While overall gold production fell 10.0% cf H116, there were sharp increases at both the BTRP (+14.0%) and the ETRP (+77.3%), while production at both of Pan African’s traditional, underground operations fell, with output at Barberton down 21.0% and at Evander down 27.2%. As a result, the BTRP and ETRP were Pan African’s second and third most profitable business units overall, behind Barberton (underground), but ahead of Evander (underground). As a result, for the first time the company recorded greater profits, in the form of adjusted EBITDA, from its tailings retreatment projects than from its underground operations.

We had anyway expected a decline in tonnes milled from underground at Evander to 349kt for FY17 (174.5kt pro rata for H117) versus c 400ktpa in prior years. In the event, this decline was slightly greater than expected, being augmented by Section 54 DMR stoppage notices, in particular.

Exhibit 2: EGM operational results, H114-H217e, actual and forecasts

|

H114 |

H214 |

H115 |

H215 |

H116 |

H216 |

H117 |

H117 vs H216 (%) |

H217e |

Tonnes milled underground (t) |

200,272 |

194,855 |

197,879 |

184,107 |

200,942 |

207,339 |

161,872 |

(21.9) |

116,333 |

Head grade underground (g/t) |

6.20 |

4.17 |

4.30 |

4.92 |

5.80 |

5.60 |

5.40 |

(3.6) |

6.01 |

Underground gold contained (oz) |

39,921 |

26,138 |

27,357 |

29,137 |

37,471 |

37,351 |

28,103 |

(24.8) |

22,467 |

Tonnes milled surface (t) |

111,225 |

149,676 |

198,578 |

67,645 |

0 |

0 |

0 |

N/A |

0 |

Head grade surface (g/t) |

1.30 |

1.47 |

1.40 |

0.22 |

0.00 |

0.00 |

0.00 |

N/A |

0.00 |

Surface gold contained (oz) |

4,649 |

7,095 |

8,938 |

477 |

0 |

0 |

0 |

N/A |

0 |

Tonnes milled (t) |

311,497 |

344,531 |

396,457 |

251,752 |

200,942 |

207,339 |

161,872 |

(21.9) |

116,333 |

Head grade (g/t) |

4.45 |

3.00 |

2.85 |

3.66 |

5.80 |

5.60 |

5.40 |

(3.6) |

6.01 |

Contained gold (oz) |

44,570 |

33,233 |

36,295 |

29,614 |

37,471 |

37,351 |

28,103 |

(24.8) |

22,467 |

Recovery (%) |

97 |

102 |

93 |

100 |

97 |

99 |

94 |

(5.4) |

100 |

Production underground (oz) |

38,710 |

27,246 |

26,024 |

27,722 |

36,370 |

37,126 |

26,477 |

(28.7) |

22,467 |

Production surface (oz) |

3,955 |

6,645 |

7,831 |

1,982 |

0 |

0 |

0 |

N/A |

|

Total production (oz) |

42,665 |

33,891 |

33,855 |

29,704 |

36,370 |

37,126 |

26,477 |

(28.7) |

22,467 |

Recovered grade (g/t) |

4.26 |

3.06 |

2.66 |

3.67 |

5.63 |

5.57 |

5.09 |

(8.7) |

6.01 |

|

|

|

|

|

|

|

|

|

|

Gold sold (oz) |

43,164 |

33,392 |

33,733 |

29,825 |

36,370 |

37,126 |

26,477 |

(28.7) |

22,467 |

Average spot price (US$/oz) |

1,302 |

1,290 |

1,233 |

1,206 |

1,105 |

1,221 |

1,256 |

2.8 |

1235 |

Average spot price (ZAR/kg) |

421,273 |

443,171 |

435,376 |

461,891 |

483,309 |

605,265 |

565,009 |

(6.7) |

517,627 |

|

|

|

|

|

|

|

|

|

|

Total cash cost (US$/oz) |

985 |

1,358 |

1,317 |

1,277 |

995 |

918 |

1,457 |

58.8 |

1,739 |

Total cash cost (ZAR/kg) |

318,616 |

466,650 |

464,955 |

489,118 |

435,190 |

454,756 |

655,304 |

44.1 |

728,835 |

Total cash cost (US$/t) |

134.93 |

134.43 |

112.03 |

149.51 |

180.15 |

163.58 |

238.34 |

45.7 |

335.83 |

Total cash cost (ZAR/t) |

1,373.00 |

1,427.75 |

1,230.00 |

1,794.96 |

2,450.00 |

2,532.68 |

3,334.00 |

31.6 |

4,378.00 |

|

|

|

|

|

|

|

|

|

|

Implied revenue (US$000s) |

56,200 |

42,940 |

41,593 |

35,694 |

40,189 |

44,773 |

33,255 |

(25.7) |

27,747 |

Revenue (ZAR000s) |

565,576 |

460,221 |

456,799 |

427,794 |

546,731 |

685,865 |

465,296 |

(32.2) |

361,716 |

Implied revenue (£000s) |

35,471 |

25,504 |

25,566 |

23,502 |

26,219 |

31,052 |

26,025 |

(16.2) |

22,237 |

|

|

|

|

|

|

|

|

|

|

Implied cash costs (US$000s) |

42,029 |

46,317 |

44,415 |

37,639 |

36,199 |

33,916 |

38,581 |

13.8 |

39,068 |

Cash costs (ZAR000s) |

422,810 |

491,905 |

487,800 |

451,884 |

492,308 |

525,124 |

539,681 |

2.8 |

509,307 |

Implied cash costs (£000s) |

26,527 |

27,662 |

27,297 |

24,917 |

23,635 |

23,754 |

30,188 |

27.1 |

31,325 |

|

|

|

|

|

|

|

|

|

|

Forex (ZAR/£) |

15.9388 |

17.8279 |

17.8700 |

18.1318 |

20.8300 |

22.0942 |

17.8771 |

(19.1) |

16.2588 |

Forex (ZAR/US$) |

10.0600 |

10.6853 |

10.9827 |

11.9173 |

13.6000 |

15.4132 |

13.9875 |

(9.2) |

13.0363 |

Forex (US$/£) |

1.5844 |

1.6685 |

1.6269 |

1.5186 |

1.5328 |

1.4335 |

1.2778 |

(10.9) |

1.2478 |

Source: Edison Investment Research, Pan African Resources

During the six month period under review, Evander was issued with four Section 54 regulatory notices by the DMR, which resulted in 13 lost production days, compared with three notices and two days in the prior year period.

While cash costs of production increased by 58.8% in US dollar terms, to US$1,457/oz, most of the increase could be attributed to the lower number of ounces produced and the adverse moves in the rand:dollar exchange rate. In rand terms, aggregate costs increased by a much more respectable 2.8%, indicating a continued focus on cost control, notwithstanding the production challenges experienced during the half year.

