bp plc is a client of Edison Group. Edison Group produced and distributed this content. Edison Group does not hold any position in bp plc.

For investors focused on generating reliable income, the phrase “classic dividend growth stock” means something specific: a resilient core business, a clear commitment to increasing shareholder distributions, and the financial discipline to make those distributions sustainable.

bp, with its $90 billion market cap, has long been a staple in income-oriented portfolios. But in February 2025, the company announced a “fundamental strategy update” of its strategy. This raises an important question: does this new direction strengthen or weaken bp’s credentials as a dividend growth stock?

Let’s examine the evidence.

A Pragmatic Strategic Update: Focusing on growing shareholder value

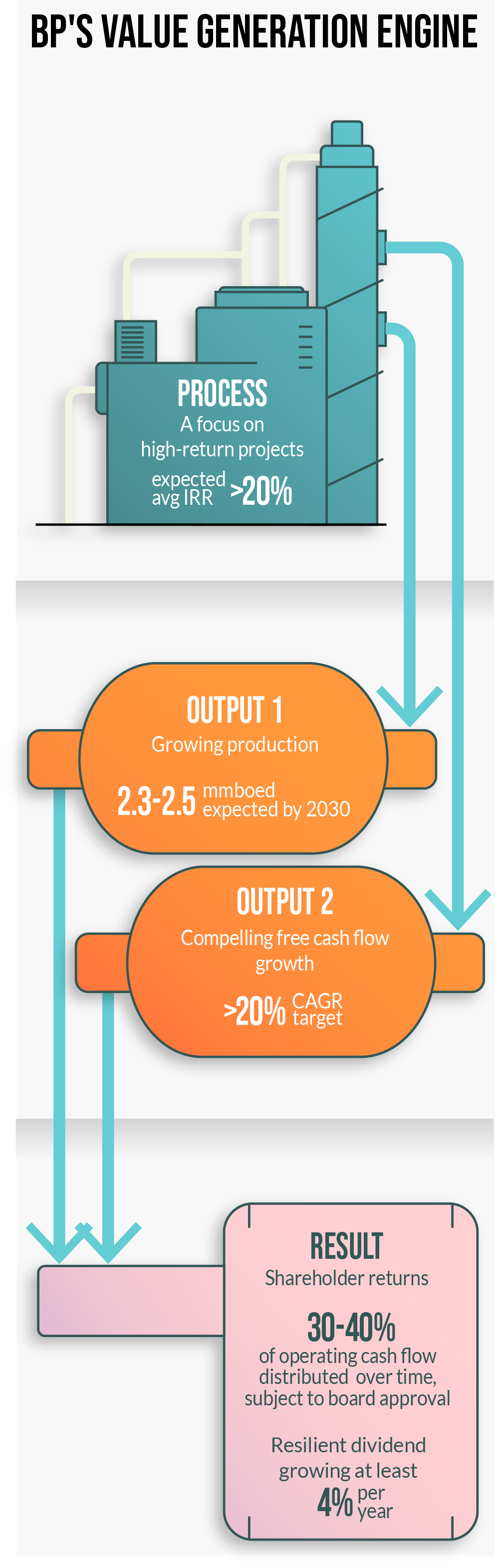

The company’s previous push into the energy transition went “too far, too fast.” With energy security and affordability back in focus globally, bp is reverting to what it does best—oil and gas.

This isn’t just rhetoric. Capital is being reallocated to the businesses that generate the highest returns and strongest cash flows—the foundation any sustainable dividend needs. The numbers tell the story: bp plans to invest around $10 billion per year in oil and gas from 2025 to 2027, representing roughly 75% of total capital expenditure.

And this investment is designed for growth. bp is expecting production of 2.3–2.5 million barrels of oil equivalent per day by 2030, supported by a high-quality portfolio including significant positions in the US Gulf of America and US onshore bpx energy business. Ten major new projects are scheduled to start up by 2027, with expected average internal rates of return exceeding 20%.

The Financial Framework: Where the rubber meets the road

A dividend growth strategy is only as credible as the financial framework supporting it. bp’s strategy update provides clear structure with three key pillars:

Free cash flow growth: The company is targeting compound annual growth of more than 20% in adjusted free cash flow from 2024 to 2027. If delivered, this would provide substantial capacity for shareholder distributions.

A growing dividend: bp has set an expectation for annual dividend increases of at least 4%. Based on current FY26 consensus estimates, this translates to a dividend yield of approximately 6%—above the peer average.

Disciplined buybacks: bp guidance is to distribute 30–40% of operating cash flow to shareholders over time and subject to board approval, some which will be delivered through the dividend, with the balance delivered through share buybacks. The company has already announced a $750 million buyback alongside its Q2 2025 results.

For investors, this framework presents a compelling proposition, particularly given bp currently trades at a discount to its peers.

The Bottom Line

So, does bp qualify as a “classic dividend growth stock”?

The strategic update has put the necessary components in place. The company has refocused on its most profitable, cash-generative business and established clear financial commitments.

Success will depend on consistent execution and supportive market conditions, but the framework is there:

- An expectation to grow the dividend by at least 4% annually, subject to board approval

- Underpinned by bp’s plan to achieve a CAGR of more than 20% for adjusted free cash flow from 2024 to 2027.

- A valuation at a discount to peers, with an above-average dividend yield

This is reinforced by renewed financial discipline, including a $4–5 billion structural cost reduction target and a plan to reduce net debt to a range of $14–18 billion by the end of 2027.

bp has constructed a clear, data-driven case. If the company executes its operational plans and adheres to its financial framework, it should exhibit the key characteristics income-focused investors typically seek.

To dive deeper into bp’s refocused project pipeline and the durability of its new financial framework, read the next report.

Forward-looking targets are based on current expectations and planning assumptions. Actual results may differ materially based on various factors including but not limited to commodity prices, operational performance, regulatory changes, and global economic conditions.

Shareholder distributions, including dividends and share buybacks, are subject to the discretion of the board and may vary based on factors including, but not limited to commodity prices, cash flow generation, balance sheet considerations, and general business conditions. Past distributions are not indicative of future distributions.