Company description: Full-service provider for geothermal projects

Founded in 1946 as a water well drilling business, Daldrup & Söhne has evolved into a technology specialist in drilling and a full-service provider for geothermal projects (from feasibility study, exploration claim acquisitions, engineering and construction to power supplies). With more than 40 drilling rigs, the company currently owns the largest drilling capacity in the European onshore industry. Its main markets are Germany, the Netherlands, Switzerland, Benelux and Poland. The company went public in November 2007, and currently employs c 140 people.

Daldrup & Söhne operates in four business segments: Geothermics; Raw Materials & Exploration; Water Procurement; and Environment, Development & Services (EDS). The Geothermics division provides drilling services for near-surface projects (eg geothermal probes of heat pumps) and deep geothermics up to 6,000m. In the Raw Materials & Exploration division, the bores made by Daldrup & Söhne are used for exploring and developing fossil fuel deposits (especially coal and gas), mineral resources and ores (eg copper and gold). The Water Procurement division comprises well construction for the extraction of drinking, service, curative, mineral, boiler-feed or cooling water as well thermal brine. The Environment, Development & Services (EDS) division comprises special environmental engineering services such as the hydraulic clean-up of contaminated sites, the drilling of gas extraction wells for recovering waste dump gas, the provision of groundwater quality measuring points and the installation of water purification plants.

Daldrup & Söhne is vertically integrated in the geothermal business, with end-to-end competence from project development to energy contracting. Undertaking drilling/exploring projects for third parties is currently the bread and butter. In the meantime, the company develops and owns stakes in projects by either (1) acting as the engineering contractor for the projects it has minority stakes in and recognises engineering revenue; or (2) acting as the project owner (with majority stakes) and recognising revenues only after the plants come online and start to sell heat/electricity. Typically, the cost split of a geothermal project throughout its lifecycle is 5-10% for feasibility study, permitting and seismic profiling, 40-50% for drilling, hydraulic tests, circulation tests and thermal water circuit construction, and 30-40% for construction of power plants and heating supplies, contracting for electricity and heat. Currently, Daldrup & Söhne owns 40% of the Landau plant (temporarily shut down) and is constructing the Taufkirchen plant (38.9% ownership).

Except in the lean year of 2015, when sales were at their lowest in the past five years, Geothermics is typically the largest division. Due to the growth of geothermal demand in Germany, management expects Geothermics to remain the major revenue contributor over the next few years. Management indicates that the revenue contribution from the drilling contracts for geothermal power plants is expected to increase from 30% in 2015 to 50% in 2017.

Exhibit 1: Revenue dynamics by division

|

Exhibit 2: Revenue breakdown by division

|

|

|

Source: Daldrup & Söhne data

|

Source: Daldrup & Söhne data

|

Exhibit 3: Vertical integration in geothermal projects

|

|

|

|

Strategy

Daldrup & Söhne Group is expanding its footprint from engineering, procurement and construction (EPC) to offering turnkey services for geothermal projects, with the following strategic initiatives:

■

Leverage of the worldwide licence and the exclusive right to use the Kalina process in Germany. As Germany is lacking in high enthalpy resources at shallow depth, the construction of deep wells and the application of binary power plant technologies (ie Organic Rankine Cycle [ORC]) are necessary to produce electricity at temperatures down to 100°C. The ORC process uses an organic liquid (such as silicone, oils and hydrocarbons) as a medium, instead of water. The Kalina process is a special ORC process that uses a mixture of ammonia and water (for evaporation at low temperatures) in order to improve efficiency. Management believes that the Kalina technology used in the geothermal energy power plant in Husavik, Iceland, as well as on German soil in Unterhaching and Bruchsal, is particularly suitable for generating electricity, especially in the low temperature range. Exorka is a global licensee of the Kalina patent and has the exclusive rights for its use in Germany. So far, two out of 10 geothermal electricity plants (Bruchsal in Baden-Württemberg and Unterhaching near Munich) have been built with the Kalina process. Daldrup & Söhne's geothermal plant in Taufkirchen will be the third plant running on the Kalina technology in Germany.

■

Development of expertise in risk mitigation. The company is a pioneer in the use of the integrated insurance model (also known as ART, alternative risk transfer). As insurance alone is too simple a tool to deal with the complexity of exploration risk (ie the risk of carrying out costly drilling but not finding sufficient thermal energy), alternative risk transfers are created with the structuring of credit derivatives for developers, banks and insurance/reinsurance companies, to better define, manage and hedge risks. Daldrup & Söhne believes that the use of the ART structure can give investors and banks new to geothermal more comfort, as trigger risk events are better defined than in plain vanilla insurance contracts. Daldrup & Söhne has been going through the learning curve of using the ART structure and this helps in the company’s project development and engineering business (eg the €19m contract for two geothermal drillings at the Geretsried site awarded by Enex Geothermieprojekt Geretsried Nord).