Operations at Evander have now advanced from 25 to 26 level, which has simultaneously improved access to more high-grade panels as well as allowing management to manage and blend the ore mined towards achieving its target of 110,000oz of gold per annum. All other things being equal therefore, the head grade is expected to remain in the range 6-7g/t for the next three to five years. Note that, had an underground head grade of 7.2g/t prevailed in H117 (and applying the group’s H117 marginal tax rate to the incremental profits), we estimate that it would have added c 0.41p to both Pan African’s EPS and headline EPS in H117. Operations will remain focused at 25 level for eight years, before progressing to 26 level. Excluding Elikhulu, management’s target is to achieve a consistent all-in sustaining cost of production of US$1,100/oz at Evander (vs US$1,310/oz in the period under review).

In fact, immediately prior to the February announcement of a fatality at seven shaft, Evander was reported to be mining material at a diluted grade of 8g/t from underground and at a mine call factor in excess of 80% (vs 65% in H116, 59% in H115 and a target of 73%) as a result of a focus on blasting and cleaning practices, in particular, including the use of blasting barricades. In the wake of the fatality, there will now be a 55-day underground mining hiatus at Evander, while steelwork at the 7A, 7 and 8 shafts is refurbished. During this period, the pump column at 8 shaft will be the only one at the mine that is operational, which represents a technical engineering risk in the event of a similar failure as at 7 shaft. During this period, management is also planning to drill a second exploration drill hole into the Kinross 2010 pay channel as a precursor to potential future exploitation.

On 10 March, PAF announced that repairs at 7 shaft were “progressing on schedule” and that they were “still expected to be completed within the 55 day period previously communicated” (ie around the middle of April). At the same time, in order to ameliorate Evander’s underground fixed cost base once mining recommences, management also announced a retrenchment programme (with the agreement of the National Union of Mineworkers and the appropriate South African government agency) whereby approximately 30% of Evander Mines’ employees will be retrenched at an estimated cost of ZAR54m (US$4.2m or £3.4m). In order to minimise the number of job losses overall, Evander has agreed to re-engage a number of retrenched employees once site activities commence at Elikhulu. In the meantime, Edison estimates that this initiative will save Evander approximately 15% of its cost base in the longer term. Pro-rata, this implies a net additional cost in the order of ZAR25m in H217. However, this should be substantially offset by management’s initiative to utilise available plant capacity to continue processing tailings and additional surface sources.

Barberton Gold Mining Operations (BGMO)

As at Evander, Barberton was served with six Section 54 regulatory notices in H117, which resulted in eight days of lost production (cf one notice costing three days of production in H116). In aggregate therefore, Barberton and Evander were served with a combined ten Section 54 regulatory stoppage notices during the 184 day period, which resulted in 21 days of lost production (cf four notices and five days lost in the prior year period). In addition however, Barberton also experienced a degree of community unrest, which was designed to target government service delivery, but which also had the collateral effect of costing Barberton six days of lost production, as a result of protests preventing employees from reporting to work. Finally, Barberton experienced flexibility constraints at its Fairview mine and specifically at its high grade 11-block, which resulted in lower grades being mined. As with Evander however, while cash costs of production were reported to have increased by 42.0% compared with the prior year period, to US$967/oz (vs US$681/oz), in fact aggregate cash costs increased by only a much more modest 3.9% in local currency terms compared to H216:

Exhibit 3: Barberton operational results, H114-H217e

|

H114 |

H214 |

H115 |

H215 |

H116 |

H216 |

H117 |

H117 vs H216 (%) |

H217e |

Tonnes milled (t) |

149,589 |

142,532 |

126,713 |

134,036 |

139,430 |

128,953 |

123,168 |

(4.5) |

139,137 |

Head grade (g/t) |

10.45 |

10.56 |

11.40 |

10.00 |

10.60 |

10.77 |

9.40 |

(12.7) |

10.26 |

Contained gold (oz) |

50,272 |

48,374 |

46,443 |

43,080 |

47,117 |

44,656 |

37,224 |

(16.6) |

45,895 |

Recovery (%) |

91 |

96 |

89 |

90 |

92 |

92 |

93 |

1.1 |

92.5 |

Production underground (oz) |

41,849 |

46,130 |

42,666 |

38,649 |

43,487 |

40,941 |

34,471 |

(15.8) |

42,449 |

Production calcine dumps/surface ops (oz) |

390 |

369 |

76 |

102 |

130 |

132 |

0 |

(100.0) |

|

Total production (oz) |

42,239 |

46,499 |

42,742 |

38,751 |

43,617 |

41,073 |

34,471 |

(16.1) |

42,449 |

|

|

|

|

|

|

|

|

|

|

Gold sold (oz) |

45,405 |

43,333 |

41,232 |

40,261 |

43,617 |

41,073 |

34,471 |

(16.1) |

42,449 |

Average spot price (US$/oz) |

1,317 |

1,290 |

1,229 |

1,206 |

1,113 |

1,221 |

1,268 |

3.8 |

1,235 |

Average spot price (ZAR/kg) |

426,101 |

443,171 |

433,966 |

461,891 |

486,567 |

605,265 |

570,251 |

(5.8) |

517,627 |

|

|

|

|

|

|

|

|

|

|

Total cash cost (US$/oz) |

787 |

770 |

885 |

825 |

681 |

708 |

967 |

36.7 |

795 |

Total cash cost (ZAR/kg) |

254,506 |

263,029 |

312,502 |

318,061 |

297,877 |

351,358 |

434,999 |

23.8 |

333,296 |

Total cash cost (US$/t) |

222.22 |

251.14 |

287.82 |

238.62 |

213.09 |

225.38 |

270.74 |

20.1 |

242.61 |

Total cash cost (ZAR/t) |

2,403.00 |

2,668.95 |

3,161.00 |

2,860.08 |

2,898.00 |

3,525.32 |

3,787.00 |

7.4 |

3,162.69 |

|

|

|

|

|

|

|

|

|

|

Implied revenue (US$000s) |

59,798 |

56,360 |

50,674 |

48,095 |

48,546 |

50,288 |

43,709 |

(13.1) |

52,424 |

Revenue (ZAR000s) |

601,758 |

600,142 |

556,300 |

574,798 |

660,091 |

774,505 |

611,400 |

(21.1) |

683,417 |

Implied revenue (£000s) |

37,743 |

33,700 |

31,148 |

31,559 |

31,671 |

34,950 |

34,207 |

(2.1) |

42,013 |

|

|

|

|

|

|

|

|

|

|

Implied cash costs (US$000s) |

33,242 |

35,796 |

36,471 |

31,983 |

29,711 |

29,064 |

33,347 |

14.7 |

33,755 |

Cash costs (ZAR000s) |

334,362 |

380,411 |

400,600 |

383,353 |

404,068 |

448,861 |

466,437 |

3.9 |

440,047 |

Implied cash costs (£000s) |

20,978 |

21,484 |

22,417 |

21,043 |

19,398 |

20,221 |

26,091 |

29.0 |

27,065 |

|

|

|

|

|

|

|

|

|

|

Forex (ZAR/£) |

15.9388 |

17.8279 |

17.8700 |

18.1318 |

20.8300 |

22.0942 |

17.8771 |

(19.1) |

16.2588 |

Forex (ZAR/US$) |

10.0600 |

10.6853 |

10.9827 |

11.9173 |

13.6000 |

15.4132 |

13.9875 |

(9.2) |

13.0363 |

Forex (US$/£) |

1.5844 |

1.6687 |

1.6269 |

1.5186 |

1.5328 |

1.4335 |

1.2778 |

(10.9) |

1.2478 |

Source: Edison Investment Research, Pan African Resources

Barberton is commencing multi-year wage negotiations with its labour-force later this year (note that Barberton traditionally negotiates its agreements outside the auspices of the South African Chamber of Mines’ collective wage bargaining process). In the meantime however, exploration drilling has confirmed at least a 200m down-dip extension of the high-grade 11-block of the MRC orebody. Consequently, work is underway to develop additional production platforms to expose additional high grades panels in order to increase mining grades and flexibility, with the result that a much improved performance is expected from BGMO operations’ in the second half of PAF’s financial year.

