Company description: Digital IR solutions

EQS Group is one of the largest global providers of digital solutions for investor relations and for broader categories of corporate communications. These are products designed to automate and simplify the work processes for IR professionals, enabling them to meet all regulatory requirements and freeing up their time to deal with the messaging of their company’s equity story and strategy rather than on information processing. By ensuring that the product suites provided are constantly updated for the latest regulatory compliance changes and are delivered via intuitive interfaces, EQS should continue to add value for its users.

The group was founded in 2000 in Munich, initially building a strong market position in its home markets of Germany, Switzerland and Austria before starting to build out its presence in overseas territories. EQS looks to position itself as a partner with its client companies, working alongside them to solve issues and reduce inefficiencies, rather than simply as a supplier whose interest may not extend beyond the initial sales timeframe, with a growing emphasis on providing software-as-a-service (SaaS). The shift away from paper-based information to digital channels of communication between corporate entities and their various stakeholders is a key driver for growth and is a trend unlikely to be reversed.

EQS has expanded both organically and by acquisition and now employs around 300 people (including those brought into the group with the consolidation of ARIVA), of whom the largest number, 100, are involved in web, back-end, platform and software development. Its headquarters are in Munich, Germany, with further German offices in Hamburg and Kiel and offices in Switzerland (Zurich), Russia (Moscow), the US (New York), Dubai and France (Paris). In December 2015, the group purchased Obsidian IR in the UK (price undisclosed), which gave a strong foothold in that market on which to build. In the Far East, the group has operations in Singapore, Hong Kong, China (Shenzhen and Shanghai) and Taiwan (Taipei). This global network enables EQS to offer the global solutions sought by some of the largest multinationals.

The group’s technical operations are based in Munich, Germany, and Kochi in India. EQS’s solutions and services enable over 8,000 companies worldwide (up from 7,000 this time last year) to fulfil complex domestic and international corporate information requirements securely, efficiently and on a timely basis. Its increased stake in ARIVA (from a 25.44%-owned associate to 67% and consolidated) has added capabilities in the production of documents for packaged retail investment and insurance-based products (PRIIPs), further broadening the target markets to encompass the financial institutions.

Exhibit 1: FY16 Revenues by segment

|

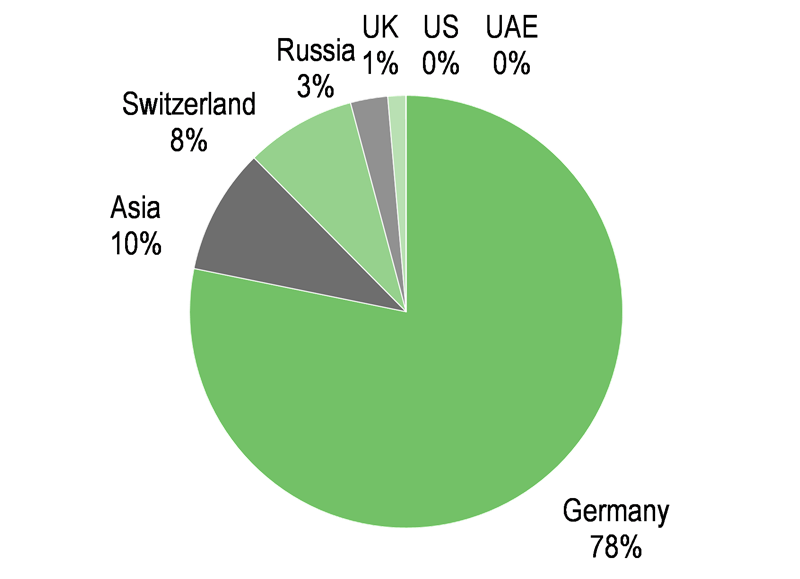

Exhibit 2: FY16 Revenues by geography

|

|

|

Source: Edison Investment Research

|

Source: Edison Investment Research

|

Exhibit 1: FY16 Revenues by segment

|

|

Source: Edison Investment Research

|

Exhibit 2: FY16 Revenues by geography

|

|

Source: Edison Investment Research

|

Strategy

The group’s strategy is based around the three strands – digitisation, regulation and globalisation – and their impact on corporate compliance and investor communication. By simplifying, organising and automating the tasks that need to be fulfilled by IR professionals, their time is freed up to concentrate on face-to-face communication and more value-adding tasks. It also should reduce the risk of financial penalties or other sanctions from non-compliance with regulation.

