CEO Andrew Bell, investment director James Hart

The investment director’s view: Fundamentally positive

WTAN’s core portfolio of five global managers and one UK manager represents around 75% of assets under management (AUM). This part of the portfolio provides shareholders with access to a select, but diversified group of managers, which invest in high-quality, predominantly large and mid-sized global companies. The managers focus on companies with enduring cash flows and underappreciated growth prospects. Investments may also include undervalued, often cyclical businesses. In addition, WTAN’s specialist portfolio, which represents the remaining 25% of its AUM, is intended to capture the many attractive investment opportunities that fall outside the remit of most mainstream fund managers due to their size, unlisted or specialist nature, but offer the prospect of superior returns over the long run. This part of WTAN’s portfolio includes best-in-class managers investing in emerging markets, private equity, real estate, life sciences and climate change strategies (Exhibit 1).

James Hart, WTAN’s investment director, believes that the trust’s diversified, core plus offering makes it a ‘cornerstone investment’ for many of its shareholders, providing a ‘one-stop shop for global equities’. This covers a significant percentage of the global large and mid-cap market, along with a wide variety of interesting opportunities in more niche areas, via a single investment.

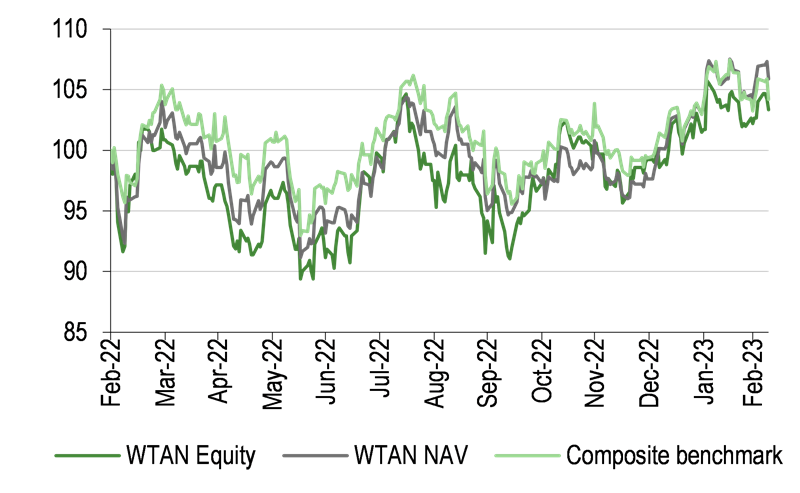

The first nine months of 2022 was particularly challenging for all investors. Markets were blind-sided by Russia’s invasion of Ukraine and the adverse knock-on effects this had for energy and commodity prices, which put further upward pressure on already elevated inflation. The unexpectedly aggressive response from central banks then added to market uncertainty and volatility. Market conditions improved somewhat, however, in the final quarter of 2022 and the early months of 2023.

Hart believes the worst of this turmoil is now behind us, and he is fundamentally positive on the outlook for global equity markets. One key reason for his optimism is that he believes inflation has most likely peaked, and although it may be slow to fall, a stabilisation of inflationary pressures will allow central banks to cease aggressive monetary tightening and hold interest rates steady while they assess the medium-term inflation outlook. This will come as a great relief to investors. China’s re-opening after almost three years of stringent, economically crippling lockdowns is another reason why Hart is positive about the market outlook. As is the case with the prospect of stable to lower interest rates, a resurgent China removes a number of the uncertainties and risks that drove last year’s market volatility, and has thus been warmly welcomed by financial markets.

The investment director is sceptical about the likelihood of a deep recession in the United States and the UK, but if recession does materialise, he expects it to be mild and shallow, and followed by a period of ‘moderate but sustained growth’. He also views company fundamentals as ‘generally good’, corporate debt levels are low and valuations are not excessive across much of the market, all of which bodes well for an extension of the nascent market upturn.

Hart is careful to guard against complacency however, as there are always risks: both the so-called ‘known unknowns’ such as an unexpected deterioration in the UK economy or policy mistakes such as last year’s misguided UK fiscal package, and the ‘unknown unknowns’, unanticipated shocks such as the pandemic or the recent collapse of Silicon Valley Bank in the US. Any of these could trigger a change in view, as well as the need to reposition the portfolio and adjust gearing. So, WTAN will be remaining vigilant for any hint that events are deviating from their anticipated path.

Unexpected and unwelcome market developments are not the only risks on which Hart and his colleagues are focused. Companies are also exposed to potentially adverse developments related to ESG issues. WTAN already integrates the assessment of environmental, social and governance risks into its investment process (see our September 2022 note for further detail). However, in the past year, WTAN has made major progress in its efforts to better identify, monitor and, where possible, mitigate ESG risks. To this end, in early 2022, a Responsible Investment strategy was adopted to ensure that WTAN’s portfolio will consist entirely of sustainable businesses by 2030.

WTAN defines the characteristics of a sustainable company as:

■

Prosperity: possessing sustainable cash flows, exhibiting good corporate behaviour, strong stakeholder engagement and respect for its shareholders.

■

People: having a strong and experienced management team (and board) with an inclusive and diverse culture that respects the wellbeing of its customers and others in the organisation, its value chain and its community.

■

Planet: following a clear strategy to minimise its environmental impact and, wherever possible, transition towards net zero by 2050. Additionally, it should be positioned to help accelerate the energy transition and carbon reduction.

■

Partnership: collaborating and engaging with all stakeholders and participating in industry initiatives to promote good practices.

Hart has led the trust’s efforts to ensure its 2030 sustainability target is successfully implemented. The first step in this process has been to establish a proprietary, in-house framework and baseline ESG ratings for each of the companies held by WTAN’s managers, in order to assess their current position relative to WTAN’s sustainability objective. Using a methodology devised by WTAN, each manager was asked to rate each portfolio holding across the four pillars outlined above – prosperity, people, planet and partnership – which together characterise a ‘sustainable business’. This data was converted by WTAN to a numerical score, with each holding receiving a rating between 1 and 100. A total of nearly 300 companies across the core and specialist portfolios were assessed, with the weighted average assessment of sustainability being 80 out of a possible 100. This means that, on average, the companies held by WTAN’s managers are already 80% aligned with sustainable practices.

While there is still work to be done to realise WTAN’s 2030 target, most companies are on a ‘positive sustainable trajectory’, and Hart is pleased with the work done to date to establish WTAN’s Responsible Investment strategy, which he believes will help the trust ‘set the agenda for the years ahead’. WTAN conducts annual ESG review meetings with all its managers, and their progress on these matters will be monitored and discussed, with particular focus on situations where progress stalls or persistently falls short on multiple issues.

and sector (right) as at 28 February 2023")

and sector (right) as at 28 February 2023")