

Price designed FEML’s investment approach. Having launched FAST Emerging Markets, he has developed, managed and grown the strategy for more than a decade. He has 25 years’ investment experience and has been with Fidelity since 1998. Chris Tennant is an emerging market specialist with 10 years’ investment experience, all with Fidelity. Chris started his career as an analyst across various sectors before progressing to a portfolio management role in 2019.

The board consists of six independent non-executive directors and has been chaired by Heather Manners since 8 December 2022. Ms Manners was appointed as a director of the company on 5 May 2022. She is an award-winning market professional with some 34 years’ experience of investment in Asia, mostly recently, and for the past 15 years as the co-founder, CEO and CIO of Prusik Investment Management. Ms Manners took over the role of chairman from Hélène Ploix, who retired from the board following the conclusion of the 2022 AGM on 8 December 2022.

On 12 December 2022, the company announced the appointment of Julian Healy to the board as an independent non-executive director with immediate effect. Mr Healy will also serve on the company's audit and risk committee, and it is intended that he will succeed Russell Edey as chair of that committee when the latter retires from the board in the first half of 2023. Following Mr Edey’s retirement, the board will be reduced to five directors.

The other directors and dates of appointment are Katherine Tsang (July 2017), Simon Colson (July 2019) and Torsten Koster (July 2020).

Strong long-term track record of FEML’s strategy, based on FAST Emerging Markets

The strategy has outperformed the MSCI EM Index since launch in October 2011 (Exhibit 7). Exhibit 8 illustrates that the strategy’s higher gross exposure increases active money; Fidelity believes that the increased exposure provides the strategy with greater opportunity to outperform.

Exhibit 7: Long-term track record of Fidelity FAST EM Fund Y- ACC-GBP (FAST) in sterling terms

|

Exhibit 8: Potentially greater scope for outperformance of strategy with higher long exposure for FEML

|

in sterling terms")

|

|

Source: Refinitiv, Edison Investment Research as at 31 December 2022. Note: *Fidelity FAST EM Fund, launched in 2011. Green represents long exposure; grey represents short exposure. **Performance since FAST's launch on 31 October 2011.

|

Exhibit 7: Long-term track record of Fidelity FAST EM Fund Y- ACC-GBP (FAST) in sterling terms

|

|

Exhibit 8: Potentially greater scope for outperformance of strategy with higher long exposure for FEML

|

|

Source: Refinitiv, Edison Investment Research as at 31 December 2022. Note: *Fidelity FAST EM Fund, launched in 2011. Green represents long exposure; grey represents short exposure. **Performance since FAST's launch on 31 October 2011.

|

General disclaimer and copyright This report has been commissioned by Fidelity Emerging Markets and prepared and issued by Edison, in consideration of a fee payable by Fidelity Emerging Markets. Edison Investment Research standard fees are £60,000 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2023 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument. New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

General disclaimer and copyright This report has been commissioned by Fidelity Emerging Markets and prepared and issued by Edison, in consideration of a fee payable by Fidelity Emerging Markets. Edison Investment Research standard fees are £60,000 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2023 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument. New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

over three years (%)")