■

Increase of exposure to project development and ownership. Through years of R&D, Daldrup & Söhne has and will continue to accumulate know-how and knowledge in exploration. For instance, the Leibniz Institute for Applied Geophysics (LIAG) has placed an order worth around €1m with Daldrup & Söhne as part of the Dolomitkluft research project to explore the high temperature ranges in the various geological layers in the south of Munich. To monetise its wealth of expertise, Daldrup & Söhne has been increasing its exposure to project development and ownership, to capitalise on the favourable feed-in-tariffs under the 2017 German Renewable Energy Sources Act (EEG).

Operating at full capacity through 2018

Following a double-digit million euro contract with Munich-based utility Stadtwerke München, announced on 3 May 2017, Daldrup & Söhne is expecting to operate at full capacity for all its business divisions until the end of 2018, with an order backlog of €65m as of 31 May 2017. As management indicates additional orders are in the pipeline, it is possible that the company may need to hire additional staff.

Based on the company’s well-filled order book, management projects gross revenue of around €40m and an EBIT margin of between 2% and 5% for 2017. This forecast does not include possible revenue and profit contributions from the geothermal power plants in Landau and Taufkirchen, Germany. The guided revenue for 2017 of approximately €40m based on output (defined as sales plus change in work-in-progress) does not include potential revenue from the sale of electricity/heat from these plants.

Exhibit 4: Contracts announcements in 2017

Project |

Contract value, €m |

Announcement |

Client |

Segment |

Stadtwerke München |

Double digit |

May 2017 |

Stadtwerke München |

Geothermics |

Geretsried |

19 |

March 2017 |

Enex Geothermieprojekt Geretsried Nord |

Geothermics |

Bad Bellingen |

3.8 |

March 2017 |

Enex Geothermieprojekt Geretsried Nord |

Geothermics |

Dolomitkluft R&D |

1 |

May 2017 |

Leibniz Institute for Applied Geophysics (LIAG) |

Geothermics |

Source: Daldrup & Söhne data

Geothermal demand in Germany

The highly variable generation profile of wind and solar has been a pressure to the grids and caused negative spot electricity prices during peak hours in Germany. It is hardly surprising that policymakers like the idea of having geothermal energy as a baseload source, available all year round and throughout the day. This is why geothermal energy continues to enjoy fixed feed-in-tariffs while wind and solar tariffs will be determined via auctions under the 2017 German Renewable Energy Sources Act (EEG). The total time horizon required from site identification, plant construction to grid connection is approximately three to four years. The EEG takes account of the longer development times and higher complexity of exploration risks associated with geothermal, and hence the feed-in tariff for electricity generated by geothermal energy is fixed at €0.252/kwh until 2020. A targeted 5% annual reduction will kick in from 2021. The tariff is paid for 20 years in addition to the year in which operation of the plant begins.

Germany is lacking in high enthalpy resources at shallow depth or natural steam reservoirs that can be used for a direct drive of turbines. Therefore, the application of binary power plant technologies (eg Kalina cycle) is necessary to produce electricity at temperatures down to 100°C. The most important geothermal resources in Germany are in the North German Basin, the South German Molasse Basin, and the Upper Rhine Graben. Geothermal projects in Germany are usually developed by municipals and private companies. Stadtwerke München (SWM), a Munich-based utility, has set a goal to make Munich, by 2040, the first city where 100% of district heating will be generated from renewable energy sources, especially geothermal energy.

Geothermal (particularly for electricity) is growing rapidly in Germany from a small base. In 2016, renewable energy covered roughly 29% of the volume of electricity generated in Germany, according to the Federal Ministry for Economic Affairs and Energy (BMWi). However, Geothermal is currently a very small portion of it. In 2016, deep geothermal accounted for 0.1% of total renewable electricity and 0.6% of heat supply from renewable energy sources.

There are 34 geothermal energy plants in operation in Germany, of which 25 produce solely heat, four produce only electricity and five generate both heat and electricity. According to the German Geothermal Association (Bundesverband Geothermie), approximately 30 plants (with an aggregate capacity of 95MW) are under development or under construction.

