Company description: Video-embedded advertising

Mirriad’s technology delivers inventory to brand owners and advertisers that was previously not available and is additive and complementary to their existing channels. Third-party research commissioned by the group from media intelligence firm Kantar Group has demonstrated very encouraging uplifts in perceived brand value, described below. For content owners, it offers a potentially substantial new revenue stream in a format more acceptable to consumers than traditional ad breaks.

Technology: Patented, innovative approach powered by AI

The five stages of the process are outlined below.

|

|

|

Source: Mirriad Advertising

|

Market seeking a more sophisticated approach

The company’s core IP lies in its ability to identify appropriate locations for product placement or brand advertising to be inserted into content post-production. This approach has considerable advantages over linear advertising and traditional product placement:

■

The message does not interrupt the content consumption. The traditional ad break is at best tolerated by viewers and ad-supported OTT platforms are at the limit of the number of advertising seconds per hour that will be tolerated by viewers. Pre- and mid-roll advertising online is disruptive, unpopular and often of poor quality. Adblockers and the ‘skip-ad’ button are both heavily used. Statista reports that in 2019, 25.8% of internet users in the US were employing adblockers on their connected devices.

■

Being able to insert product and signage post-production, rather than during the shoot, removes the long lead-times (which could be as long as two years) prevalent for traditional product placement.

■

Products and brand messaging is clearly in shot, so there ought to be no issues with viewability.

■

There is significant reduction in potential for breaches of brand safety, as the nature of the content is a known factor, meaning that the context is controlled.

■

For online advertising, increased concerns over the competing requirements of data privacy and ad targeting can be addressed by moving back up a level to be based on the demographics of the target audience of the content. However, from February 2020, Google extended its restrictions on real-time bidding to exclude contextual content categories in the bid requests sent to buyers participating in auctions, prompting a more sophisticated approach.

■

Independent research commissioned by Mirriad from Kantar Group has shown substantial comparative improvement in brand recognition and brand consideration, with the placements regarded as ‘authentic’ within its context. It can also be used to reinforce campaigns run in more traditional formats.

■

Existing content partnerships are shown below, alongside some brands that have used Mirriad’s ad format. The group now has concrete examples to demonstrate the effectiveness of campaigns from work aired, including one for a major global food and beverage brand. Research conducted across multiple cases has now shown double digit uplifts in marketing KPIs, with some cases showing that consumption frequency and/or spend can almost double.

Exhibit 2: Selection of content and brand relationships

Content partners |

Brands |

20th TV |

Corona |

Knorr |

Condé Nast |

Danone |

LG |

France TV |

Dove |

Nissan |

M6 |

Fitbit |

P&G |

MyTV Super |

Ford |

Pepsi |

RTL |

Freshpet |

Samsung |

Tastemade |

Geico |

SEAT |

Tencent |

HP |

Sherwin-Williams |

TF1 |

Ikea |

T-Mobile |

Univision |

Intel |

Unilever |

|

Johnson & Johnson |

|

Source: Mirriad Advertising

■

Mirriad’s approach has been to build scale. Over the last year, management reports that the group has established relationships with all top five global advertising agencies, over 50% of the top 100 global advertisers and 80% of the leading global entertainment companies.

A two-year exclusive platform partnership agreement was signed with Tencent in China, taking effect in July 2019. This provides for a minimum number of advertising seconds to be delivered by Mirriad to Tencent to then be sold on by Tencent, with an inbuilt minimum guarantee at a fixed fee. By the end of December, Mirriad had delivered 47% of the contracted advertising seconds, so were at that stage well on target, allowing for a ramp up. Early validation was gained with a campaign for C-Trip, where campaign research found that purchase consideration by viewers lifted from 41% to 51%.

Suite of patents in place

Mirriad has sought to protect its IP at all stages and now has 29 patents and patents pending across the USA, Europe and Asia. These include protection on dynamic emotional targeting (see below). The 19 patents in place globally cover:

■

Continuity in identifying and embedding brands across scenes – this ensures that ad insertions do not disappear or have any continuity issues.