Barberton Tailings Retreatment Project (BTRP)

In contrast to BGMO and Evander, PAF’s retreatment operations typically outperformed our expectations. In the case of the BTRP, although throughput declined, the head grade was maintained at a very high level, which resulted in materially higher metallurgical recoveries, while aggregate costs actually fell in local currency terms. Consequently, the BTRP produced 14,741oz of gold during the period, compared to a long-term, sustainable expectation of 10,000oz per semi-annual period (ie representing production outperformance of 47.4%):

Exhibit 4: BTRP operational results, H114-H217e

|

H114 |

H214 |

H115 |

H215 |

H116 |

H216 |

H117 |

H117 vs H216 (%) |

H217e |

Tonnes processed tailings (t) |

343,137 |

472,599 |

484,315 |

487,312 |

464,179 |

495,036 |

388,905 |

(21.4) |

600,000 |

Head grade tailings (g/t) |

1.70 |

1.58 |

1.50 |

1.30 |

1.30 |

2.08 |

2.20 |

6.0 |

1.66 |

Tailings gold contained (oz) |

18,755 |

23,208 |

23,357 |

20,377 |

19,401 |

33,027 |

27,508 |

(16.7) |

32,022 |

Recovery (%) |

60 |

49 |

51 |

65 |

64 |

47 |

55 |

17.3 |

56 |

Production tailings (oz) |

11,603 |

11,282 |

11,710 |

13,219 |

12,830 |

15,481 |

14,741 |

(4.8) |

17,868 |

Production other (oz) |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

N/A |

0 |

Total production (oz) |

11,603 |

11,282 |

11,710 |

12,573 |

12,830 |

15,761 |

14,741 |

(6.5) |

17,868 |

Recovered grade (g/t) |

1.05 |

0.74 |

0.75 |

0.80 |

0.86 |

0.99 |

1.18 |

19.1 |

0.93 |

|

|

|

|

|

|

|

|

|

|

Gold sold (oz) |

11,603 |

11,282 |

11,710 |

12,573 |

12,830 |

15,761 |

14,741 |

(6.5) |

17,868 |

Average spot price (US$/oz) |

1,317 |

1,290 |

1,229 |

1,206 |

1,113 |

1,221 |

1,268 |

3.8 |

1,235 |

Average spot price (ZAR/kg) |

426,101 |

443,171 |

433,799 |

461,891 |

486,566 |

605,265 |

570,349 |

(5.8) |

517,627 |

|

|

|

|

|

|

|

|

|

|

Total cash cost (US$/oz) |

454 |

528 |

459 |

497 |

367 |

275 |

319 |

16.0 |

288 |

Total cash cost (ZAR/kg) |

146,928 |

181,511 |

162,203 |

190,268 |

160,665 |

136,287 |

143,451 |

5.3 |

120,914 |

Total cash cost (US$/t) |

15.36 |

12.72 |

11.11 |

12.88 |

10.15 |

8.68 |

12.09 |

39.3 |

8.59 |

Total cash cost (ZAR/t) |

154.53 |

131.28 |

121.98 |

152.69 |

138.00 |

134.96 |

169.00 |

25.2 |

112.00 |

|

|

|

|

|

|

|

|

|

|

Implied revenue (US$000s) |

15,281 |

14,584 |

14,392 |

15,112 |

14,280 |

19,286 |

18,692 |

(3.1) |

22,068 |

Revenue (ZAR000s) |

153,776 |

155,425 |

157,998 |

179,905 |

194,166 |

293,032 |

261,501 |

(10.8) |

287,680 |

Implied revenue (£000s) |

9,645 |

8,723 |

8,846 |

9,885 |

9,316 |

13,310 |

14,628 |

9.9 |

17,685 |

|

|

|

|

|

|

|

|

|

|

Implied cash costs (US$000s) |

5,271 |

6,011 |

5,379 |

6,277 |

4,710 |

4,296 |

4,702 |

9.5 |

5,155 |

Cash costs (ZAR000s) |

53,025 |

63,693 |

59,077 |

74,406 |

64,057 |

66,810 |

65,771 |

(1.6) |

67,200 |

Implied cash costs (£000s) |

3,327 |

3,590 |

3,306 |

4,111 |

3,075 |

3,020 |

3,679 |

21.8 |

4,133 |

|

|

|

|

|

|

|

|

|

|

Forex (ZAR/£) |

15.9388 |

17.8279 |

17.8700 |

18.1318 |

20.8300 |

22.0942 |

17.8771 |

(19.1) |

16.2588 |

Forex (ZAR/US$) |

10.0600 |

10.6853 |

10.9827 |

11.9173 |

13.6000 |

15.4132 |

13.9875 |

(9.2) |

13.0363 |

Forex (US$/£) |

1.5844 |

1.6685 |

1.6269 |

1.5186 |

1.5328 |

1.4335 |

1.2778 |

(10.9) |

1.2478 |

|

|

|

|

|

|

|

|

|

|

Capex (US$000s) |

3,569 |

364 |

100 |

188 |

566 |

(8) |

1,494 |

(18,916.7) |

0 |

Capex (ZAR000s) |

35,900 |

4,800 |

1,100 |

2,200 |

7,700 |

400 |

20,900 |

5,125.0 |

0 |

Capex (£000s) |

2,252 |

159 |

62 |

122 |

370 |

8 |

1,169 |

15,263.2 |

0 |

Source: Edison Investment Research, Pan African Resources

Nameplate capacity at the BTRP is 100ktpm and management is working towards achieving this level in H217. For the moment, we continue to anticipate a moderation in grade and metallurgical recoveries. However, management has also recently been investigating the potential to reduce retention times, while maintaining metallurgical recoveries at relatively high levels. To the extent that it is successful, our forecasts may therefore prove to be relatively conservative.

In the longer term, approximately two-thirds of the tailings being treated at the BTRP originated from the Fairview concentrator at a grade of c 1.6g/t. The remaining third are from the same origin, but are supplemented with material from the Biox plant at a grade of 3-10g/t. As a result, a substantial portion of the resources being treated by BTRP exists at a grade in excess of 1.6g/t and there is therefore ample opportunity for management to pursue higher-grade strategies in order to increase financial returns.