Exhibit 5: Geothermal power plant in operation in Germany

Plant |

Region |

COD |

Status |

MWtherm |

MWel |

Process |

Asset owner/developer |

Bruchsal |

Upper Rhine Graben |

2010 |

Temporary shut-down |

5.5 |

0.44 |

Kalina |

EnBW |

Dürrnhaar |

Molasse Basin |

2012 |

Operating |

|

5.5 |

ORC |

Stadtwerke München |

Laufzorn |

Molasse Basin |

2014 |

Operating |

40 |

4.3 |

ORC |

|

Insheim |

Upper Rhine Graben |

2012 |

Operating |

|

|

ORC |

BESTEC |

Kirchstockach |

Molasse Basin |

2013 |

Operating |

|

5.5 |

ORC |

Stadtwerke München |

Landau |

Upper Rhine Graben |

2007 |

Temporary shut-down |

7 |

3.6 |

ORC |

40% owned by Geysir |

Sauerlach |

Molasse Basin |

2013 |

Operating |

5 |

6 |

ORC |

Stadtwerke München |

Oberhaching |

Molasse Basin |

2014 |

Operating |

4 |

5 |

ORC |

|

Traunreut |

Molasse Basin |

2016 |

Operating |

12 |

5.5 |

ORC |

Geothermischen Kraftwerksgesellschaft Traunreut |

Unterhaching |

Molasse Basin |

2007 |

Operating |

38 |

3.36 |

Kalina |

Unterhaching municipality |

Source: German Geothermal Association (Bundesverband Geothermie); Think Geoenergy; Leibniz Institute for Applied Geophysics; Edison Investment Research

Management, organisation and corporate governance

Supervisory board and management board

The management board is responsible for the day-to-day operations of the company and dealings with third parties. The supervisory board monitors the performance of the management.

Management board

CEO Josef Daldrup, born in 1953, joined the family business in 1976; Daldrup & Söhne was founded in 1946 by his father Karl Daldrup. Josef Daldrup has a master craftsman's diploma as a well builder and a sanitary expert. He studied at the University of Minden and has also been chairman of the management board since 2001. Since the IPO in November 2007 he is responsible for Strategy, Key Accounts, PR, HR and Law.

Curd Bems (CFO), born in 1977, was appointed CFO in 2013 and is responsible for Controlling, Finance, Investor Relations and Business Development. He is MD of Geysir Europe GmbH in which Daldrup & Söhne has 75.01 % stakes. Before he joined the company, Mr Bems acted in various companies in leading technical and commercial management positions.

Peter Maasewerd (COO), born in 1960, is responsible for the business segments EDS, water procurement, raw materials & exploration as well as the close-to-the-surface geothermal energy projects. He has a master's degree in geology, joined the company in 1988 and was appointed COO in 2002.

Andreas Tönies (COO), born in 1965, is a sophisticated gas and water plumber and a well constructor. He joined Daldrup & Söhne in the 1980s as a project manager. In 2005 he joined the management board and is responsible for logistics & merchandise management, procurement and the business segment, deep geothermal projects.

Supervisory board

Wolfgang Clement joined the supervisory board in 2008 and was appointed Chair in July 2012. He has been prime minister of North Rhine-Westphalia and federal minister of economics and employment of Germany.

Wolfgang Quecke has been a member of the supervisory board since 2001. He served as general manager at various mining operations from 1995-2000, was head of operations for the Rehabilitation of Mining Sites (BDSB) of DSK AG from 2001-05 and a member of the management board for RAG Montan Immobilien GmbH from 2005-08. Since 2009, he has been an independent advisor.

Joachim Rumstadt has been a member of the supervisory board since July 2012. He started his career in 1997 as a corporate attorney with STEAG. Since 2007, he has served as a member of the management board of STEAG GmbH, and since 2009 as chairman of the management board of STEAG GmbH.

Organisation

Daldrup & Söhne operates in four business segments: Geothermics; Raw Materials & Exploration; Water Procurement; and Environment, Development & Services (EDS).

