For investors whose strategy is focused on securing a reliable and growing income stream, the term ‘classic dividend growth stock’ implies a specific set of criteria:

- A resilient core business.

- A clear commitment to increasing shareholder distributions.

- A disciplined financial framework to ensure those distributions are sustainable.

As a major integrated energy company with a market capitalization of approximately $90bn, bp has long been featured in income-oriented portfolios.

However, in February 2025, bp announced what it termed a ‘fundamental reset’ of its corporate strategy. This prompts the question: Do these changes strengthen, or weaken, bp’s characteristics as a dividend growth stock?

This analysis examines the core components of bp’s new direction to provide an objective assessment. We will evaluate the reallocation of capital, the operational growth targets and explicit financial policies that now define the company’s investment case.

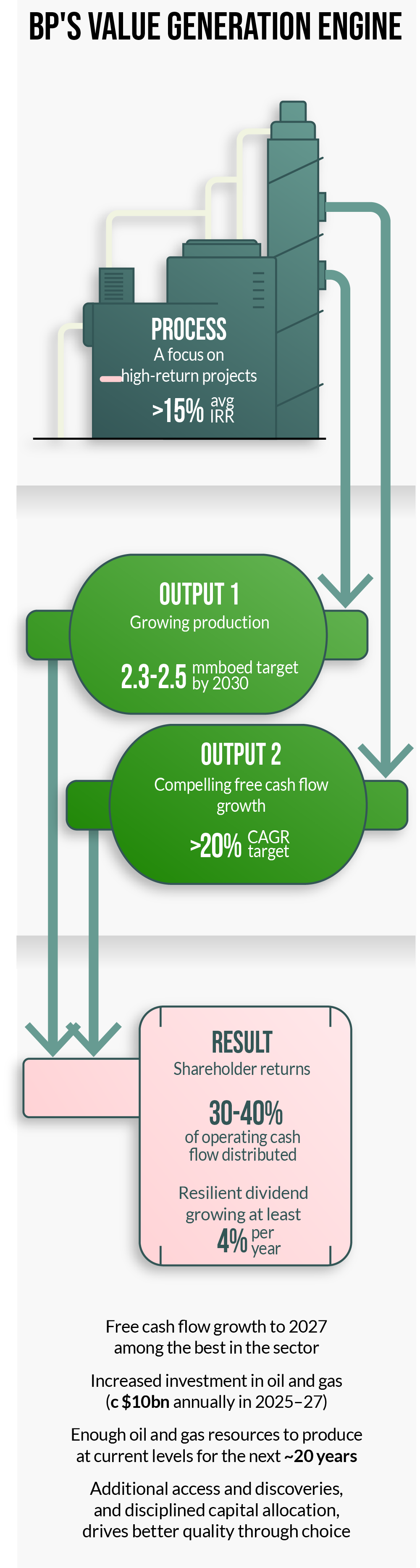

A pragmatic reset: Refocusing on the core cash engine

To evaluate bp’s future, one must first acknowledge its recent past. The company’s leadership concedes that its previous strategy, which accelerated investment into the energy transition, went ‘too far, too fast’. Global events have elevated the importance of energy security and affordability, prompting a strategic pivot back towards the company’s area of core strength: its upstream oil and gas business.

This is a significant rebalancing. Capital is being reallocated to the businesses that generate the highest returns and the most robust cash flow – the foundational requirements for any sustainable dividend policy. The plan is explicit: to increase investment in oil and gas to an average of approximately $10bn per year for 2025 to 2027. This accounts for around 75% of the company’s total capital expenditure, a clear signal of its new priority.

This increased investment is also programmed for growth. The company targets an increase in production to 2.3–2.5m barrels of oil equivalent per day (mmboed) by 2030. This growth is underpinned by a high-quality portfolio, including a significant presence in the US Gulf of America, including the recently sanctioned Tiber-Guadalupe project and the Permian Basin, and a pipeline of 10 major new projects slated to start by 2027, bolstered by 12 exploration discoveries year-to-date in 2025. These projects have an expected average internal rate of return (IRR) of more than 20%, although returns are ultimately dependent on execution and market conditions.

The financial framework for shareholder returns

A dividend growth strategy is only as credible as the financial framework that supports it. We believe bp’s reset provides a clear structure. In addition, it appears designed for resilience and shareholder returns. Its ultimate success will be contingent on delivering the underlying operational and financial plans.

The central financial objective is to deliver compelling growth in free cash flow. The company is targeting a compound annual growth rate (CAGR) of more than 20% for adjusted free cash flow from 2024 to 2027. Achieving this target would provide significant capacity for shareholder distributions. This cash flow target would also support a simplified policy for shareholder returns. bp has a stated intention to distribute 30–40% of operating cash flow to shareholders over time through two primary mechanisms:

- A resilient, growing dividend: the company has set an expectation for an annual increase in the dividend per ordinary share of at least 4%. Based on current consensus estimates for FY26, this policy represents a dividend yield of approximately 6%, which is above the peer average.

- Disciplined share buybacks: the remainder of the 30–40% distribution is planned to be delivered via share buybacks. As a tangible demonstration of this policy, bp executed a $750m share buyback during Q325, while announcing a further $750m share buyback expected to be completed prior to reporting its Q4 results.

For investors, this framework presents a clear value proposition, especially as the company currently trades at a discount to its peers. The market will be looking for bp to deliver on its new plan to address this valuation gap.

In conclusion

Does bp fit the description of a ‘classic dividend growth stock’?

Our analysis indicates that bp’s strategic reset has put in place the necessary components of such a plan. The company has re-centered its strategy on its most profitable and cash-generative business. However, the success of this strategy will depend on consistent execution and a supportive macroeconomic environment.

The key elements for consideration are:

- A stated policy to grow the dividend by at least 4% annually, supported by a target to return 30–40% of operating cash flow to shareholders.

- A plan to fuel this with >20% annual growth in free cash flow.

- A valuation that currently trades at a discount to its peers, coupled with a dividend yield that is above the peer average.

This framework is fortified by a new emphasis on financial discipline, including a $4–5bn structural cost reduction target and a plan to reduce net debt to $14–18bn by 2027. This successful focus on the financial foundation will be critical to determining the long-term sustainability of its shareholder return policy.

Ultimately, bp has constructed a clear, data-driven case. If it successfully executes its operational plans and adheres to its new financial framework, it would be reasonable to expect the stock to exhibit the key characteristics that income-focused investors typically seek.

To further analyze bp’s refocused project pipeline and the durability of its new financial framework, read the next report.