bp plc is a client of Edison Group. Edison Group produced and distributed this content. Edison Group does not hold any position in bp plc.

A credible bull case for any income-oriented stock rests not on ambition, but on the mathematics of cash flow.

For investors evaluating bp’s renewed focus on shareholder returns (via dividends and buybacks), the central question is whether the company’s operational plans can generate sufficient, durable cash to support its commitments through the cycle.

The headline financial target, a compound annual growth rate (CAGR) of more than 20% for adjusted free cash flow between 2024 and 2027, is, without doubt, ambitious. And achieving it is fundamental to the investment thesis.

This analysis examines the primary engines intended to drive this growth. We look at the specific contributions the market has been told to expect from bp’s upstream and downstream businesses, together with the operational improvements that underpin these projections.

We will also evaluate the commercial capabilities and balance sheet enhancements that support the plan, alongside the execution and market risks that form a credible bear case.

The financial framework at a glance

Before dissecting the drivers, it is useful to establish the key metrics that frame bp’s financial strategy through 2027.

- Adjusted free cash flow growth: more than 20% CAGR target (2024–27).

- Capital expenditure frame: $13–15bn annually (2026–27).

- Shareholder distributions: 30–40% of operating cash flow expected to be distributed over time, subject to board approval.

- Net debt target: a reduction to a range of $14–18bn by end-2027.

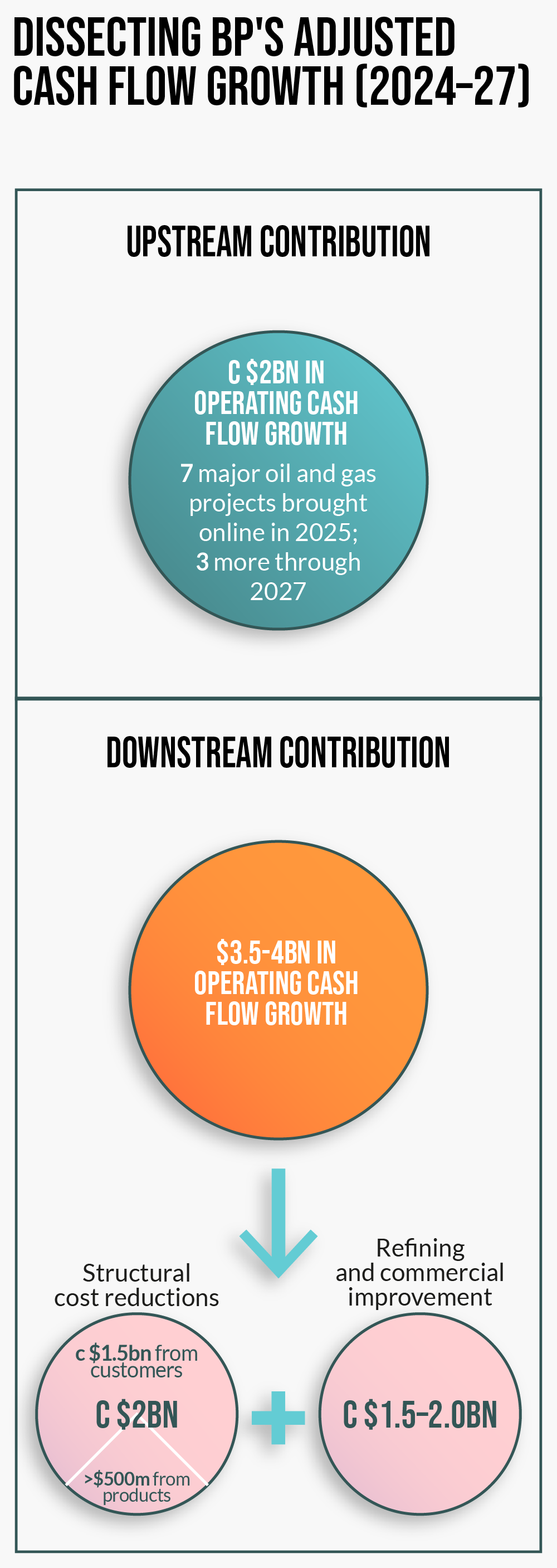

Dissecting the cash flow targets

The company’s cash flow growth targets are predicated on specific operational outcomes in its two main divisions.