■

Online catalogues for scene selections, which gives exposure to advertisers and agencies to scenes for ad insertions.

■

Generate embedding instructions, which allows automation of the ad insertion process.

■

Dynamic segment insertion, which allows for dynamic selection of branded segments per viewer, key for addressable solutions.

■

Content valuation, which allows the platform to forecast the value of unseen content, a prerequisite for inventory planning, selling and buying.

Exhibit 3: Excerpts of conversations with operational management

|

|

Source: Edison Investment Research

|

Amplification through use of emotional context

The technology is being developed beyond identifying suitable locations within content to a more sophisticated model that also identifies the emotional context. The principle of prevalent emotions influencing reactions to advertising is long and well established. However, further independent research commissioned by Mirriad indicates that the correlation of perception of brand value (“How much would you be willing to pay for…?”) is more significant for emotional intensity than it is for simple ‘positive’ emotions or ‘negative’ emotions.

Exhibit 4: Emotional intensity enhancement

|

|

Source: Mirriad Advertising, Edison Investment Research

|

Mirriad has showcased enhancements to its existing analytical tools that enable it to make data-driven judgements on the prevailing emotions shown in visual content. Getting this right – and automated – could lead to far greater usage of embedded advertising.

Competitive position of technology

There are other embedded content offerings in the market and being developed, but none are yet at or near the level of technical achievement or commercialisation achieved by Mirriad, which is running campaigns with credible content and brand partners.

Exhibit 5: Competitive technologies/ companies

|

Founded |

Fund-raising to date |

Ownership |

Notes |

Ryff |

2018 |

$5m |

VC backed, private |

Virtual computer-generated product placement |

Triplelift |

2019 |

$16.6m |

Private |

Bulk of revenue from in-feed native advertising |

Branded Entertainment Network |

2016 |

|

|

Spun out from Corbis, well established brand integration specialist |

Bidstack |

2018 |

£14m |

AIM quoted |

Native in-game advertising. Market cap £18m |

Source: Edison Investment Research

Ryff is at an earlier stage of corporate development, while Triplelift primarily works in native advertising, placing in stream advertising, which may be in the form of video. It has been developing a platform for product and brand placement for over-the-top/streaming content providers which is currently reported to be in beta-testing.

Branded Entertainment Network is an important player in the traditional product placement and influencer markets, increasingly using technology to identify suitable opportunities. Bidstack is focused solely on providing native in-game advertising to the global video games industry.

Disrupted market needs new monetisation models

Patterns of content consumption globally have shifted rapidly over the past decade, with the growth and proliferation of the streaming platforms. This has been partially at the expense of terrestrial broadcasters and the cable companies in the US, but also represents growth in the overall market. Zenith Optimedia estimates that the time spent watching online video globally has grown at a CAGR of 32% from 2013 and 2018 and that individuals watch an average of 84 minutes a day.

New platforms continue to be launched, with the global roll-out of lockdowns in the face of the spread of COVID-19 likely to have increased further the number of visits per month after the time frame illustrated in Exhibit 6 below. These names have since been joined by HBO Max, which launched in late May 2020, with Peacock (NBC/Comcast) slated for July 2020.

The subscriptions are not exclusive, with households typically stacking two or three streaming providers to cater for different tastes and requirements. However, the number of subscriptions is limited by household budgets and competitive pricing is crucial. The other differentiator is content. With new streamers such as Disney pulling their content from other platforms in order to drive traffic to their own, and the cost of producing original content very high (with additional marketing costs to aid discoverability), novel monetisation techniques should have good resonance.

Exhibit 6: Recent traffic to global streaming platforms

|

|

|

|

For advertising supported video on demand (AVOD) and for advertising-funded linear TV and video, there are limits to how much advertising per hour of content will be tolerated by the viewer.

Management with client and agency credibility

Stephan Beringer, CEO, joined the company in October 2018 from Publicis, where he had held a series of key roles, including president of data, technology and innovation and CEO of Vivaki, its programmatic buying offering. Stephan was previously chief growth and strategy officer for the digital technologies arm of Publicis. He therefore brought with him a deep understanding of the industry structure and relationships. Mirriad at that stage was pursuing a global sales approach, which resulted in business that did not necessarily scale and that was not inherently profitable. Stephan carried out a review of the business and chose to focus on fewer, but key, markets, namely the US, the UK, China, Germany and France.