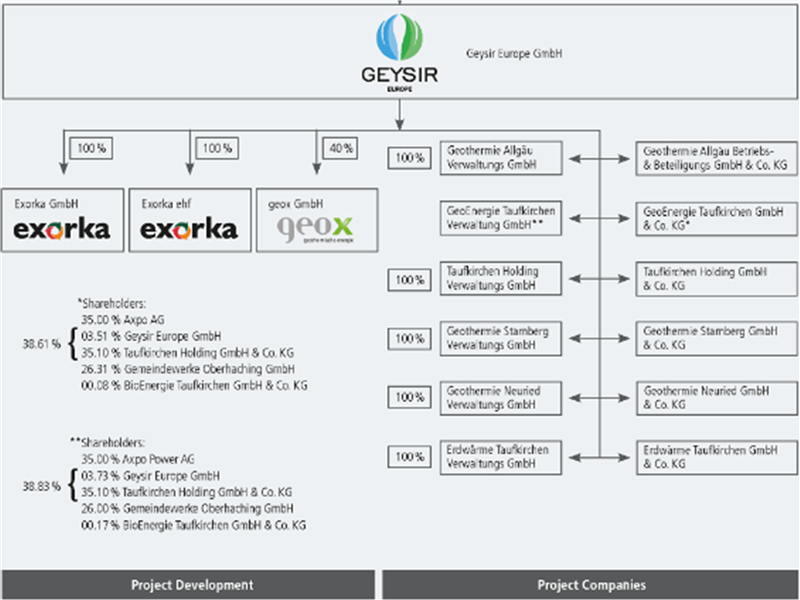

Since the acquisition of a 51% stake in Geysir Europe in 2009, the Geothermics division has been developing its project business under the Exorka brand, particularly in the Molasse Basin and in the Upper Rhine Plain. Currently, Daldrup & Söhne owns 75% of Geysir. Curd Bems, CFO of Daldrup & Söhne, owns 22.9% of Geysir. All the project companies are incorporated under Geysir.

Daldrup & Söhne is currently building the Taufkirchen plant. As this plant is not consolidated in the company’s financials, the engineering revenue is expected to be recognized in 2017 or 2018. The two plants consolidated in Daldrup & Söhne’s financials are the Laudau plant (40% stakes) and the Neuried plant. Neuried will start construction in 2017/18.

Taufkirchen geothermal power plant (38.9% owned by Daldrup & Söhne)

The installed capacity of the geothermal cogeneration plant will total approximately 35MW for thermal energy and about 4.3MW for electricity. In the Taufkirchen power plant project, the thermal water well system was successfully created in 2012 with a thermal capacity of approximately 38MW. Since the end of 2015, heat directed from the new cogeneration plant has been fed into the district heating networks of the customers in Taufkirchen and Oberhaching. New heat exchange will be installed by Daldrup & Söhne within the next few months.

Landau power plant (40% owned by Daldrup & Söhne)

The Landau plant is temporarily closed and valued at €1 in Daldrup & Söhne’s financial assets as of the end of 2016. The permit to resume operations was granted at the end of July 2016, pending the approval for the special operating plan.

The power plant, with a capacity of up to 3.6MW for electricity and up to 7MW for thermal energy, was in operation since 2007 and supplied electricity to EnergieSüdwest’s customers. In August 2013, Daldrup & Söhne acquired 40% of the shares in the geox GmbH (Landau/Pfalz) power plant company from EnergieSüdwest AG via Geysir Europe. The parties also agreed on an option for Geysir Europe to purchase an additional 10%. On 2 January 2014 Daldrup & Söhne agreed to acquire an additional 50% from Pfalzwerke AG, through Geysir Europe. However, Geysir Europe GmbH did not increase its stakes by 50% to 90% because the share purchase agreement with Pfalzwerke AG was rescinded on 2 December 2013, as if the contract had never existed. A court case is pending. After a leakage in 2014, the cause of which clearly predates the acquisition of shares and the takeover of operational management by Daldrup & Söhne, geox shut the power plant down as a precaution to avoid damage to the environment. In 2015, the power plant was upgraded to meet the regulatory requirements for safety.

Neuried (100% owned by Daldrup & Söhne)

In March 2017, the city of Kehl lost the case against the state of Baden-Württemberg regarding the approval of the main operating plan for four geothermal drillings. As the lawsuit has been cleared, management intends to start construction of the plant in either 2017 or 2018. The state of Baden-Württemberg has agreed a grant totaling €1m as a default guarantee for the first deep well.

Exhibit 6: Structure of geothermal project business

|

|

|

|

Shareholders and free float

The Daldrup family owns 65.21% of the company. At the time of the IPO in November 2007, a 10-year pooling agreement was established for the family owners that no single family owner can sell shares unless approved by all the other members. After the expiration of the original pooling agreement in September 2017, it is automatically renewed on an annual basis. There is no succession plan as yet.

Shareholders |

Title/comment |

Holdings |

Josef Daldrup |

Founder, CEO/Chairman |

5.69% |

Karl Daldrup |

Son/employee |

17.80% |

Bernd Daldrup |

Son/employee |

17.98% |

Thomas Daldrup |

Son/employee |

18.02% |

Michaela Daldrup |

Daughter |

5.73% |

TOTAL Daldrup holdings |

|

65.21% |

Free float |

|

34.79% |

Source: Daldrup & Söhne data

Based on the company’s well-filled order book, management guides gross revenue of around €40m and an EBIT margin of between 2% and 5% for 2017. This forecast does not include possible revenue and profit contributions from the geothermal power plants in Landau and Taufkirchen, Germany, for the selling of heat and electricity.