The earlier growth strategy was predicated on increasing the range of products and services and rolling them out across different territories. To a large extent, the core of the growth strategy remains unchanged, but the increase in the scale of the operations has meant that management is able to lift its gaze and look at the more fundamental drivers of the next few years of growth opportunities. These fall into the three factors identified above.

Digitisation. As the business of corporate communications has become more complex, with different stakeholders with often very different requirements in terms of style and content, the attractions of digitising and automating as much of the process as possible are becoming ever more apparent. The tools that EQS has built to service this market have been designed to relieve the IR or communications teams of as many of the routine elements as possible, with the COCKPIT product allowing the client control over what is integrated. Driving the SaaS sales should protect it from avoidable client churn and improve the quality of the group’s earnings, as well as delivering a higher margin than one-off sales with a high element of customisation.

Regulation in financial markets changes regularly. There is some deregulation, such as the reduced requirements for publicising changes in voting rights in Germany, but considerably more in the way of tightening and extension of existing regulation, as well as the imposition of new requirements on corporate entities. With the rise of the larger asset managers, cash is increasingly seeking out investment opportunities globally and there is a correlated increase in expectation that some form of investor protection will be in place. The impact of changes in regulation can be a major factor. Well flagged, the reduction in the requirement to issue quarterly notifications in some circumstances following the introduction of the EU Transparency Directive had a marked impact on EQS in H116, with 46% fewer such announcements in H116 when compared to H115. There was, however, an increase in voluntary communications, which partially offset the decline of news volumes released through the COCKPIT. H216 benefited from the introduction of the EU’s Market Abuse Regulations, which came into force in July 2016. This extended the obligations to unlisted securities, opening up a new potential market area for EQS, one where those responsible will have less working knowledge of the day-to-day requirements imposed. Even for experienced IR professionals, the responsibilities are onerous and the risks of not complying with the requirements are heavy in terms of both finance and individual careers. This is helping to drive sales of contracts for the INSIDER MANAGER product, growing the group’s SaaS revenues.

Internationalisation. Being the market leader in its home markets, the potential for growth was self-evidently restricted. The steps into other markets, primarily through acquisition, have been taken carefully over the last few years, with the aim of building a global network of businesses that serve clients within their domestic markets and those larger, and/or global, concerns that want to have consistency between the markets in which they operate. EQS needs both global capability and local expertise. This requires local offices and local knowledge, which obviously has cost implications. However, by centralising the technical development and support functions, these capabilities can be leveraged across the network.

The growth strategy is also now predicated on increasing the amount of up- and cross-selling of products and services, increasing the average revenue per client and bolstering achievable margin.

Recent newsflow and upcoming catalysts

FY16 figures were released in early April 2017. The AGM is scheduled for 17 May, at which point the market will be updated for Q117. The interim results will be presented to the market on 14 August, with the Q3 statement on 15 November.

There are two impending pieces of financial market regulation that will directly affect EQS’s client base and the way that they conduct their investor relations processes. These are:

■

the PRIIP (packaged retail investment and insurance-based investment products) regulation, which will be mandatory across the EU, which is due to take effect at the beginning of 2018, extending this requirement to retail investment companies and insurance-based products – approximately 8,000 companies across Europe. The production of these leaflets is already mandatory for non-retail banks. ARIVA (67%-owned) has developed and launched a new turnkey software solution, which enables issuers in the financial sector to automatically generate documents for packaged retail investment and insurance-based products (PRIIPs), significantly reducing the administrative burden (currently either banks have developed their own software or generate these reports in a fairly manual way). ARIVA joined the group with a high-profile reference client for the software and management plans. It is leveraging EQS’s existing relationships with the financial industry to accelerate the rollout of this product, which has the potential to become a significant new product line.

■

MiFID II, also scheduled to take effect from early 2018. Although this does not have the same direct implications for clients as the PRIIP regulations will, the move towards more rigorous standards in corporate communications with investors fits well with the other elements of EQS’s client offering.

The opportunity that EQS has to build its business ultimately depends on the health of financial markets around the world, documented through the number of listed companies across the global markets in which it operates. This is obviously a function of new listings, offset by de-listings, which have been a feature of the more mature markets. A company going through the IPO process is potentially the most remunerative client for EQS, as it may well be putting in place investor communication for the first time, therefore offering several possible income stream opportunities.

