“Edison is the go-to for a new investor to get full understanding of the investment case and business. Edison’s distribution reaches investors that we want to connect with directly.”

Financial influencers, or ‘finfluencers’, are content creators who share investment advice, market commentary and personal finance tips on social media platforms such as TikTok, Instagram and YouTube. Many finfluencers provide genuine value by improving financial literacy. UK creators such as Mark Tilbury, who uses humour and sketches to teach wealth-building strategies to his more than seven million YouTube subscribers, and Andreea Ion and Jamie Galvin of Stocks and Savings, who demystify investing for young people by documenting their own journey to financial independence, have built substantial followings by translating complex financial concepts into digestible content. Others, such as Aash Thapa, Nischa Shah and Cameron Smith (cazzatime), focus on empowering younger or less-experienced investors with the basics of budgeting, tax and long-term investing. These educators help bridge the gap between complete ignorance and the confidence to enter the market.

Exhibit 1: Top UK finfluencers by subscriber count across social media platforms

Source: Edison Investment Research. Note: As at 7 January 2026. Platforms include Instagram, TikTok and YouTube, and exclude Facebook, LinkedIn and X. Subject to rounding and not a definite list.

Why have finfluencers become so popular?

The term emerged in the late 2010s as social media began to democratise access to financial information that had long been locked behind institutional paywalls or buried in jargon-heavy reports. Finfluencers helped dismantle these barriers by making finance accessible, relatable and entertaining. The shift to finfluencer-led education accelerated during the COVID-19 pandemic, when retail trading activity surged as locked-down individuals sought new income streams and hobbies. By packaging financial education in the language of the internet (memes, quick cuts and personal storytelling), finfluencers are able to share financial knowledge with a generation that might otherwise have been excluded from wealth-building opportunities.

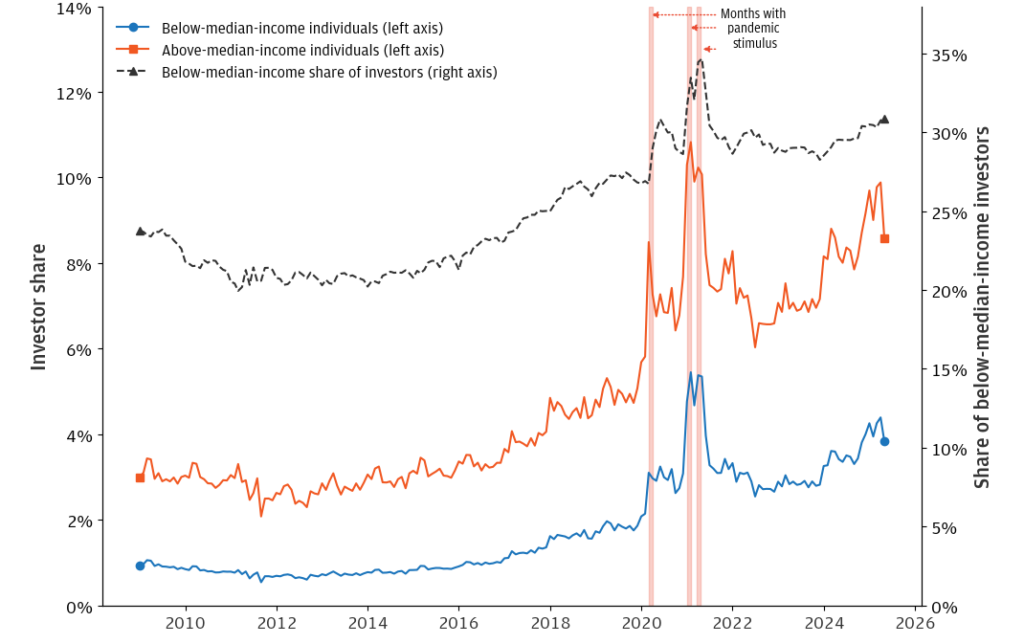

Exhibit 2: Increase in retail investor participation across income groups during COVID-19 pandemic

Source: JPMorganChase Institute. Note: Plot shows the monthly share of the sample making net transfers to investments and the share of investors that are below-median-income. Individuals are categorised by their full-sample average age-adjusted real income.

A survey conducted by the Financial Conduct Authority (FCA) found that 85% of 18- to 40-year-olds in the UK now use social media to inform investment decisions and almost two-thirds (62%) of 18- to 29-year-olds follow finfluencers. This trend reflects a broader shift in how younger investors consume information. Whereas previous generations turned to financial advisers or newspaper columns, today’s retail investors often encounter investment ideas through a 60-second video while scrolling on their phone.

What are the risks of following finfluencer advice?