Exhibit 8: Financial summary

Year end 31 December |

€000s |

2012 |

2013 |

2014 |

2015 |

2016 |

Income statement (pursuant to the German Commercial Code (HGB) |

Sales |

|

|

22,690 |

60,826 |

52,327 |

17,255 |

31,137 |

Gross revenue |

45,395 |

59,888 |

44,010 |

26,398 |

39,458 |

EBITDA |

6,089 |

5,189 |

(6,344) |

4,520 |

4,557 |

EBIT |

2,254 |

1,155 |

(18,404) |

806 |

951 |

Profit Before Tax (as reported) |

1,812 |

131 |

(18,781) |

48 |

(228) |

Net income (as reported) |

|

1,164 |

89 |

(18,944) |

175 |

152 |

EPS (as reported) – (€) |

|

0.21 |

0.016 |

(3.45) |

0.03 |

0.03 |

Dividend per share (€) |

|

0 |

0 |

0.11 |

0 |

0 |

|

|

|

|

|

|

|

Balance sheet |

|

|

|

|

|

|

Intangible fixed assets |

|

3,875 |

3,320 |

2,657 |

2,016 |

1,347 |

Property, plant and equipment |

|

41,367 |

39,975 |

28,896 |

25,519 |

24,580 |

Fixed financial assets |

|

22,988 |

22,375 |

24,371 |

22,733 |

23,387 |

Inventory |

|

4,447 |

1,218 |

2,149 |

12,542 |

17,001 |

Receivables and other assets |

|

22,706 |

25,422 |

16,243 |

21,589 |

24,107 |

Liquid funds |

|

5,863 |

3,567 |

4,520 |

3,165 |

755 |

Other assets |

|

205 |

1,800 |

178 |

308 |

206 |

Total assets |

|

101,451 |

97,687 |

79,016 |

88,872 |

91,384 |

Provision |

|

3,594 |

2,472 |

3,756 |

3,121 |

3,180 |

Liabilities to banks |

|

8,049 |

7,163 |

9,436 |

11,917 |

8.618 |

Trade payables |

|

11,404 |

9,183 |

4,964 |

4,211 |

7,888 |

Other liabilities |

|

12,281 |

12,871 |

14,461 |

23,160 |

25,641 |

Total liabilities |

|

|

35,328 |

31,729 |

32,617 |

42,409 |

45,327 |

Net Assets |

|

|

66,123 |

65,958 |

46,399 |

46,463 |

46,057 |

Shareholder equity |

|

66,123 |

65,958 |

46,399 |

46,463 |

46,057 |

|

|

|

|

|

|

|

Cash flow statement |

|

|

|

|

|

|

Net cash from operating activities |

|

14,351 |

733 |

3,484 |

(17,233) |

3,654 |

Net cash from investing activities |

|

(1,418) |

(1,888) |

(4,188) |

4,111 |

(1,130) |

Net Cash from financing activities |

|

3,682 |

(886) |

2,272 |

11,983 |

(2,304) |

Net cash flow |

|

16,615 |

(2,044) |

1,568 |

(1,139) |

220 |

Cash & cash equivalent end of year |

|

5,863 |

3,567 |

4,520 |

3,165 |

755 |

Source: Daldrup & Söhne accounts

Income statement

Daldrup & Söhne reports both sales and gross revenue (defined as sales recognised plus change in work-in-progress) to better match the cash flow profile of the engineering business, as contracts typically last two years. Hence, the change in work-in-progress is usually a good indicator of its revenue trend in the subsequent year. The calculation of profitability is based on gross revenue, although the segment breakdown is still based on reported revenue. While the inclusion of the change in work-in-progress helps to smoothen out the timing difference between revenue recognition and cash flows, all the costs and expenses are still recognised when they are incurred according to the German GAAP. This means likely understated profitability at good times and overstated profitability at subsequently bad times. Daldrup & Söhne’s top line and bottom line are still reflective of the lumpy nature of engineering order backlogs. The normalised depreciation and amortisation in the past five years is slightly below €4m, regardless of the revenue level. Excluding the year 2014 with significant one-offs (eg 50% depreciation for the Mauerstetten well of €7.4m), the normalised EBIT margin (based on gross revenue) in 2012-13 and 2015-16 was in the range of 2.4-3.8%.

Exhibit 9: Sales and change in work-in-progress

|

Exhibit 10: Reported EBIT

|

|

|

Source: Daldrup & Söhne data

|

Source: Daldrup & Söhne data

|

Exhibit 9: Sales and change in work-in-progress

|

|

Source: Daldrup & Söhne data

|

Exhibit 10: Reported EBIT

|

|

Source: Daldrup & Söhne data

|

Balance sheet and cash flow

There are two significant elements in Daldrup & Söhne’s fixed assets: property, plant and equipment for its engineering/contracting activities; and financial assets, predominately comprised of geothermal projects. The intangible assets represent the value of the Kalina licence and the permits for the exploration of geothermal energy (claims). The long-term financial assets are predominately shares in project companies, including 38.59% in GeoEnergie Taufkirchen GmbH & Co. KG and a 40% stake in geox GmbH. The Landau geothermal power plant is valued at €1 in the balance sheet.