All companies operating in regulated equity and/ or debt markets will have requirements to communicate effectively with their stakeholders on a clear and consistent basis, with potentially onerous penalties for non-compliance.

EQS is the leading supplier in its field in its home markets of Germany and Switzerland, as well as in Russia, where it has been established for some time. It has early-mover advantage in faster-developing Asian markets.

In the more mature Anglo-Saxon markets, competition from established providers is more intense. By integrating its market offering to cover off all the required elements of investment relations, with the requisite understanding of local – as well as international – compliance, EQS should be in a position to offer an end-to-end solution for clients that operate in multiple territories.

Management, organisation and corporate governance

Supervisory board and management board

There are three members of the supervisory board and two members of the executive board. The role of the supervisory board is to oversee the executive board in the leadership of the company.

Management steeped in financial markets and IR

The group’s CEO is Achim Weick, who began his career at Commerzbank. Subsequently, he was co-founder of investor relations manager CMC Capital Markets Consulting. Achim is the originator, founder and largest shareholder of EQS and has been on the board since its foundation. COO Christian Pfleger joined EQS in 2001, initially as a client relationship manager, moving on to project management from 2003. In 2007, he took over responsibility for Products and Services. André Silverio Marques, who fulfils the finance function, previously ran the group’s Russian businesses. Before that, he was in charge of the IR, business development and corporate finance activities. Marcus Sultzer, CEO Asia-Pacific, is also a key team member. He joined the group in 2007 and was in charge of business development in Russia and the CIS from 2009.

Shareholders and free float

CEO Achim Weick is the largest shareholder, with 23% of the equity. Supervisory board members hold 8%, with the other executive board member holding 2%. 22% of the shares are held by Investmentaktiengesellschaft für langfristige Investoren TGV, a long-term, institutional investment fund. The free float is 45%.

Exhibit 3: Shareholders and free float

|

|

Source: EQS Group accounts. Note: SB = supervisory board, EB = executive board

|

Income statement

EQS is still in the investment phase of its corporate development, seeking to build meaningful positions in its key target geographic and product/service markets. The top line grew by 12.5% compound in 2009-15, with the larger uplift in 2016 reflecting the consolidation of ARIVA and the acquisition of the Swiss company Tensid during the year. German revenues increased by 38% (6% stripping out ARIVA) for FY16 vs FY15. Non-domestic revenues, though, grew 57%. Overall organic growth for the year was 4%.

A key emphasis is on building recurring and repeatable revenue streams (see Exhibit 6, below). The cloud-based revenues (up 29% FY16 over FY15) are in news, compliance and workflow functions, and, once set up (and once fixed infrastructure costs are recovered), should generate comparatively strong operating margins. Licensing revenues (+20% y-o-y) principally relate to filing, webcast and hosting. In FY16, the proportion of recurring revenues decreased to 68% (78%), due to the consolidation of ARIVA, which generates mostly project and media revenues. Although project revenues relate to discrete bits of business, some, such as preparation of report and accounts, can repeat on an annual basis.

The investment in corporate expansion, both in terms of product development and physical infrastructure, has put continued pressure on EBITDA margins, but is a prerequisite to building a sustainable, long-term business model. Consensus forecasts are assuming that there will be further contraction of EBITDA margin in the current year from 16.0% in FY16 to 14.9% in FY17, before starting to build in the following year as earlier expenditure starts to be leveraged, with a suggested level of 16.7%.

Company guidance for FY17 is for sales growth of 20-25% to €31.2-32.5m, with non-IRFS EBIT expected to increase by 10-20% to a range of €3.6-3.9m. The medium-term top-line guidance is for 10-15% average growth for the next five years.

