“Edison is the go-to for a new investor to get full understanding of the investment case and business. Edison’s distribution reaches investors that we want to connect with directly.”

Rare earth elements (REEs) sit at the heart of the green energy transition, modern defence and the coming wave of robotics. Despite their name, they are not especially rare in the Earth’s crust but they are rarely found in economically viable concentrations and processing them is extraordinarily complex. This complexity has allowed China to dominate the supply chain for decades. Today, as geopolitical tensions reshape global trade, governments and companies around the world are racing to find alternatives.

REEs are 17 metallic elements, consisting of the lanthanides, scandium and yttrium. REEs are typically found together in nature and extracted as a group, requiring a complex separation process to isolate them individually. They are categorised as light rare earth elements (LREEs), including neodymium (Nd) and praseodymium (Pr), and heavy rare earth elements (HREEs), including dysprosium (Dy) and terbium (Tb). These four elements are critical inputs for rare earth permanent magnets, which are a major application of REEs. HREEs are scarcer, more expensive and more geopolitically sensitive: dysprosium oxide currently trades at around US$239/kg and terbium oxide at around US$1,010/kg, against roughly US$123/kg for LREE Nd-Pr oxide.

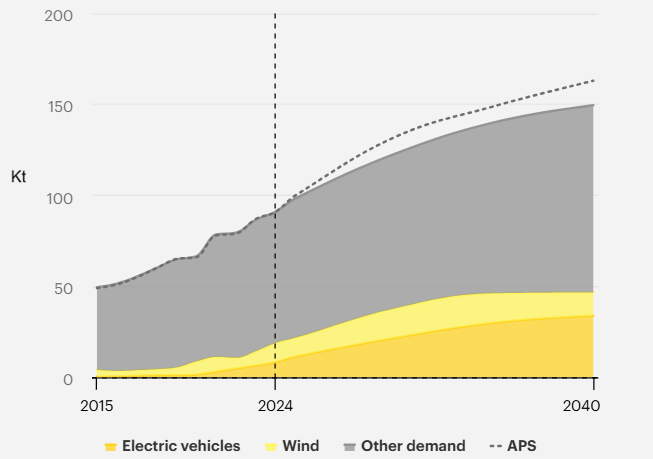

REEs have a range of critical applications in sectors such as defence, robotics and clean energy, but it is their use in permanent magnets that has made them strategically irreplaceable. Rare earth permanent magnets produce their own magnetic field continuously without an external power source and are used in electric vehicle (EV) motors, wind turbines, industrial motors and consumer electronics. The most powerful commercially available REE magnets are neodymium iron boron (NdFeB) magnets, which represented 96% of global rare earth magnet demand in 2025, according to IDTechEx, which forecasts the market will reach US$9.19bn by 2036 at a 3.9% compound annual growth rate.

Why does China dominate the supply chain?

China’s dominance is not a product of geology but the result of deliberate economic and industrial policy. Through the 1980s and 1990s, cheap capital, low labour costs and looser environmental enforcement made it uneconomic for Western producers to compete. According to the International Energy Agency’s (IEA’s) figures for 2024, China’s dominance spans the entire supply chain: the country is responsible for 60–70% of global mining and 91% of global refined rare earth output, while also controlling 94% of sintered NdFeB for magnet production. In April 2024 China introduced a traceability and quota regime under the Rare Earth Management Regulations, and the following year it imposed export controls on seven medium and heavy REEs, including Dy and Tb. In November 2025 China suspended exports of rare earth magnet technology and equipment for one year. These measures have created supply anxiety for manufacturers of EV motors, wind turbines and defence systems in Europe and North America.

What are the different types of REE deposits?

There are three distinct types of REE deposits:

Hard rock carbonatites: the most common type, which tends to be dominated by LREEs.

Ionic adsorption clay: these deposits carry a more meaningful heavy rare earth component and are able to be extracted without explosives or harsh acids, making them relatively low impact to mine.

Complex peralkaline silicate: the rarest deposit type, which tends to be the most HREE-rich but is challenging to process.

Understanding the REE deposit type matters because it largely determines the rare earth basket produced and the processing complexity involved.

Exhibit 2: Close-up of complex silicate

Source: iStock.com/Marieke Peche

Which countries are leading the charge on supply chain diversification?

The US, the second-largest miner after China, produced 45,000 tonnes of REEs in 2024 and is now pursuing a fully integrated mine-to-magnet approach. In July 2025, MP Materials (NYSE: MP, c US$10.3bn market cap) secured a public-private partnership with the US Defense Department, including US$400m of equity and a US$150m loan to accelerate domestic magnet production. In January 2026, USA Rare Earth (Nasdaq: USAR, c US$4.2bn market cap) signed a non-binding letter of intent with the US Department of Commerce’s CHIPS Program, covering US$277m of proposed federal incentives and a US$1.3bn proposed senior secured loan. The US has also imposed 37.1% import tariffs on Chinese NdFeB permanent magnets.

A significant share of new mined supply is expected to come from ionic clay deposits, particularly in Brazil. The US International Development Finance Corporation (DFC) has committed US$465m to expand Serra Verde’s Pela Ema project in Goiás state, Brazil’s first large-scale rare earth mine, with projected output of 4,800 to 6,500 tonnes of rare earth oxides by 2027, potentially supplying 5% of global demand. However, there is an inherent tension in the investment: Serra Verde’s concentrate currently has only one realistic destination, Chinese refineries, as Western refining infrastructure will not come online until around 2028. Brazil holds 21Mt of REE reserves according to the United States Geological Survey, the largest outside China, and the broader region is attracting growing attention as a source of diversified supply.