Exhibit 11: Leverage and interest cover analysis

€k |

2012 |

2013 |

2014 |

2015 |

2016 |

Gross cash |

5,863 |

3,567 |

4,520 |

3,165 |

755 |

Liabilities to banks |

8,049 |

7,163 |

9,436 |

11,917 |

8,618 |

Net debt |

2,186 |

3,596 |

4,916 |

8,752 |

7,863 |

Equity |

66,123 |

65,958 |

45,463 |

46,463 |

46,058 |

Net debt to equity |

3% |

5% |

11% |

19% |

17% |

EBIT |

2,254 |

1,155 |

(18,404) |

806 |

951 |

EBITDA |

6,089 |

5,189 |

(6,344) |

4,520 |

4,557 |

Interest expense |

779 |

760 |

426 |

1,072 |

1,354 |

Coverage ratio (EBIT) |

2.9x |

1.5x |

(43.2x) |

0.8x |

0.7x |

Coverage ratio (EBITDA) |

7.8x |

6.8x |

(14.9x) |

4.2x |

3.4x |

Source: Daldrup & Söhne data; Edison Investment Research

Exhibit 12: Increase of short-term bank loans

|

Exhibit 13: Rising % of short-term bank loans

|

|

|

Source: Daldrup & Söhne data

|

Source: Daldrup & Söhne data

|

Exhibit 12: Increase of short-term bank loans

|

|

Source: Daldrup & Söhne data

|

Exhibit 13: Rising % of short-term bank loans

|

|

Source: Daldrup & Söhne data

|

The company’s net debt position increased from €2.2m in 2012 to €7.9m in 2016, with the net debt to equity ratio up from 3% to 17% during the period. This in part can be attributed to the write-offs at €8m and one-off expenses totalling €12m in 2014. It is worth noting that the short-term portion of bank loans has increased since 2012, both in value terms and as a share of gross debt, although it was still under control in 2016. Based on the interest expense of €1.35m in 2016 and the guidance of FY17 gross revenue at €40m, the company needs to achieve an EBIT margin towards the high end of the guided range of 2-5% (vs 2% in FY16) or generate revenues from the power plants in Landau and Taufkirchen, in order to cover the interest expenses.

Exhibit 14: Accounting treatment of project development business

|

Majority ownership |

Minority ownership |

Revenue/COGS |

100% revenue from sale of heat/electricity and/or projects |

EPC services |

Equity investment income |

(not applicable) |

% net income from FiT and project sale |

Assets |

Financial assets |

Equity investments |

Liabilities |

75-80% debt financing required |

No liability associated with project loans |

Cash flows from operating activities |

FiT income and project operations/maintenance |

Revenue, costs and expenses |

Cash flows from investing activities |

Claim/site acquisitions |

Equity investment in project companies |

Cash flows from financing activities |

Loan repayments and interests |

Working capital finance with bank loans |

Source: Edison Investment Research

The accounting treatment for consolidated plants and co-developed projects to the income statement and the balance sheet is summarised above. Management has not disclosed the hurdle rate for its independent power producer (IPP) business, but hopes that the predictable revenue streams from the selling of heat/electricity can smoothen out the historically volatile pattern of the engineering revenues.

Daldrup & Söhne is currently valued at 275x P/E, 11.5x EV/EBITDA and 55x EV/EBIT based on 2016 results. In terms of the P/E and EV/EBITDA multiples, Daldrup & Söhne looks expensive compared to its drilling and engineering peers, possibly due to its relative smaller size (hence a lack of opex leverage) and increasing interest burden as the company is expanding its geothermal project development business. For now, the onshore/offshore drilling companies look like more appropriate peers, although this may change over the long term if project assets become a more significant part of Daldrup & Söhne’s income statement and balance sheet.

The closest competitors to Daldrup & Söhne in similar regions are BAUER, KCA Deutag and ITAG. It is worth nothing that Daldrup & Söhne only undertakes onshore projects and the majority of its competitors are also active offshore. As offshore drilling capabilities serve the oil and gas industry, the economic drivers and regulatory environments are rather different from the geothermal sector. In addition, Daldrup & Söhne is only involved in onshore drilling projects. Large onshore/offshore drilling/engineering companies may not be the most suitable peers for the valuation of Daldrup & Söhne in the long run, although it competes with these companies for onshore drilling contracts.