First, management projects that the upstream oil and gas business will grow its operating cash flow by approximately $2bn between 2024 and 2027. This is tied to tangible increases in production to a range of 2.3–2.5m barrels of oil equivalent per day (mmboed) by 2030, as well as a focus on higher-margin projects.

Second, and more significant for near-term growth, is the turnaround in the downstream business. According to bp’s projections, this segment is expected to deliver $3.5–4.0bn in operating cash flow growth by 2027. The company has broken this down into two primary drivers:

- Structural cost reductions: a group-wide program is in place and is intended to deliver $4–5bn in structural cost reductions by 2027.

- A substantial portion is from downstream operations, including c $1.5bn from the Customers division and more than $500m from the Products division. These savings are linked to specific initiatives, including streamlining operations and consolidating suppliers.

- Refining and commercial performance: the remainder of the downstream growth is linked to improved refining performance. Management aims to lower the cash break-even of its refining assets by approximately $3 per barrel, driven by achieving a consistent 96% availability and better commercial optimization.

Underpinning the projections: Asset quality and trading

To what extent are these financial targets supported by operational and commercial advantages?

Firstly, production growth appears to be predicated on an asset base of commensurate quality, particularly in the US.

bp’s onshore business, bpx energy, holds more than 7bn barrels of oil equivalent resources across the advantaged Permian, Eagle Ford and Haynesville basins. In parallel, its deepwater Gulf of America portfolio provides access to the largest undeveloped resource in the basin, the Paleogene trend.

Secondly, beyond operational production, bp’s integrated model includes a well-performing supply and trading business. According to company disclosures, trading has delivered an average uplift of approximately 4% to the group’s return on average capital employed (ROACE) over the last five years.

This capability could be expected to provide resilient earnings during periods of market volatility.

De-risking the dividend: The net debt reduction plan

A key pillar supporting the sustainability of bp’s cash return expectation is its explicit intention to strengthen the balance sheet.

The company has set a primary target to reduce net debt from its mid-2025 level of $26.0bn to a range of $14–18bn by the end of 2027.

This is designed to be achieved primarily through a $20bn divestment program by the end of 2027, which includes the announced strategic review of Castrol and the plan to bring a strategic partner into Lightsource bp. A stronger balance sheet provides a bigger safety buffer for the dividend, making the income stream more secure.

The valuation context

A final component of the bull case is the company’s valuation relative to its peers. bp currently trades at a discount to the sector average. Furthermore, its dividend yield of approximately 6% (based on consensus estimates for FY26) is higher than the peer average.

The bull case assumes that successful execution of the strategic update will lead to a re-rating of the stock, closing this valuation gap over time.

Considering the bear case: A granular risk analysis

An objective analysis requires a consideration of the risks. The primary risks to this cash flow projection fall into two categories:

- Execution risk: the targets are ambitious. The bear case centers on the risk of slippage in delivering the $4–5bn cost reduction program and maintaining the project timelines for the 10 new major upstream projects scheduled by 2027, although we note 7 out of the 10 major project start-ups have already been delivered to date

- Market risk: while much of the plan is based on self-help, the absolute level of cash generation remains sensitive to commodity prices. bp’s financial targets are based on a reference price assumption of approximately $74/bbl Brent in 2027.

In conclusion

This analysis indicates that bp has constructed a clear, data-driven plan to expand its cash flow through 2027. The bull case is noteworthy because it is built on several pillars: a detailed plan for operational cash flow growth, a credible asset base, a strong commercial position, a significant deleveraging strategy, and a future offering the possibility of a favorable relative valuation.

Ultimately, of course, its credibility hinges on execution. However, if the company successfully delivers on its operational and cost-saving targets, we believe it is entirely reasonable to expect the stock to deliver the projected dividends and to execute the buybacks. This is, of course, subject to movements in the oil and gas markets.

To further analyze bp’s strategic update and its positioning within the global energy landscape, read the next report.

Forward-looking targets are based on current expectations and planning assumptions. Actual results may differ materially based on various factors including but not limited to commodity prices, operational performance, regulatory changes, and global economic conditions.

Shareholder distributions, including dividends and share buybacks, are subject to the discretion of the board and may vary based on factors including, but not limited to commodity prices, cash flow generation, balance sheet considerations, and general business conditions. Past distributions are not indicative of future distributions.