The CEO, chairman and Bob Head, a non-executive director, all have options that trigger at various share price levels, starting at 30p, then 45p, 60p etc up to 120p. These total 5.5m, 1.35m and 0.4m respectively.

Moving beyond the repeat trial

To build genuine traction in the market, it is necessary to persuade all the relevant parties to specify embedded in-video as part of the campaign package. As well as having partnerships with the platforms, therefore, it is also important that Mirriad has the necessary relationships with the brand owners and with the agencies that buy media on their behalf. The contractual relationships vest with the content owner or distributor, but there needs to be a ‘pull’ element from their customer as well as the ‘push’ element.

The broadcast and video entertainment markets are a significant target themselves; management estimates this aspect of the advertising market for 2018 was $133bn globally. However, there are other attractive markets in which this technology could prosper. These are summarised in the exhibit below.

The music video market could be particularly fertile territory in the current market conditions. Artist revenues from streaming are notoriously parsimonious and most of music artists’ income stream is made from touring, merchandising and licensing. With concerts and tours effectively off the agenda, artists’ incomes are under great pressure and artists and their management should be more open to new means of monetisation, particularly where they are able to control the brand partners. The band Kodaline has already incorporated Mirriad’s technology in its lockdown video promoting Unicef. This is part of a new, larger collaboration between Mirriad and record label B-Unique.

Exhibit 7: Opportunity runway

|

|

Source: Mirriad Advertising, Edison Investment Research

|

Live events are a particularly interesting proposition, particularly if ad insertion can be combined with versioning for different audiences within the short available latency.

■

New business: The key sensitivity is over contract and new business wins. The scale of potential revenues mean that small numbers of additional clients could be truly transformational to the group’s financial outlook.

■

Lack of adoption: Even when contracts with content producers and distributors are in place, a lack of take-up by agencies and advertisers could compromise the ability of the group to establish its methodology within the ecosystem. Mirriad does not generally ‘own’ the clients’ customers, except in the case of music videos.

■

New applications: Management is looking beyond the film and TV sector to other areas in which the technology can be applied, such as music, influencer marketing and games. Success in penetrating these markets is not built into market forecasts.

■

Technology: While the tech stack has been developed over several years and is protected by a suite of patents, there may be hurdles in terms of further automation. With production centred in India, there is a possible risk of dislocation or business interruption.

■

Competitive position: As described above, the technology has a good degree of patent protection and alternatives appear to be at an earlier phase of technological and commercial development.

■

Financing: A successful round of financing completed in July 2019 has provided sufficient funding to last into Q321 or Q421 at current rates of cash burn. Edison’s assumption is that at least one further round of funding is likely to be needed to get the group into profitability.

■

Staff and key employee risk: The CEO has strong relationships in the industry, key to obtaining the trust of potential clients and users. To reflect this, he is highly incentivised through up to 5.5m options, triggering at share price levels from 30p through to 120p. The knowledge and experience within the tech team may also be difficult to replicate, given that this is a relatively new field.

■

Regulatory risk: Regulatory authorities may see it appropriate to place limits or warnings on content with embedded advertisements, in a similar way that influencers must now make it clear when their promotional activities are sponsored in various territories.

Revenue models

The group is at an early stage of its commercialisation and revenues are currently small, but with the potential for rapid growth, as outlined below.

Following the appointment of Stephan Beringer as CEO in late 2018, a change was implemented in how Mirriad approached its markets, which had previously been to look to sell as broadly as possible, on a project basis. The new strategy was (and is) to focus on the largest advertising markets: the US; China; the UK; France; and Germany. Revenue for FY18 was down on the prior year, with substantially lower revenues generated in China and in India. Gains in the US were offset by reductions in the UK.