Albeit achieved at the expense of higher costs in local currency terms, throughput, grade and metallurgical recovery at the ETRP all increased materially during the period compared to H216. Prima facie, this could be attributed to the processing of higher-grade surface material. In addition however, the plant also operated at 98.4% capacity utilisation.

Exhibit 5: ETRP operational results, H115-H217e

|

H215 |

H116 |

H216 |

H117 |

H117 vs H216 (%) |

H217e |

Tonnes processed from surface feedstocks (t) |

139,723 |

161,090 |

235,852 |

240,495 |

2.0 |

100,000 |

Head grade surface feedstocks (g/t) |

1.10 |

1.30 |

1.25 |

1.80 |

44.0 |

1.36 |

Surface feedstocks gold contained (oz) |

4,941 |

6,733 |

9,858 |

13,918 |

41.2 |

4,373 |

Tonnes processed tailings (t) |

507,444 |

729,085 |

715,959 |

940,489 |

31.4 |

1,080,000 |

Head grade tailings (g/t) |

0.30 |

0.30 |

0.30 |

0.30 |

0.0 |

0.32 |

Tailings gold contained (oz) |

4,894 |

7,032 |

6,906 |

9,071 |

31.4 |

11,111 |

Total tonnes processed (t) |

647,167 |

890,175 |

951,811 |

1,180,984 |

24.1 |

1,180,000 |

Head grade (g/t) |

0.47 |

0.48 |

0.55 |

0.61 |

10.5 |

0.41 |

Contained gold (oz) |

9,836 |

13,765 |

16,763 |

22,989 |

37.1 |

15,484 |

Recovery (%) |

54 |

63 |

54.7 |

65.0 |

18.8 |

61.0 |

Production tailings (oz) |

4,029 |

3,708 |

3,016 |

4,444 |

47.3 |

9,445 |

Production surface (oz) |

2,494 |

5,272 |

6,155 |

11,480 |

86.5 |

|

Total production (oz) |

6,523 |

8,980 |

9,171 |

15,924 |

73.6 |

9,445 |

Recovered grade (g/t) |

0.31 |

0.31 |

0.30 |

0.42 |

39.9 |

0.25 |

|

|

|

|

|

|

|

Gold sold (oz) |

6,523 |

8,980 |

9,171 |

15,924 |

73.6 |

9,445 |

Average spot price (US$/oz) |

1,206 |

1,108 |

1,221 |

1,224 |

0.2 |

1,235 |

Average spot price (ZAR/kg) |

466,647 |

484,298 |

605,265 |

550,380 |

(9.1) |

517,627 |

|

|

|

|

|

|

|

Total cash cost (US$/oz) |

688 |

528 |

638 |

545 |

(14.5) |

846 |

Total cash cost (ZAR/kg) |

266,453 |

230,857 |

316,105 |

245,178 |

(22.4) |

354,752 |

Total cash cost (US$/t) |

6.93 |

5.33 |

6.22 |

7.35 |

18.2 |

6.77 |

Total cash cost (ZAR/t) |

83.53 |

72.00 |

94.73 |

103.00 |

8.7 |

88.32 |

|

|

|

|

|

|

|

Implied revenue (US$000s) |

7,260 |

9,950 |

11,123 |

19,491 |

75.2 |

11,665 |

Revenue (ZAR000s) |

87,403 |

135,268 |

170,429 |

272,597 |

59.9 |

152,066 |

Implied revenue (£000s) |

4,609 |

6,491 |

7,714 |

15,254 |

97.7 |

9,348 |

|

|

|

|

|

|

|

Implied cash costs (US$000s) |

4,488 |

4,741 |

5,918 |

8,682 |

46.7 |

7,994 |

Cash costs (ZAR000s) |

54,060 |

64,500 |

90,168 |

121,434 |

34.7 |

104,218 |

Implied cash costs (£000s) |

3,004 |

3,096 |

4,107 |

6,793 |

65.4 |

6,410 |

|

|

|

|

|

|

|

Forex (ZAR/£) |

18.1318 |

20.8300 |

22.0942 |

17.8771 |

(19.1) |

16.2588 |

Forex (ZAR/US$) |

12.0400 |

13.6000 |

15.4132 |

13.9875 |

(9.2) |

13.0363 |

Forex (US$/£) |

1.5186 |

1.5328 |

1.4335 |

1.2778 |

(10.9) |

1.2478 |

|

|

|

|

|

|

|

Capex (US$000s) |

7,899 |

0 |

0 |

0 |

N/A |

0 |

Capex (ZAR000s) |

95,100 |

0 |

0 |

0 |

N/A |

0 |

Capex (£000s) |

5,284 |

0 |

0 |

0 |

N/A |

0 |

Source: Edison Investment Research, Pan African Resources

The grade of the dam being re-mined at the ETRP is 0.3g/t. However, the operation is commercially viable given its ability to fill unutilised capacity in the Kinross plant such that it therefore attracts only incremental operating costs (eg 14 additional employees). Re-mining is being conducted without breaching the dam wall and the tailings are being redeposited at Winkelhaak, thereby simplifying the environmental requirements (ie the Environmental Impact Assessment) with respect to re-filling the Kinross dam at a later date.

Nameplate capacity at the ETRP is 200ktpm and management’s target is to achieve 150-160ktpm (75-80% capacity utilisation on a sustainable, long-term basis). At ambient head grades (0.32g/t) and metallurgical recoveries (45%), this should result in the production of 10,000oz per annum at a total cash cost of US$1,012/oz (Edison calculation), based on prevailing forex rates and the ETRP’s current cost base of c ZAR130m per annum. In the meantime however, management will continue to source toll-treatment material with higher grades than the ETRP’s reserve and resource grades. Note that, in this respect, it is at a commercial advantage in that it is the only retreatment operator in the area and is therefore (effectively) the buyer of choice (or even the buyer of last resort) for tailings assets destined for retreatment in the region.

Effectively, the ETRP represents a substantial pilot plant, designed to prove recovery and cost parameters, before the development of the much larger Elikhulu project, which is currently poised to break ground imminently, subject to the conclusion of the final financing package. Compared with the ETRP’s 2.4Mtpa processing plant capacity, Elikhulu will process 12Mtpa to produce c 50koz per annum, at a cost of c ZAR1.7bn in initial capex and ongoing costs of c US$398-504/oz in opex.

Phoenix returned to profitability at the EBTIDA level during H117, despite a material decrease in head grade owing to re-mining from the lower grade Elandskraal/Kroondal tailings facility, as opposed to Samancor’s Buffelsfontein facility, and the fact that re-mining was limited by the recent drought in South Africa’s North West province. Compared with H216 however, metallurgical recoveries were materially higher following the installation of high energy agitation cells in the plant, as were sales of platinum group metals, while aggregate costs increased by only 3.6% in local currency terms.