Exhibit 15: Peer group comparison – onshore/offshore drilling

|

Market cap |

P/E (x) |

EV/EBITDA (x) |

EV/EBIT (x) |

|

(m) |

2017e |

2018e |

2017e |

2018e |

2017e |

2018e |

Lamprell PLC |

£390m |

N/A |

77.4 |

8.8 |

6.6 |

132.7 |

24.7 |

Seadrill Ltd |

€200m |

N/A |

N/A |

9.5 |

14.4 |

54.0 |

N/A |

Odfjell Drilling |

€422m |

13.7 |

18.0 |

6.3 |

6.5 |

18.1 |

19.2 |

Songa Offshore |

€443m |

45.8 |

40.6 |

6.3 |

5.6 |

11.8 |

11.0 |

BAUER |

€363m |

15.1 |

12.1 |

6.6 |

6.2 |

14.2 |

12.2 |

Peer group average |

24.9 |

34.5 |

7.4 |

7.9 |

46.2 |

16.8 |

Source: Bloomberg. Note: prices as at 13 June 2017.

A more appropriate group of peers for Daldrup & Söhne in the long run is perhaps renewable EPC/developers with their main operations in Germany and the rest of the Europe, given the similarities to their exposure to regulatory risks. Most such companies are focused on wind and solar, and have gone through a few cycles as a result of demand/supply dynamics and regulatory changes (from fixed feed-in tariffs to auction-based pricing). As a result of increasing supply, both solar and wind have seen significant cost reductions over the past decade and have therefore reached grid parity in different geographies. This means the levelized cost of electricity (LCOE, the cost of generation during the life of operating assets) is lower than or equal to the price of purchasing power from the electricity grid (from the perspective of utilities or consumers).

Exhibit 16: Publicly listed renewable companies in Europe

Company |

Ticker |

Renewables |

Assets |

7C Solarparken |

FWB: HRPK |

Solar |

Over 95% of the assets in Germany, predominantly in Bavaria and Saxony |

Energiekontor |

EKT: Xetra |

Wind, solar |

Wind and solar projects in Germany, Portugal and the UK |

Phoenix Solar |

PS4:Xetra |

Solar |

Solar project EPC |

EDP Renováveis |

Data |

Wind |

Wind projects in Europe (mainly Iberia) and North America |

Good Energy |

GOOD:LN |

Wind, solar |

Solar/wind projects and electricity distribution |

Source: Edison Investment Research

Compared to solar and wind, geothermal power in Germany is still at an early stage of development. The recent revival of interest from investors is mainly a result of the regulatory support (ie the visibility of fixed feed-in tariffs if projects come online before 2020 and 5% annual reductions thereafter). On the positive side, the geothermal sector is less susceptible to the pressure of oversupply (as in the case of solar and wind) and pricing pressure, because of a much more complex and elongated process in permitting, exploration and engineering. On the negative side, investors are less likely to see exponential growth in a short period of time for geothermal companies.

Exhibit 17: Peer group comparison – renewable companies

|

Market cap |

P/E (x) |

EV/EBITDA (x) |

EV/EBIT |

|

(m) |

2017e |

2018e |

2017e |

2018e |

2017e |

2018e |

7C Solarparken |

€111 |

23.3 |

20.1 |

9.8 |

9.4 |

24.3 |

23.0 |

Energiekontor |

€259 |

14.1 |

13.7 |

6.1 |

5.6 |

8.3 |

7.8 |

Phoenix Solar |

€20 |

N/A |

26.5 |

7.9 |

6.8 |

12.5 |

10.1 |

EDP Renováveis |

€6,117 |

33.2 |

29.2 |

8.4 |

7.9 |

14.5 |

14.1 |

Good Energy |

£36 |

21.6 |

16.4 |

8.5 |

7.5 |

14.7 |

13.2 |

Peer group average |

23.0 |

21.2 |

8.1 |

7.1 |

14.9 |

13.6 |

Source: Bloomberg. Note: Prices as at 13 June 2017.

Daldrup & Söhne’s business activities are subject to the following risk factors:

■

Subsoil issues: This refers to the risk of known and unforeseeable effects and difficulties originating from the subsoil (all underground, geological risks). This is generally within the sphere of responsibility of the client. Daldrup & Söhne as the contractor bears the risk for technical drilling operations. In the deep drilling carried out by Daldrup, this risk can generally be absorbed by project-related machinery breakdown and so-called lost-in-hole-insurance.

■

Technological issues: Daldrup & Söhne is a licensee of the Kalina process and believes that this technology is ideal for countries like Germany lacking in high enthalpy resources. As Exorka, a subsidiary of Daldrup& Söhne has the exclusive right to use the Kalina process in Germany, its competitors may push the alternative binary process, OCR.

■

Competitive issues: Competitors in the area of deep geothermal wells include drilling companies that are primarily engaged in the oil and gas business and occasionally participate in invitations to tender for geothermal projects. When crude oil prices are low, the competition is greater because there is an additional supply of drilling capacity.