As the new strategy started to take hold, H119 revenues at £429k were greater than those achieved for the whole of FY18. The new contract with Tencent (signed in June 2019 but running from April 2019 to March 2021) immediately benefited the top line. It carries a fixed monthly fee, with minimum guarantees based on volume and runs for 24 months on an exclusive basis. Looking at the H219 revenues for China, the uplift over H1 was £240k, which implies that the value of the contract on an annualised basis is between £0.5m and £1.0m. There is potential for considerable incremental growth as the methodology proves its worth and gains traction in the market.

While it would be to Mirriad’s advantage to negotiate similar revenue models with other clients, most of its existing contracts are on a straight revenue share model. We believe the share of advertising revenue under these to be around 20%.

Exhibit 8: Standard revenue model

|

|

Source: Mirriad Advertising

|

In this model, the content producer (or distributor) charges the advertiser (or agency), and a percentage of this fee is then paid across to Mirriad. Mirriad’s customer is therefore the content provider, rather than the ad agency. However, it is crucial to build and maintain strong relationships with the agencies and the brand owners in order for campaigns to include this new channel in the mix and be greenlit.

Management has said that it is currently in discussions with multiple entertainment majors to incorporate Mirriad’s advertising solution into their content (ie to ingest and appraise the agreed content and suggest inventory which can then be sold). A positive outcome of any of these negotiations could lead to a substantial uplift in revenues, which could be of the order of $1m+ for each agreement.

The group is also looking to build its revenues in other forms of online content where the market and mechanisms for selling ad inventory are less sophisticated, such as music videos, games and influencer marketing. These areas would give Mirriad the opportunity for direct sales of inventory to agencies, with an obvious benefit to achievable margin.

Given the current revenue inflection point, forecasting is particularly subjective, and Edison is not preparing forecasts at this time. While there is no formal guidance, market forecasts of a doubling of revenue in FY20 looks very achievable, despite the COVID-19 impact on the market. A summary of consensus financial estimates is shown below.

Exhibit 9: Market forecasts

|

FY19 |

FY20e |

FY21e |

FY22e |

Revenue (£m) |

1.1 |

2.2 |

6.0 |

11.0 |

Adjusted EBITDA (£m) |

(11.5) |

(11.2) |

(9.8) |

(6.8) |

Adjusted PBT (£m) |

(12.2) |

(11.6) |

(10.1) |

(7.1) |

Adjusted EPS (p) |

(8.1) |

(5.4) |

(4.8) |

(3.3) |

The largest element of cost is staff. The group currently employs just under 100 people, with technology and R&D based in the UK (30 people in FY19), and production based in India (37 people in FY19), with offices in London, New York, Shanghai and Mumbai. Operating costs for FY19 were down on the prior year, but this partly reflects a lower amortisation charge after the internally generated software development costs were written off in the prior year. Employee costs were up 18% on average headcount down 6% at 95 people, reflecting a change in mix. General and administration costs were down 23% on the prior year at £4.4m.

As the degree of automation in the processes increases, personnel costs will decrease as a proportion and become a semi-fixed cost, building in operational gearing. However, there may need to be a greater emphasis on client account management. The market forecasts indicate a gradual reduction in the operating and pre-tax loss, but profitability is not yet in the forecast horizon. Should current discussions with potential content partners come to fruition, however, this timescale could shorten considerably.

Balance sheet strengthened by placing

Mirriad has raised additional funds at regular intervals to support its development, including £25.0m net at its listing in 2017. In FY15–19, it raised a total of £63.8m net from the issue of shares. The latest fund raise was a placing and open offer in July 2019 at 15p, which generated £15.3m net (£16.2m gross).

As at end FY19, Mirriad had cash of £19.1m on its balance sheet, with lease-related debt only (following the adoption of IFRS 16) of £0.8m. At 30 April 2020, this figure had gone down to £15.8m.

Sufficient funding until at least Q321

The current rate of the group’s cash burn is under £1m per month (average of £825k over the first four months of FY20). If it were to continue at this rate, then existing cash resources would support the group until Q421, so we would assume that there would be a further fund raise at some point in FY21 to support further growth and move towards achieving profitability. Investors may at this point need to see some positive revenue progression, with the company delivering on growth.