Exhibit 6: Phoenix Platinum operating and financial performance, H114-H117

|

H114 |

H214 |

H115 |

H215 |

H116 |

H216 |

H117 |

H117 vs H216 (%) |

Plant feed - total (t) |

118,259 |

132,923 |

135,963 |

126,156 |

117,461 |

131,520 |

122,024 |

(7.2) |

Head grade (g/t) |

3.80 |

3.61 |

3.16 |

3.47 |

3.25 |

3.02 |

2.24 |

(23.5) |

Contained PGE (oz) |

14,448 |

15,432 |

13,813 |

14,081 |

12,274 |

12,382 |

8,788 |

(29.0) |

Plant recovery (%) |

24.0 |

27.3 |

34.0 |

53.8 |

39.0 |

36.3 |

57.0 |

15.5 |

Recovered PGE (oz) |

3,468 |

4,217 |

4,697 |

7,577 |

4,493 |

6,109 |

5,009 |

(18.0) |

|

|

|

|

|

|

|

|

|

Production and sales of PGE 6E (oz) |

2,987 |

4,217 |

4,711 |

5,534 |

4,493 |

3,846 |

4,574 |

18.9 |

Basket price received (ZAR/oz) |

9,380 |

10,016 |

9,815 |

9,423 |

8,716 |

9,228 |

9,284 |

0.6 |

Basket price received (US$/oz) |

932 |

937 |

894 |

791 |

641 |

599 |

664 |

10.9 |

Implied revenue (ZAR000s) |

28,018 |

43,934 |

46,238 |

52,144 |

39,161 |

35,490 |

42,465 |

19.7 |

Implied revenue (£000s) |

1,758 |

2,464 |

2,587 |

2,876 |

1,880 |

1,606 |

2,375 |

47.9 |

Total cash costs (ZAR/oz) |

8,484 |

9,868 |

6,817 |

6,453 |

7,653 |

10,318 |

8,991 |

(12.9) |

Total cash costs (US$/oz) |

843 |

924 |

621 |

542 |

563 |

669 |

643 |

(3.9) |

Total cash costs (ZAR/t) |

214 |

313 |

236 |

283 |

293 |

302 |

337 |

11.7 |

Implied total cash costs (ZAR000s) |

25,307 |

41,615 |

32,087 |

35,713 |

34,416 |

39,684 |

41,122 |

3.6 |

Implied total cash costs (£000s) |

1,588 |

2,334 |

1,796 |

1,970 |

1,652 |

1,796 |

2,300 |

28.1 |

Capex (ZAR000s) |

200 |

200 |

100 |

500 |

800 |

6,000 |

2,900 |

(51.7) |

Source: Edison Investment Research, Pan African Resources

Effective from 1 July 2016, the life of operations at Phoenix has decreased to nine years as a result of the cessation of mining operations at Lesedi, following IFM’s business rescue plan. Note that the right to the PGEs contained within the Lesedi resource continues to reside with Phoenix. Hence, the life of operations is likely to return to c 28 years in the event that the mine is re-opened once again. Nevertheless, it creates the risk of an impairment to PAF’s carrying value for Phoenix at the financial year end (albeit, this is clearly a non-cash cost). It also imposes on Phoenix a requirement for a new, permanent tailings storage facility (at an estimated cost of c ZAR30-40m). Nevertheless, Phoenix remains a ‘strategic’ investment for Pan African, providing it with an entry into the PGE market. It will also benefit in future periods as a result of a new offtake contract, signed with Northam Platinum, which lowers chrome penalties associated with the refining of Phoenix material.

Having been purchased effective from 1 April 2016, there are no meaningful comparative measures for the performance of the Uitkomst colliery under Pan African management. During H117 however, it was reported to have sold 327kt of coal from own and third-party sources at an average price of US$49/t after incurring production costs of US$41/t. The colliery’s contribution to Pan African’s EBITDA was reported to be ZAR38.0m, on which basis we estimate that it made a contribution to PAF’s EPS in the order of 0.1p/share during the period.

Pan African’s strategy is not to hedge its gold production forward, except in specific circumstances and to provide protection against specific risks. In July 2015 however, in order to protect its operational revenue, Barberton Mines entered into a short-medium zero cost collar via the following instruments:

■

A put option over 50,000oz of gold at a strike price of ZAR450,000/kg

■

A call option over 25,000oz of gold at a strike price of ZAR505,000/kg

As a consequence, the decline in the price of gold, from ZAR625,886/kg on 30 June 2016 to ZAR506,917/kg on 31 December 2016, resulted in a mark-to-market fair value profit of ZAR90.0m (£5.3m) in the period under review, compared with a loss of ZAR40.6m (£1.8m) in the prior year period, which is included in ‘other’ expenses in PAF’s income statement. Based purely on intrinsic value, a profit of this magnitude implies a net open position in the order of 24,000oz (which is as expected, given that some of the contracts will have been delivered into).

At the time of writing the rand price of gold is ZAR521,547/kg and we expect this to increase modestly to US$1,275/oz, or 535,457/kg, by 30 June 2017, resulting in a small equivalent loss in H217. Note that, for the purposes of our financial forecasting, we calculate mark-to-market fair value adjustments based on our gold price forecasts for the year in question and the intrinsic value of the remaining open option contracts (ie no time value is included). These are included in our forecasts of ‘other’ expenses in Pan African’s income statements.

In addition to its hedge position, PAF has a gold loan, valued at ZAR53.9m (cf ZAR110.4m previously) – equivalent to c 3,419oz of gold (cf 6,706oz of gold previously).

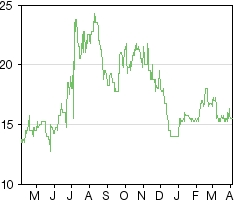

Pan African is the third-best performer of the London-listed gold miners, with its share price having risen by 111.1% in US dollar terms, since March 2010 (NB: more than one standard deviation above the mean, which has been a decline of 22.8% over the same period) and outperforming the gold price by 86.5%:

Exhibit 9: PAF share price performance vs peers, March 2010-present, factor (underlying data US$)

|

")

|

Source: Thomson Datastream, Edison Investment Research

|

Of as much significance, PAF remains cheaper than its South African peers on at least 70% of valuation measures (ie 21 out of 30 measures in the table below on an individual company basis) regardless of whether consensus or Edison forecasts are used:

Exhibit 10: Comparative valuation of PAF with respect to South African peers

|

EV/EBITDA (x) |

P/E (x) |

Yield (%) |

|

Year 1 |

Year 2 |

Year 1 |

Year 2 |

Year 1 |

Year 2 |

AngloGold Ashanti |

4.5 |

3.8 |

13.6 |

7.8 |

1.8 |

2.2 |

Gold Fields |

3.6 |

3.3 |

16.3 |

12.8 |

1.9 |

2.3 |

Sibanye |

4.1 |

2.9 |

21.0 |

9.8 |

3.1 |

4.6 |

Harmony |

3.4 |

3.1 |

9.5 |

9.0 |

2.1 |

2.6 |

Randgold Resources |

12.4 |

11.2 |

26.5 |

21.7 |

2.0 |

2.3 |

Average (excluding PAF) |

5.6 |

4.9 |

17.4 |

12.2 |

2.2 |

2.8 |

Pan African (Edison) |

5.9 |

3.9 |

12.0 |

6.7 |

4.5 |

5.2 |

Pan African (consensus) |

5.8 |

4.2 |

8.3 |

6.6 |

5.7 |

7.0 |

Source: Edison Investment Research, Bloomberg. Note: Priced at 31 March 2017.