Geothermal, like all renewable energy sources, is subject to the regulatory and macroeconomic risks. However, the technical complexity of the exploration process and the long-time horizon of geothermal project development come with additional risks. Daldrup & Söhne assumes the following risks for its project development business:

■

Regulatory issues: As Germany is lacking in high enthalpy resources at shallow depth, geothermal projects (particularly with electricity generation) require the support of feed-in tariffs. The 2017 German Renewable Energy Sources Act (EEG) offers fixed feed-in tariffs of €0.252/kwh to geothermal until 2020. A targeted 5% annual degression will kick in from 2021.

■

Project development issues: Similar to other large renewables such as solar and wind, only a small percentage of project pipelines will eventually come into fruition. In the case of geothermal projects, the permitting process alone is highly complicated. Developers have to obtain both exploration claims (for the right to investigate sites) and mining claims (for the right to extract the natural resources). In Bavaria’s Molasse basin alone, 140 exploration claims were granted, but only 21 projects have been implemented. Many licences were cancelled because of failure to launch any exploration activities within three years of the licence date.

■

Exploration issues: Geothermal as a renewable source had a false start about 10 years ago because investors and banks active in the renewable market were inexperienced in exploration risks, ie the risk of carrying out costly drilling but not finding sufficient thermal energy to achieve the originally intended economic value. This is one of the main reasons why relatively few geothermal energy projects have been completed in Germany to date.

■

Macroeconomic issues: Geothermal projects are typically 20-30% funded with equity and 70-80% with debt. A low interest environment is conducive to renewable project finance as investors and bankers seek higher yields supported by feed-in tariffs.

■

Legal issues: Law suits are not uncommon in the case of public opposition to extractions or contention regarding the accountability of technical faults. Partnerships with local heating networks or a bulk purchaser, such as public or municipal utilities or large industrial consumers, can sometimes help to address concerns from local communities.

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 295 Madison Avenue, 18th Floor 10017, New York US |

Sydney +61 (0)2 8249 8342 Level 12, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Edison, the investment intelligence firm, is the future of investor interaction with corporates. Our team of over 100 analysts and investment professionals work with leading companies, fund managers and investment banks worldwide to support their capital markets activity. We provide services to more than 400 retained corporate and investor clients from our offices in London, New York, Frankfurt and Sydney. Edison is authorised and regulated by the Financial Conduct Authority. Edison Investment Research (NZ) Limited (Edison NZ) is the New Zealand subsidiary of Edison. Edison NZ is registered on the New Zealand Financial Service Providers Register (FSP number 247505) and is registered to provide wholesale and/or generic financial adviser services only. Edison Investment Research Inc (Edison US) is the US subsidiary of Edison and is regulated by the Securities and Exchange Commission. Edison Investment Research Limited (Edison Aus) [46085869] is the Australian subsidiary of Edison and is not regulated by the Australian Securities and Investment Commission. Edison Germany is a branch entity of Edison Investment Research Limited [4794244]. www.edisongroup.com DISCLAIMER

Any Information, data, analysis and opinions contained in this report do not constitute investment advice by Deutsche Börse AG or the Frankfurter Wertpapierbörse. Any investment decision should be solely based on a securities offering document or another document containing all information required to make such an investment decision, including risk factors. Copyright 2017 Edison Investment Research Limited. All rights reserved. This report has been commissioned by Deutsche Börse AG and prepared and issued by Edison for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Opinions contained in this report represent those of the research department of Edison at the time of publication. The securities described in the Investment Research may not be eligible for sale in all jurisdictions or to certain categories of investors. This research is issued in Australia by Edison Aus and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securities and Exchange Commission. Edison US relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. As such, Edison does not offer or provide personalised advice. We publish information about companies in which we believe our readers may be interested and this information reflects our sincere opinions. The information that we provide or that is derived from our website is not intended to be, and should not be construed in any manner whatsoever as, personalised advice. Also, our website and the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. This document is provided for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Edison has a restrictive policy relating to personal dealing. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report. Edison or its affiliates may perform services or solicit business from any of the companies mentioned in this report. The value of securities mentioned in this report can fall as well as rise and are subject to large and sudden swings. In addition it may be difficult or not possible to buy, sell or obtain accurate information about the value of securities mentioned in this report. Past performance is not necessarily a guide to future performance. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (ie without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision. To the maximum extent permitted by law, Edison, its affiliates and contractors, and their respective directors, officers and employees will not be liable for any loss or damage arising as a result of reliance being placed on any of the information contained in this report and do not guarantee the returns on investments in the products discussed in this publication. FTSE International Limited (“FTSE”) © FTSE 2017. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. |

|