Exhibit 10: Financial summary

|

|

£'000s |

2017 |

2018 |

2019 |

Year end 31 December |

|

|

IFRS |

IFRS |

IFRS |

INCOME STATEMENT |

|

|

|

|

|

Revenue |

|

|

874 |

416 |

1,140 |

Cost of Sales |

|

|

(181) |

(144) |

(178) |

Gross Profit |

|

|

694 |

272 |

961 |

EBITDA |

|

|

(10,359) |

(11,931) |

(11,505) |

Normalised operating profit |

|

|

(11,272) |

(14,429) |

(12,174) |

Amortisation of acquired intangibles |

|

|

0 |

0 |

0 |

Exceptionals |

|

|

0 |

0 |

0 |

Share-based payments |

|

|

(1,675) |

(176) |

(360) |

Reported operating profit |

|

|

(12,947) |

(14,605) |

(12,534) |

Net Interest |

|

|

1 |

58 |

23 |

Joint ventures & associates (post tax) |

|

|

0 |

0 |

0 |

Exceptionals |

|

|

0 |

0 |

0 |

Profit Before Tax (norm) |

|

|

(11,271) |

(14,371) |

(12,151) |

Profit Before Tax (reported) |

|

|

(12,947) |

(14,547) |

(12,511) |

Reported tax |

|

|

209 |

42 |

56 |

Profit After Tax (norm) |

|

|

(11,089) |

(14,329) |

(12,095) |

Profit After Tax (reported) |

|

|

(12,738) |

(14,505) |

(12,455) |

Minority interests |

|

|

0 |

0 |

0 |

Discontinued operations |

|

|

0 |

0 |

0 |

Net income (normalised) |

|

|

(11,089) |

(14,329) |

(12,095) |

Net income (reported) |

|

|

(12,738) |

(14,505) |

(12,455) |

Basic average number of shares outstanding (m) |

|

58.0 |

104.1 |

150.2 |

EPS - basic normalised (p) |

|

|

(19.11) |

(13.76) |

(8.05) |

EPS - diluted normalised (p) |

|

|

(19.11) |

(13.76) |

(8.05) |

EPS - basic reported (p) |

|

|

(21.95) |

(13.93) |

(8.29) |

Dividend (p) |

|

|

0.00 |

0.00 |

0.00 |

|

|

|

|

|

|

Revenue growth (%) |

|

|

- |

(52.4) |

174.0 |

Gross Margin (%) |

|

|

79.3 |

65.5 |

84.4 |

EBITDA Margin (%) |

|

|

-1185.0 |

-2868.7 |

-1009.7 |

Normalised Operating Margin |

|

|

-1289.4 |

-3469.4 |

-1068.3 |

BALANCE SHEET |

|

|

|

|

|

Fixed Assets |

|

|

2,280 |

770 |

1,125 |

Intangible Assets |

|

|

1,641 |

170 |

0 |

Tangible Assets |

|

|

426 |

414 |

913 |

Trade & other receivables |

|

|

213 |

186 |

212 |

Current Assets |

|

|

27,667 |

16,466 |

20,193 |

Stocks |

|

|

0 |

0 |

0 |

Debtors |

|

|

1,074 |

974 |

1,025 |

Cash & cash equivalents |

|

|

26,384 |

15,204 |

19,092 |

Other |

|

|

209 |

288 |

77 |

Current Liabilities |

|

|

(2,055) |

(1,659) |

(1,322) |

Creditors |

|

|

(2,055) |

(1,622) |

(1,298) |

Tax and social security |

|

|

0 |

(37) |

(25) |

Short term borrowings |

|

|

0 |

0 |

0 |

Other |

|

|

0 |

0 |

0 |

Long Term Liabilities |

|

|

0 |

0 |

0 |

Long term borrowings |

|

|

0 |

0 |

0 |

Other long term liabilities |

|

|

0 |

0 |

0 |

Net Assets |

|

|

27,892 |

15,577 |

19,996 |

Minority interests |

|

|

0 |

0 |

0 |

Shareholders' equity |

|

|

27,892 |

15,577 |

19,996 |

|

|

|

|

|

|

CASH FLOW |

|

|

|

|

|

Op Cash Flow before WC and tax |

|

|

(10,359) |

(11,931) |

(11,505) |

Working capital |

|

|

980 |

(332) |

(237) |

Exceptional & other |

|

|

0 |

0 |

0 |

Tax |

|

|

184 |

(7) |

248 |