Within the global context, meanwhile, it has the third-highest dividend yield of the 39 ostensibly gold counters paying dividends to shareholders (including royalty companies):

Exhibit 11: Global gold mining companies ranked by forecast dividend yield (%)

|

")

|

Source: Bloomberg (consensus data, priced 31 March 2017), Edison Investment Research

|

Pan African had £33.2m in net debt on its balance sheet as at 31 December 2016 after the payment of a £17.1m final dividend in late December (cf £22.8m as at 30 June 2016, £16.2m as at 31 December 2015 and £18.0m as at 30 June 2015). Net debt currently equates to a gearing (net debt/equity) ratio of 16.7% and a leverage (net debt/[net debt + equity]) ratio of 14.3%.

Our forecasts for Pan African’s immediate capital expenditure commitments related to Elikhulu by financial year are as follows:

Exhibit 12: Estimated Elikhulu capex requirements by financial year

£000s |

FY17 |

FY18 |

FY19 |

FY20 |

FY21 |

FY22 |

Total capex* |

20,492 |

54,236 |

33,935 |

8,626 |

18,391 |

18,391 |

Source: Pan African Resources, Edison Investment Research. Note: *Includes sustaining capex, but excludes phase 3 capex, which commences in FY26.

In the wake of shareholder approval to waive statutory pre-emption rights (confirmed on 9 February), PAF duly built a book of demand in excess of the 291.5m that it had been given the authority to issue. However, the company has elected not to use this funding option at this time, but instead to fund the Elikhulu development from cash and banking facilities until the final funding package is secured.

Whereas we had previously been expecting PAF to be net debt free ‘by the end of FY17’, all other things being equal, the imposition of capital requirements related to Elikhulu will now delay this until FY21.

Maintaining a dividend policy of 40% of free cash flows less sustaining capital, debt repayments and exceptional items, Pan African’s funding requirement, on our estimates, will evolve as follows in the period from FY16 to FY21:

Exhibit 13: Pan African estimated funding requirement, FY16 to FY21e

|

|

Source: Edison Investment Research, Pan African Resources

|

Note that PAF’s maximum funding requirement of £71.6m in FY19, as estimated by Edison, equates to ZAR1,150m at prevailing forex rates, or gearing (debt/equity) of 36.3% and leverage (debt/[debt+equity]) of 26.6%.

Debt is financed via a ZAR800m revolving credit facility (£49.8m at current exchange rates), of which ZAR511.5m (£31.8m) is currently drawn down, but which can be expanded to ZAR1,100m (£68.4m), plus a gold loan of ZAR53.9m (£3.4m) and a banking facility. In addition, Rand Merchant Bank (a division of First Rand) has provided Pan African with all the necessary approvals for a ZAR1bn underwritten five-year debt facility to fund the Elikhulu project.

The group’s revolving credit facility (RCF) debt covenants and their actual recorded levels within recent history are as follows:

Exhibit 14: Pan African group debt covenants

Measurement |

Constraint |

31 December 2016 (actual) |

30 June 2016 (actual) |

31 December 2015 (actual) |

Net debt:equity |

Must be less than 1:1 |

0.17:1 |

0.35:1 |

0.50:1 |

Net debt:EBITDA |

Must be less than 2.5:1 |

0.48:1 |

0.12:1 |

0.13:1 |

Interest cover ratio |

Must be greater than four times |

21.99 |

23.98 |

18.08 |

Source: Pan African Resources

Exhibit 15: Financial summary

|

|

£'000s |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017e |

2018e |

Year end 30 June |

|

|

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

PROFIT & LOSS |

|

|

|

|

|

|

|

|

|

|

Revenue |

|

|

79,051 |

100,905 |

133,308 |

154,202 |

140,386 |

168,404 |

203,409 |

204,785 |

Cost of sales |

|

|

(45,345) |

(46,123) |

(71,181) |

(106,394) |

(110,413) |

(108,223) |

(155,491) |

(133,356) |

Gross profit |

|

|

33,705 |

54,783 |

62,127 |

47,808 |

29,973 |

60,181 |

47,917 |

71,430 |

EBITDA |

|

|

28,540 |

45,018 |

53,276 |

44,165 |

28,448 |

57,381 |

45,185 |

68,292 |

Operating profit (before GW and except.) |

25,655 |

41,759 |

47,278 |

34,142 |

18,110 |

46,925 |

30,703 |

57,522 |

Intangible amortisation |

|

|

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

Exceptionals |

|

|

0 |

(48) |

7,232 |

(12) |

(198) |

(12,183) |

(127) |

(1,082) |

Other |

|

|

0 |

0 |

0 |

0 |

0 |

0 |

256 |

0 |

Operating profit |

|

|

25,655 |

41,711 |

54,510 |

34,130 |

17,912 |

34,742 |

30,832 |

56,440 |

Net interest |

|

|

762 |

516 |

197 |

(191) |

(2,109) |

(1,006) |

(2,034) |

(2,415) |

Profit before tax (norm) |

|

|

26,417 |

42,274 |

47,475 |

33,951 |

16,001 |

45,919 |

28,669 |

55,107 |

Profit before tax (FRS 3) |

|

|

26,417 |

42,226 |

54,707 |

33,939 |

15,803 |

33,736 |

28,798 |

54,025 |

Tax |

|

|

(9,248) |

(12,985) |

(12,133) |

(7,155) |

(4,133) |

(8,234) |

(8,346) |

(18,758) |

Profit after tax (norm) |

|

|

17,169 |

29,290 |

35,342 |

26,796 |

11,868 |

37,685 |

20,323 |

36,349 |

Profit after tax (FRS 3) |

|

|

17,169 |

29,242 |

42,574 |

26,785 |

11,670 |

25,502 |

20,452 |

35,267 |

|

|

|

|

|

|

|

|

|

|

|

Average number of shares outstanding (m) |

|

1,432.7 |

1,445.2 |

1,619.8 |

1,827.2 |

1,830.4 |

1,811.4 |

1,506.8 |

1,506.8 |

EPS - normalised (p) |

|

|

1.20 |

2.03 |

2.18 |

1.46 |

0.64 |

2.08 |

1.35 |

2.41 |

EPS - FRS 3 (p) |

|

|

1.20 |

2.02 |

2.63 |

1.47 |

0.64 |

1.41 |

1.36 |

2.34 |

Dividend per share (p) |

|

|

0.51 |

0.00 |

0.83 |

0.82 |

0.54 |

0.88 |

0.73 |

0.85 |

|

|

|

|

|

|

|

|

|

|

|

Gross margin (%) |

|

|

42.6 |

54.3 |

46.6 |

31.0 |

21.4 |

35.7 |

23.6 |

34.9 |

EBITDA margin (%) |

|

|

36.1 |

44.6 |

40.0 |

28.6 |

20.3 |

34.1 |

22.2 |

33.3 |

Operating margin (before GW and except.) (%) |

|

32.5 |

41.4 |

35.5 |

22.1 |

12.9 |

27.9 |

15.1 |

28.1 |

|

|

|

|

|

|

|

|

|

|

|

BALANCE SHEET |

|

|

|

|

|

|

|

|

|

|

Fixed assets |

|

|

97,281 |

86,075 |

249,316 |

223,425 |

220,150 |

230,676 |

249,580 |

304,708 |

Intangible assets |

|

|

38,229 |

23,664 |

38,628 |

37,040 |

37,713 |

38,682 |

40,418 |

42,154 |

Tangible assets |

|

|

59,052 |

62,412 |

209,490 |

185,376 |

181,533 |

190,725 |

207,893 |

261,284 |

Investments |

|

|

0 |

0 |

1,199 |

1,010 |

905 |

1,269 |

1,269 |

1,269 |

Current assets |

|

|

15,835 |

41,614 |

26,962 |

23,510 |

17,218 |

22,016 |

21,074 |

20,943 |

Stocks |

|

|

1,457 |

1,869 |

6,596 |

5,341 |

3,503 |

4,399 |

6,877 |

6,834 |

Debtors |

|

|

4,254 |

6,828 |

15,384 |

12,551 |

10,386 |

14,891 |

14,130 |

14,043 |

Cash |

|

|

10,124 |

19,782 |

4,769 |

5,618 |

3,329 |

2,659 |

0 |

0 |

Current liabilities |

|

|

(8,960) |

(11,062) |

(24,066) |

(24,012) |

(22,350) |

(32,211) |

(39,305) |

(70,501) |

Creditors |

|

|

(8,960) |

(11,062) |

(23,202) |

(19,257) |

(17,301) |

(25,230) |

(30,923) |

(27,114) |

Short-term borrowings |

|

|

0 |

0 |

(864) |

(4,755) |

(5,049) |

(6,981) |

(8,382) |

(43,387) |

Long-term liabilities |

|

|

(13,410) |

(14,001) |

(80,004) |

(63,528) |

(67,850) |

(69,506) |

(70,876) |

(72,232) |

Long-term borrowings |

|

|

(181) |

(869) |

(11,133) |

(8,141) |

(16,313) |

(18,456) |

(18,456) |

(18,456) |

Other long-term liabilities |

|

|

(13,228) |

(13,132) |

(68,871) |

(55,387) |

(51,537) |

(51,049) |

(52,420) |

(53,775) |

Net assets |

|

|

90,746 |

102,626 |

172,208 |

159,396 |

147,167 |

150,975 |

160,473 |

182,918 |

|

|

|

|

|

|

|

|

|

|

|

CASH FLOW |

|

|

|

|

|

|

|

|

|

|

Operating cash flow |

|

|

31,968 |

49,092 |

61,618 |

45,996 |

26,423 |

47,130 |

49,290 |

63,532 |

Net Interest |

|

|

762 |

516 |

314 |

(606) |

(2,109) |

(1,006) |

(2,034) |

(2,415) |

Tax |

|

|

(10,743) |

(11,616) |

(13,666) |

(8,536) |

(3,943) |

(7,777) |

(6,975) |

(17,403) |

Capex |

|

|

(21,712) |

(17,814) |

(27,197) |

(21,355) |

(19,554) |

(14,097) |

(33,386) |

(65,898) |

Acquisitions/disposals |

|

|

0 |

(1,549) |

(96,006) |

0 |

(760) |

(30,999) |

0 |

0 |

Financing |

|

|

1,545 |

259 |

47,112 |

349 |

(235) |

15,207 |

0 |

0 |

Dividends |

|

|

(5,376) |

(7,416) |

0 |

(14,684) |

(15,006) |

(9,882) |

(10,954) |

(12,821) |

Net cash flow |

|

|

(3,557) |

11,471 |

(27,826) |

1,164 |

(15,184) |

(1,425) |

(4,060) |

(35,005) |

Opening net debt/(cash) |

|

|

(12,756) |

(9,943) |

(18,913) |

7,228 |

7,278 |

18,033 |

22,778 |

26,838 |

Exchange rate movements |

|

|

925 |

(1,813) |

594 |

(839) |

(276) |

812 |

0 |

0 |

Other |

|

|

(181) |

(688) |

1,090 |

(375) |

4,705 |

(4,131) |

0 |

0 |

Closing net debt/(cash) |

|

|

(9,943) |

(18,913) |

7,228 |

7,278 |

18,033 |

22,778 |

26,838 |

61,843 |

Source: Company sources, Edison Investment Research

Contact details |

Revenue by geography |

The Firs Office Building,

1st Floor, Office 101, Cnr Cradock & Biermann Avenues, Rosebank, Johannesburg. South Africa.

+27(0)11 243 2900

www.panafricanresources.com |

|

Contact details |

The Firs Office Building,

1st Floor, Office 101, Cnr Cradock & Biermann Avenues, Rosebank, Johannesburg. South Africa.

+27(0)11 243 2900

www.panafricanresources.com |

Revenue by geography |

|

Management team |

|

Chairman: Keith Spencer |

CEO: Cobus Loots |

Keith is a qualified mining engineer with 47 years’ experience. He has managed some of the largest gold mines in the world including Kloof and Greenside colliery as general manager. In 1989 he was appointed consulting engineer for Gold Fields of South Africa encompassing Driefontein, Doornfontein, the Greenside colliery and Tsumeb base metals mine. He served as a board member of all GFSA gold mines. In 1999 he joined Metorex, becoming operations director in 2001. |

Cobus’ experience includes mining-specific acquisitions and finance as well as the management of both exploration and production mineral assets – most recently before 2009 as managing director of Shanduka Resources. Cobus has been a director of Pan African Resources since 2009 (Financial Director during 2009–2011 and a non- executive director during 2011–2013). He served as joint Chief Executive Officer alongside Ron Holding until assuming the office of Financial Director on 1 October 2013. He was appointed Chief Executive Officer on 1 March 2015 |

FD Deon Louw |

Independent Non-executive Director: Thabo Mosololi |

Deon has extensive finance and business experience, including investment banking, advisory and business administration in the finance and mining sectors. He has fulfilled the roles of Financial Director of Sentula Mining Limited, chief financial officer of Shanduka Coal, Director of Resource Finance Advisers and Head of Resource Structured Finance at Investec Bank. Deon was appointed as Financial Director on 1 March 2015. |

Thabo brings a wealth of experience in financial management, corporate governance and audit, having qualified as a chartered accountant with KPMG in 1994. Since then, he has served on various boards as a member and chairman of audit committees in the resources and other industries in South Africa. He is currently a director of MFT Investment Holdings, a family-owned investment company strategically placed to capitalise on B-BBEE investment opportunities. |

Management team |

Chairman: Keith Spencer |

Keith is a qualified mining engineer with 47 years’ experience. He has managed some of the largest gold mines in the world including Kloof and Greenside colliery as general manager. In 1989 he was appointed consulting engineer for Gold Fields of South Africa encompassing Driefontein, Doornfontein, the Greenside colliery and Tsumeb base metals mine. He served as a board member of all GFSA gold mines. In 1999 he joined Metorex, becoming operations director in 2001. |