Myanmar, the third-largest miner, accounted for around 45% of global mined HREE supply in 2024 from ionic clay deposits, but the seizure of its Kachin State mining region by the Kachin Independence Army in November 2024 caused a sharp drop in supplies to Chinese refineries, exposing the fragility of the global HREE supply chain.

Australia is emerging as the most credible alternative refining hub, with the IEA expecting it to enter the top three producing countries within a decade, supported by Iluka Resources’ Eneabba refinery (ASX: ILU, c A$2.27bn market cap) and Arafura Rare Earths’ Nolans Project (ASX: ARU, c A$1.09bn market cap). This positions Australia as a key pillar in supply diversification.

In Africa, the US has committed US$50m through the DFC to a rare earth processing project in South Africa, and the European Commission has signed raw material partnerships with South Africa, Rwanda, the Democratic Republic of the Congo, Zambia and Namibia.

What is Europe’s position in the rare earths industry?

Europe currently produces no rare earths from its own mines. Its processing capability rests on two facilities: Solvay’s La Rochelle plant in France (XBRU: SOLB, c €2.85bn market cap) and Neo Performance Materials’ Silmet plant in Estonia (TSX: NEO, c C$887m market cap). Neither of these facilities is anchored to a European mine feed. The EU’s Critical Raw Materials Act (CRMA), in force since May 2024, sets 2030 strategic raw materials targets of sourcing 10% of annual consumption from EU extraction, 40% from EU processing and 25% from EU recycling, while limiting dependency on any single third country to 65%. However, Europe currently has no producing rare earth mines, and several of the first CRMA strategic projects are located outside the EU. Many of these projects are also weighted toward LREEs, rather than the heavier elements most exposed to supply concentration.

Greenland, once considered a potential nearby supply source, has become geopolitically complex following the Trump administration’s stated desire to acquire the territory, meaning any development there may not primarily serve EU strategic objectives. This makes a mine within Europe itself a potential solution to European supply security, and it is in this context thatLeading Edge Materials’* Norra Kärr deposit (TSX: LEM, c C$77.6m market cap) in Sweden becomes important.

Could Norra Kärr be the answer to Europe’s rare earths problem?

Norra Kärr is unique for two reasons: it is geographically within the EU and its rare earth basket is heavily weighted towards the most strategically valuable HREEs, with heavy rare earth oxides representing approximately 52% of the total basket – a characteristic of a complex peralkaline silicate deposit. Edison estimates current European Dy demand at around 180–200tpa. Norra Kärr’s 2021 preliminary economic assessment projects average annual dysprosium oxide output of 248 tonnes, suggesting the deposit could supply all of Europe’s dysprosium needs. The project is currently in the permitting phase, and in December 2025 both relevant County Administrative Boards endorsed the new mining lease application.

What should investors watch?

The IEA projects that current mine supply is broadly sufficient to meet demand for the next few years. It identifies the major long-term concern as not a demand-supply gap but an exceptional level of geographical concentration that leaves the market exposed to price volatility and supply disruption. Although China’s share of refining is expected to decline from 91% currently to 75% by 2040 as early-stage projects outside China come online, it is still expected to dominate global rare earth refining well into the next decade.

Recycling is emerging as a partial solution, with IDTechEx predicting rare earth magnet recycling will increase 6.5 times over the next decade, reaching 10% of global supply by 2036, supported by growing commitments from automotive original equipment manufacturers, including Ford, BMW and JLR. But recycling alone cannot close the gap, and investment in new primary supply remains essential. For European investors, the combination of binding CRMA targets, lack of domestic mine production and an accelerating policy environment creates a compelling structural case for projects that can credibly supply European industry from within the EU. Norra Kärr’s position as the only significant HREE deposit in Europe places it at the centre of that supply transition.

Edison insight

REEs are central to EVs, wind turbines and advanced defence systems, yet supply remains highly concentrated. China controls around 91% of global refining capacity and continues to shape market dynamics through export policy. While governments in the US, Europe and Australia are accelerating efforts to diversify supply, refining plants and new mines take years to develop, limiting how quickly concentration can fall. Europe is particularly exposed, with no active domestic mine feed despite binding CRMA targets for local extraction by 2030. For investors, the key issue is not demand growth, but whether non-Chinese supply can scale in time to reduce strategic vulnerability.

Megatrends: resource scarcity, energy transition, disruptive technologies, automation and industrial innovation, future of transport, climate change

*Leading Edge Materials is a client of Edison Investment Research.

Decarbonising the built environment – Steel and cement in focus

This report is the second in our series on decarbonising the built environment. While our first report focused on building materials, this report tackles two of the sector’s most critical and emissions-intensive inputs: cement and steel. Together, these materials account for approximately 16% of global CO2 emissions and sit at the heart of modern construction. They are also difficult to decarbonise as their respective production processes are heat intensive, assets are long lived and margins are typically thin. Regulation, customers and capital are increasingly pushing for lower-carbon materials and new technologies are emerging, including clinker substitution and carbon capture in cement, and greater scrap use, electrification and hydrogen-based routes in steel. The investment cycle will mean that the transition takes time, but materials producers will need to adapt.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping us understand which section of the website you find more interesting and useful. See our Cookie Policy for more information.

Strictly necessary and functional

These cookies are used to deliver our website and content. Strictly necessary cookies relate to our hosting environment, and functional cookies are used to facilitate social logins, social sharing and rich-media content embeds.

Advertising

Advertising Cookies collect information about your browsing habits such as the pages you visit and links you follow. These audience insights are used to make our website more relevant.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Performance

Performance Cookies collect anonymous information designed to help us improve the site and respond to the needs of our audiences. We use this information to make our site faster, more relevant and improve the navigation for all users.

Please enable Strictly Necessary Cookies first so that we can save your preferences!