“Edison is the go-to for a new investor to get full understanding of the investment case and business. Edison’s distribution reaches investors that we want to connect with directly.”

Gamification refers to the application of game-design elements and principles to non-game contexts. In investing, this involves incorporating such features into financial trading platforms and apps to keep users engaged, active and returning frequently, similar to how mobile games encourage repeated play. For retail investors, particularly younger users trading on smartphones, this can make the experience feel more akin to sports betting or casino apps than to a traditional investment portal.

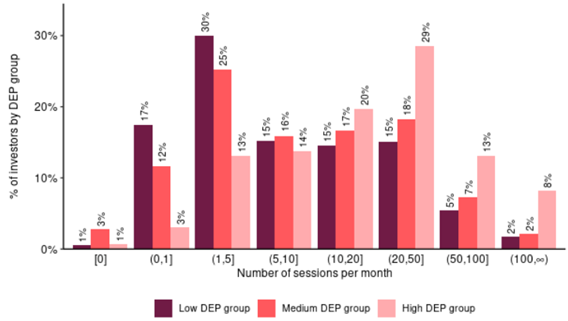

Common examples of digital engagement practices (DEPs) include flashing prices, push notifications and celebratory animations, such as confetti falling after a trade is executed, which deliver an immediate dopamine hit similar to completing a level in a game. Other features include prize draws, leaderboards that rank users by percentage returns, ‘scratch card’-style rewards for depositing funds or referring friends, and badges awarded for reaching specific activity milestones. These DEPs are closely associated with increased user engagement. A report published by the Financial Conduct Authority (FCA) found that users of high-DEP apps logged in significantly more frequently, with 21% averaging more than 50 sessions per month, compared with 10% of users of medium-DEP apps and just 7% of users of low-DEP apps.

Exhibit 1: Number of app sessions per month by DEP group

Source: Occasional Paper 66, Playing the market: a behavioural data analysis of digital engagement practices and investment outcomes by John Gathergood, Cameron Gilchrist, Mark D. Griffiths, Lucy Hayes, Emily Morris, Stephen O’Neill, Jesal D. Sheth and Neil Stewart, FCA .

Social features are also prevalent, with platforms such as eToro or ZuluTrade popularising ‘social trading’ feeds and copy-trading functions, where users can automatically replicate the moves of ‘top performers’ or influencers . Even the interface itself, often characterised by bright colours and a frictionless ‘swipe-to-buy’ mechanic, is designed to minimise the psychological weight of spending money.

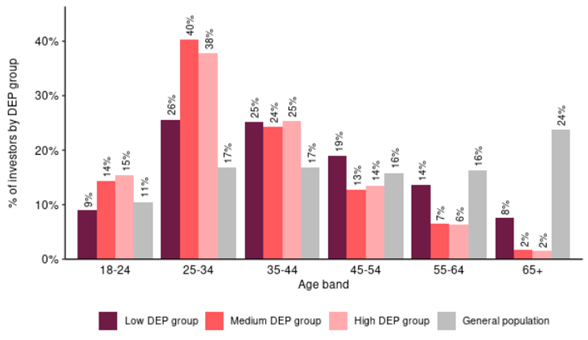

The FCA reported that in the first four months of 2021, 1.15m accounts were opened across four trading app companies. Between 2021 and 2024, these same companies continued to see strong growth, with an average of 70,000 new accounts opened each month (FCA). By 2024, trading apps were used by 3% of UK adults (c 1.6 million people), almost half of whom (47%) were aged between 18 and 34 (FCA). Notably, the average user of high-DEP apps was six years younger than users of low-DEP apps and 15 years younger than the median age of the UK adult population (c 48 years old, FCA). This younger skew may reflect the ease and convenience of these platforms, which enable retail investors to trade stocks, exchange-traded funds and other securities with minimal friction.

Exhibit 2: Age of investors by low-, medium- and high-DEP applications

Source: Occasional Paper 66, Playing the market: a behavioural data analysis of digital engagement practices and investment outcomes by John Gathergood, Cameron Gilchrist, Mark D. Griffiths, Lucy Hayes, Emily Morris, Stephen O’Neill, Jesal D. Sheth and Neil Stewart, FCA.

What are the benefits for retail investors?

Gamification can reduce psychological barriers to starting to invest and can help some users engage with finance who otherwise might stay out entirely. The intuitive interfaces and low minimum deposit requirements appeal particularly to younger or first-time investors who find traditional brokerage platforms intimidating or inaccessible.

Furthermore, game mechanics can, in principle, be used to support positive financial behaviours. Some apps have begun to pivot these techniques towards education and prudence, for instance by rewarding users for completing educational modules, diversifying their portfolios or holding assets for the long term. Coinbase had ‘Learning Rewards’ , where users could watch short educational videos about different cryptocurrencies, take a quiz to verify understanding and then receive a small amount of that cryptocurrency, ensuring users understood the asset before they held it. If designed responsibly, these ‘nudges’ can help users build financial literacy and better saving habits.

What are the risks of gamifying investing?

While gamification increases engagement, it can also distort decision-making and encourage excessive risk-taking. The psychological mechanisms behind gamification are well understood by app designers. Variable reward schedules, similar to those used in slot machines, create anticipation and encourage repeated checking of portfolios. Social comparison through leaderboards triggers competitive instincts that may override rational risk assessment. Celebratory animations create positive reinforcement for trading activity, regardless of whether the trade was financially sound. The immediate feedback loops (such as flashing lights or push notifications about market movements) can trigger a fear of missing out and impulsive reactions.