CEO: Cobus Loots |

Cobus’ experience includes mining-specific acquisitions and finance as well as the management of both exploration and production mineral assets – most recently before 2009 as managing director of Shanduka Resources. Cobus has been a director of Pan African Resources since 2009 (Financial Director during 2009–2011 and a non- executive director during 2011–2013). He served as joint Chief Executive Officer alongside Ron Holding until assuming the office of Financial Director on 1 October 2013. He was appointed Chief Executive Officer on 1 March 2015 |

FD Deon Louw |

Deon has extensive finance and business experience, including investment banking, advisory and business administration in the finance and mining sectors. He has fulfilled the roles of Financial Director of Sentula Mining Limited, chief financial officer of Shanduka Coal, Director of Resource Finance Advisers and Head of Resource Structured Finance at Investec Bank. Deon was appointed as Financial Director on 1 March 2015. |

Independent Non-executive Director: Thabo Mosololi |

Thabo brings a wealth of experience in financial management, corporate governance and audit, having qualified as a chartered accountant with KPMG in 1994. Since then, he has served on various boards as a member and chairman of audit committees in the resources and other industries in South Africa. He is currently a director of MFT Investment Holdings, a family-owned investment company strategically placed to capitalise on B-BBEE investment opportunities. |

Principal shareholders |

(%) |

Shanduka Gold |

22.5 |

Allan Gray Investment Management |

19.6 |

Truffle Asset Management |

6.1 |

Prudential Portfolio Managers (South Africa) |

4.7 |

Old Mutual Investment Group (South Africa) |

4.4 |

Coronation Fund Management |

2.8 |

Miton Asset Management |

1.6 |

|

Companies named in this report |

Anglogold Ashanti (ANG SJ), Gold Fields (GFI SJ), Sibanye (SGL SJ), Harmony (HAR SJ), Randgold Resources (RRS LN) |

|

Edison is an investment research and advisory company, with offices in North America, Europe, the Middle East and AsiaPac. The heart of Edison is our world-renowned equity research platform and deep multi-sector expertise. At Edison Investment Research, our research is widely read by international investors, advisers and stakeholders. Edison Advisors leverages our core research platform to provide differentiated services including investor relations and strategic consulting. Edison is authorised and regulated by the Financial Conduct Authority. Edison Investment Research (NZ) Limited (Edison NZ) is the New Zealand subsidiary of Edison. Edison NZ is registered on the New Zealand Financial Service Providers Register (FSP number 247505) and is registered to provide wholesale and/or generic financial adviser services only. Edison Investment Research Inc (Edison US) is the US subsidiary of Edison and is regulated by the Securities and Exchange Commission. Edison Investment Research Limited (Edison Aus) [46085869] is the Australian subsidiary of Edison and is not regulated by the Australian Securities and Investment Commission. Edison Germany is a branch entity of Edison Investment Research Limited [4794244]. www.edisongroup.com DISCLAIMER

Copyright 2017 Edison Investment Research Limited. All rights reserved. This report has been commissioned by Pan African Resources and prepared and issued by Edison for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Opinions contained in this report represent those of the research department of Edison at the time of publication. The securities described in the Investment Research may not be eligible for sale in all jurisdictions or to certain categories of investors. This research is issued in Australia by Edison Aus and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securities and Exchange Commission. Edison US relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. As such, Edison does not offer or provide personalised advice. We publish information about companies in which we believe our readers may be interested and this information reflects our sincere opinions. The information that we provide or that is derived from our website is not intended to be, and should not be construed in any manner whatsoever as, personalised advice. Also, our website and the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. This document is provided for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Edison has a restrictive policy relating to personal dealing. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report. Edison or its affiliates may perform services or solicit business from any of the companies mentioned in this report. The value of securities mentioned in this report can fall as well as rise and are subject to large and sudden swings. In addition it may be difficult or not possible to buy, sell or obtain accurate information about the value of securities mentioned in this report. Past performance is not necessarily a guide to future performance. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (ie without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision. To the maximum extent permitted by law, Edison, its affiliates and contractors, and their respective directors, officers and employees will not be liable for any loss or damage arising as a result of reliance being placed on any of the information contained in this report and do not guarantee the returns on investments in the products discussed in this publication. FTSE International Limited (“FTSE”) © FTSE 2017. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 245 Park Avenue, 39th Floor 10167, New York US |

Sydney +61 (0)2 8249 8342 Level 12, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

|

Edison is an investment research and advisory company, with offices in North America, Europe, the Middle East and AsiaPac. The heart of Edison is our world-renowned equity research platform and deep multi-sector expertise. At Edison Investment Research, our research is widely read by international investors, advisers and stakeholders. Edison Advisors leverages our core research platform to provide differentiated services including investor relations and strategic consulting. Edison is authorised and regulated by the Financial Conduct Authority. Edison Investment Research (NZ) Limited (Edison NZ) is the New Zealand subsidiary of Edison. Edison NZ is registered on the New Zealand Financial Service Providers Register (FSP number 247505) and is registered to provide wholesale and/or generic financial adviser services only. Edison Investment Research Inc (Edison US) is the US subsidiary of Edison and is regulated by the Securities and Exchange Commission. Edison Investment Research Limited (Edison Aus) [46085869] is the Australian subsidiary of Edison and is not regulated by the Australian Securities and Investment Commission. Edison Germany is a branch entity of Edison Investment Research Limited [4794244]. www.edisongroup.com DISCLAIMER

Copyright 2017 Edison Investment Research Limited. All rights reserved. This report has been commissioned by Pan African Resources and prepared and issued by Edison for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Opinions contained in this report represent those of the research department of Edison at the time of publication. The securities described in the Investment Research may not be eligible for sale in all jurisdictions or to certain categories of investors. This research is issued in Australia by Edison Aus and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securities and Exchange Commission. Edison US relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. As such, Edison does not offer or provide personalised advice. We publish information about companies in which we believe our readers may be interested and this information reflects our sincere opinions. The information that we provide or that is derived from our website is not intended to be, and should not be construed in any manner whatsoever as, personalised advice. Also, our website and the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. This document is provided for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Edison has a restrictive policy relating to personal dealing. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report. Edison or its affiliates may perform services or solicit business from any of the companies mentioned in this report. The value of securities mentioned in this report can fall as well as rise and are subject to large and sudden swings. In addition it may be difficult or not possible to buy, sell or obtain accurate information about the value of securities mentioned in this report. Past performance is not necessarily a guide to future performance. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (ie without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision. To the maximum extent permitted by law, Edison, its affiliates and contractors, and their respective directors, officers and employees will not be liable for any loss or damage arising as a result of reliance being placed on any of the information contained in this report and do not guarantee the returns on investments in the products discussed in this publication. FTSE International Limited (“FTSE”) © FTSE 2017. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 245 Park Avenue, 39th Floor 10167, New York US |

Sydney +61 (0)2 8249 8342 Level 12, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

|

DPS")