The very accessibility that makes finfluencers appealing also creates vulnerabilities. Social media engagement tends to reward sensationalism over nuance, and finfluencers monetise attention, not investment success. Their income typically comes from advertising, sponsorships, affiliate commissions and course sales, meaning that keeping audiences engaged often matters more than delivering consistent returns.

A 2025 study titled VideoConviction evaluated thousands of finfluencers’ stock recommendations using multimodal analysis of video content. The researchers found that although finfluencers often expressed high conviction in their picks, this confidence had little relationship to subsequent stock performance. In fact, betting against those recommendations ‘outperform[ed] the S&P 500 by 6.8% in annual returns.’

Retail investors can also fall into the trap of ‘copy-trading’, which is mimicking the moves of the personality they follow without understanding the underlying business or the creator’s financial motivations. This behaviour leads to fragile portfolios built on hype rather than fundamentals. When a finfluencer moves on to the next trend, followers are left holding positions they neither understand nor can evaluate independently.

Analysing stock recommendations from over 29,000 finfluencers, a Swiss Finance Institute research paper found that many popular stock-pickers exhibited negative skill, meaning that following their advice often yielded worse returns (-2.3%) than random chance. Notably, the finfluencers with the largest followings were not those with the strongest track records, but rather those who produced the most engaging content.

The credibility spectrum among finfluencers is wide, ranging from legitimate educators to paid promoters to outright fraudsters. The risks are amplified by the fact that 53% of people using social media for investment guidance do not always verify the reliability of the finfluencer content they consume (Barclays).

High-profile examples illustrate these dangers. US YouTuber Graham Stephan, once widely respected for his real estate content, faced significant criticism and legal scrutiny for promoting FTX and other controversial fintech products that ultimately harmed some followers. More recently, in early 2025, Argentina’s President Javier Milei, acting as a ‘finfluencer-in-chief’, promoted a cryptocurrency token ($LIBRA) that crashed shortly after launch. The incident resulted in investigations and a significant loss of public trust, showing that even figures with substantial authority can mislead investors when they step outside the bounds of regulated advice.

The contrast with institutional-grade research is stark. Professional analysts operate under regulatory oversight, disclose conflicts of interest, explain their methodology and typically have their compensation tied to accuracy rather than virality. When an analyst issues a recommendation, it is accompanied by price targets, risk factors and an established track record. Finfluencer content rarely offers such rigour.

How is the FCA responding to finfluencer risks?

The era of unchecked promotion is coming to an end. The FCA has launched a significant crackdown on finfluencers, aligning its efforts with the UK’s Online Safety Act. Steve Smart, the FCA’s joint executive director of enforcement and market oversight, emphasised that finfluencers ‘need to check the products they promote to ensure they are not breaking the law and putting their followers’ livelihoods and life savings at risk.’

The regulator has been highly active, issuing over 50 warning alerts and more than 650 takedown requests to social media platforms for unauthorised promotions, with some cases escalating to criminal charges. In a landmark move in September 2025, the FCA initiated proceedings against three high-profile individuals (Charles Hunter, Kayan Kalipha and Luke Desmaris) accusing them of promoting unauthorised financial products and encouraging investments in high-risk foreign exchange trading schemes without proper authorisation. All three have pleaded not guilty, with trials scheduled for 2027. These prosecutions serve as a stark warning to content creators that the ‘Wild West’ days of financial promotion are coming to an end.

Edison’s view

Finfluencers have permanently reshaped the financial information landscape, largely for the better in terms of accessibility. However, entertainment value and investment quality are not the same thing. The more effective approach for retail investors is to enjoy the engaging content finfluencers produce while verifying the facts through institutional-grade research.

The fundamental principle remains unchanged: quality investment research requires expertise, transparency and accountability. In an era where anyone with a smartphone can broadcast investment advice to millions, the ability to critically evaluate sources has become an essential investment skill. Those who thrive will be the investors who pair the accessibility of modern financial media with the discipline of traditional investment analysis.

In a year that has been characterised by a roller-coaster ride in sentiment, the end outcome is likely to be one that is very positive for those investors who blocked out the noise, held their noses and stayed in equity markets.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping us understand which section of the website you find more interesting and useful. See our Cookie Policy for more information.

Strictly necessary and functional

These cookies are used to deliver our website and content. Strictly necessary cookies relate to our hosting environment, and functional cookies are used to facilitate social logins, social sharing and rich-media content embeds.

Advertising

Advertising Cookies collect information about your browsing habits such as the pages you visit and links you follow. These audience insights are used to make our website more relevant.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Performance

Performance Cookies collect anonymous information designed to help us improve the site and respond to the needs of our audiences. We use this information to make our site faster, more relevant and improve the navigation for all users.

Please enable Strictly Necessary Cookies first so that we can save your preferences!