Research suggests that these environments can lead investors to trade more frequently and speculatively than they intended. The FCA found that push notifications and points and prize draws increased the number of trades made by 11% and 12%, respectively, and increased the proportion of trades in risky investments by 8% and 6%, respectively. This demonstrates how these apps can blur the line between investing and gambling.

A 2024 study by the Ontario Securities Commission found that features like social feeds and copy trading increased ‘herding’ behaviour. Users were more likely to buy promoted stocks or follow the crowd, often disregarding fundamental analysis or their own risk tolerance. The study highlighted that the pressure to conform to visible ‘winners’ on a leaderboard can push investors towards volatile assets they do not fully understand. In fact, the FCA found that ‘regardless of how returns [were] measured (realised returns, unrealised returns, or large losses), investors enjoyed significantly poorer returns on high-DEP apps when compared to low-DEP apps,’ suggesting that the engagement these features generate may be detrimental rather than beneficial to long-term wealth building.

How are regulators approaching the issue?

Regulators in the UK and globally have expressed growing concern that gamification reframes trading as entertainment rather than a serious financial activity. The European Securities and Markets Authority has warned that gamified ‘digital nudges’ can mislead investors and breach requirements to act in a client’s best interest, while the FCA’s CEO, Nikhil Rathi, has observed that the line ‘between legitimate investment and trading and unregulated entertainment and gambling has become blurred.’

At the same time, academic commentary highlights a regulatory tension. |In an article in the UCL Journal of Law and Jurisprudence, James Isaacs’ analysis of the FCA’s competition mandate notes that the regulator must balance its duty to promote competition and innovation with its responsibility to protect consumers and safeguard financial stability. Although gamified investing apps have increased competition and reduced costs, they may also introduce new systemic risks by encouraging herding behaviour or excessive leverage among retail investors. Similarly, in their report Digital-Savvy Retail Investors, Marie Brière and Apostolos Thomadakis advocate a regulatory approach that helps investors prosper by clearly distinguishing between beneficial forms of engagement and manipulative design. They argue that regulation should encourage companies to deploy digital tools in ways that nudge users towards long-term, goal-based investing rather than high-frequency speculation.

What should retail investors do?

For the individual investor, awareness is the first and most effective line of defence. It is important to critically assess the features of any trading platform you use. For example, consider turning off non-essential push notifications, particularly those highlighting daily ‘movers’ or sharp price swings, as these alerts are often designed provoke an emotional reaction rather than support informed decision-making.

Investors should also be wary of ‘achievement’ features that reward frequent trading. Instead, setting clear, written investment goals and risk limits outside the app environment can help maintain discipline. When making a trade, compare the decision against your personal criteria rather than in-app rewards, rankings or social sentiment. Choosing platforms or settings that emphasise diversification and long-term investing can further reduce the temptation to over-trade.

It is also important to recognise that a platform’s incentives may not align with your own. Trading apps typically generate revenue through mechanisms such as payment for order flow, bid-ask spreads or subscriptions tied to active use. As a result, increased trading activity benefits the platform regardless of whether those trades are profitable for the investor.

Finally, consider complementing app-based trading with access to independent, institutional-grade research that prioritises fundamental analysis over engagement metrics. While gamified platforms excel in accessibility and user experience, traditional research providers offer deeper company analysis, management insights and sector expertise without the psychological prompts designed to increase trading frequency. Combining these approaches can help investors make more informed decisions, while still benefiting from the convenience of modern trading technology.

Edison’s view

The gamification of investing apps represents a double-edged innovation. On the one hand, the technology has genuinely lowered barriers to entry, making investing more accessible to millions who might otherwise have remained on the sidelines. On the other hand, its current implementation often prioritises engagement metrics over investor outcomes, creating an environment in which the interests of platforms and users diverge.

Evidence from behavioural research is clear: many gamification features increase trading frequency and risk taking without improving returns. For retail investors, this means the colourful and engaging interface may be actively working against their long-term financial interests. The solution is not to avoid investing apps altogether, but to use them with a clear understanding of how they are designed to influence behaviour.

As regulatory scrutiny increases, there may be a shift toward more responsible forms of gamification that genuinely supports sound investing habits. Until then, the responsibility largely rests with individual investors to recognise the psychological techniques being deployed and to develop strategies to counteract them. In an era where trading apps may be more sophisticated in behavioural psychology than their users, scepticism toward gamified features is not cynicism but prudence.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping us understand which section of the website you find more interesting and useful. See our Cookie Policy for more information.

Strictly necessary and functional

These cookies are used to deliver our website and content. Strictly necessary cookies relate to our hosting environment, and functional cookies are used to facilitate social logins, social sharing and rich-media content embeds.

Advertising

Advertising Cookies collect information about your browsing habits such as the pages you visit and links you follow. These audience insights are used to make our website more relevant.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Performance

Performance Cookies collect anonymous information designed to help us improve the site and respond to the needs of our audiences. We use this information to make our site faster, more relevant and improve the navigation for all users.

Please enable Strictly Necessary Cookies first so that we can save your preferences!