Net operating cash flow |

|

|

(9,195) |

(12,269) |

(11,494) |

Capex |

|

|

(1,309) |

(1,016) |

(62) |

Acquisitions/disposals |

|

|

3 |

0 |

0 |

Net interest |

|

|

1 |

58 |

23 |

Equity financing |

|

|

25,069 |

1,926 |

15,290 |

Dividends |

|

|

0 |

0 |

0 |

Other |

|

|

(202) |

(169) |

(389) |

Net Cash Flow |

|

|

14,367 |

(11,470) |

3,367 |

Opening net debt/(cash) |

|

|

(12,017) |

(26,384) |

(15,204) |

FX |

|

|

0 |

0 |

0 |

Other non-cash movements |

|

|

0 |

290 |

520 |

Closing net debt/(cash) |

|

|

(26,384) |

(15,204) |

(19,092) |

Contact details |

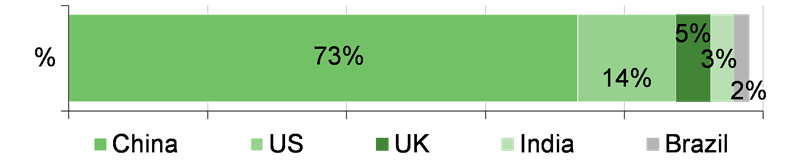

Revenue by geography |

96 Great Suffolk Street

London SE1 0BE

+44 (0) 207 884 2530

www.mirriad.com |

|

Contact details |

96 Great Suffolk Street

London SE1 0BE

+44 (0) 207 884 2530

www.mirriad.com |

Revenue by geography |

|

Management team |

|

Non-executive Chairman: John Pearson |

CEO: Stephan Beringer |

Former CEO of Virgin Radio and Virgin Radio Intl, John joined the Mirriad Board in 2017 and was appointed Chair in April 2019. He has extensive experience across the advertising, marketing, technology and digital fields and in corporate governance and M&A. |

Stephan joined the Board as CEO in September 2018 from Publicis Media, where he held a series of key roles. He was President of data, technology and Innovation and CEO of Vivaki, its programmatic buying offering. Stephan was previously Chief Growth and Strategy Officer for the digital technologies arm of Publicis. |

CFO: David Dorans |

CTO: Niteen Crawford-Prajapati |

David joined the Board in December 2017 from Mindshare UK, following a career spanning over 15 years at board level in the Technology, Media & Telecoms sector. David held the role of CFO at YouView, the UK connected television platform owned by the UK’s major broadcasters, had a senior operational role at Channel 4 and was General Manager at UKTV. |

Niteen joined Mirriad in April 2019 and is responsible for the technology vision and for accelerating Mirriad’s core technology development as well as the strategy for integrations with global broadcasters and the digital video ecosystem. With over ten years of experience in the digital media and technology space, he joined following a spell as Chief Architect at the European Broadcast Exchange, where he designed, and built the EBX technology offering from the ground up. Prior to EBX he spearheaded AppNexus and FreeWheel Europe expansions. |

Principal shareholders |

(%) |

IP Group |

16.1 |

Parkwalk Advisors Ltd |

14.9 |

M&G Inv Mgmt |

13.9 |

Ninety One |

5.2 |

Investec Wealth & Inv |

5.2 |

Janus Henderson |

3.4 |

Mole Valley AM |

3.3 |

Hargreaves Lansdown |

3.3 |

|

|

General disclaimer and copyright This report has been commissioned by Mirriad Advertising and prepared and issued by Edison, in consideration of a fee payable by Mirriad Advertising. Edison Investment Research standard fees are £49,500 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2020 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument. New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

|

|