Exhibit 4: Financial summary

€000s |

2012 |

2013 |

2014 |

2015 |

2016 |

Year end 31 December |

|

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

Income statement |

|

|

|

|

|

|

Revenue |

|

|

14,220 |

15,829 |

16,390 |

18,377 |

26,061 |

EBITDA |

3,609 |

3,572 |

3,660 |

3,485 |

4,175 |

Profit before tax (as reported) |

3,432 |

3,278 |

2,945 |

2,471 |

1,774 |

|

|

|

|

|

|

|

|

EPS (as reported) – (€) |

|

|

N/A |

1.83 |

1.57 |

1.20 |

0.96 |

Dividend per share (€) |

|

0.00 |

0.75 |

0.75 |

0.75 |

0.75 |

|

|

|

|

|

|

|

|

Balance sheet |

|

|

|

|

|

|

Total non-current assets |

|

10,413 |

13,658 |

19,383 |

22,777 |

30,389 |

Total current assets |

|

5,526 |

6,055 |

4,750 |

6,972 |

12,014 |

Total assets |

|

15,939 |

19,613 |

24,133 |

29,749 |

42,403 |

Total current liabilities |

|

(1,994) |

(3,274) |

(4,380) |

(5,325) |

(9,942) |

Total non-current liabilities |

|

(96) |

(1,070) |

(3,882) |

(7,276) |

(7,237) |

Total liabilities |

|

|

(2,090) |

(4,344) |

(8,262) |

(12,601) |

(17,179) |

Net Assets |

|

|

13,849 |

15,369 |

15,870 |

17,148 |

25,224 |

|

|

|

|

|

|

|

|

Shareholder equity |

|

13,849 |

15,369 |

15,833 |

17,148 |

22,255 |

|

|

|

|

|

|

|

Cash flow |

|

|

|

|

|

|

Net cash from operating activities |

|

2,025 |

2,476 |

2,844 |

3,618 |

3,473 |

Net cash from investing activities |

|

(587) |

(3,290) |

(4,710) |

(3,024) |

(2,944) |

Net cash from financing activities |

|

(731) |

1,046 |

533 |

2,066 |

5,279 |

Net cash flow |

|

707 |

232 |

(1,333) |

2,660 |

5,808 |

Cash & cash equivalent end of year |

|

2,748 |

2,980 |

1,370 |

3,607 |

6,610 |

Source: EQS Group accounts. Note: Reported numbers are stated before amortisation of acquired customer base, purchase price allocation and acquisition expenses.

Exhibit 5: Revenue and EBITDA

|

Exhibit 6: FY16 revenue by type

|

|

|

Source: EQS Group accounts

|

Source: EQS Group accounts

|

Exhibit 5: Revenue and EBITDA

|

|

Source: EQS Group accounts

|

Exhibit 6: FY16 revenue by type

|

|

Source: EQS Group accounts

|

Balance sheet and cash flow

Three key factors influenced the growth in the balance sheet in FY16: the consolidation of ARIVA; the acquisition of Tensid; and a capital raise in December 2016. This raised €5.2m (€5.4m gross) through the issue of 118,998 new shares at €45, with the funds earmarked to fund the group’s continued global expansion.

In FY16, EQS’s gross debt rose 11% to €9.2m (FY15: €8.3m) due to taking on the additional funding for the increase in the ARIVA holding, as well as the earlier acquisition of Obsidian IR in the UK. The increase in other liabilities is attributable to higher customer pre-payments at both Tensid and EQS, leading to absorption of working capital of €0.6m.

Net debt at the end of FY16 (post the capital raise) was €2.6m, giving gearing of 10.0% (FY15: 27.5%).

With the process of news dissemination highly automated, the regulatory information and news element of the business is particularly cash generative. This has enabled the group to demonstrate a high underlying cash conversion rate, which in turn has meant that it has effectively been able to fund its expansion programme to date through operational cash flow.

Peer valuation

We have looked at the valuation of EQS in comparison to three peer categories: global technology software companies in business services (principally US based); business-to-business media companies, principally based in Europe; and financial publishing companies (Thomson Reuters, Envestnet, Morningstar, and Dun and Bradstreet, with the addition of FactSet).

Exhibit 7: Comparison of valuation between EQS and global quoted peers

|

Agg. market cap (US$) |

|

TTM EBITDA margin |

TTM Rev growth |

EV/TTM rev (x) |

EV/TTM EBITDA (x) |

Forward EV/rev |

Forward EV/EBITDA |

Business intelligence |

2,710 |

|

13.6% |

13.5% |

3.0 |

12.2 |

2.8 |

12.0 |

Financial & accounting |

3,329 |

|

24.6% |

5.0% |

3.7 |

16.4 |

3.5 |

16 |

Vertical - finance |

6,669 |

|

34.5% |

8.5% |

4.4 |

14.0 |

4.2 |

13.6 |

Weighted software companies |

12,708 |

|

27.4% |

8.6% |

3.9 |

14.2 |

3.7 |

13.9 |

B2B media businesses |

53,966 |

|

23.1% |

12.8% |

4.6 |

17.9 |

3.3 |

12.8 |

Financial publishing companies |

46,508 |

|

27.3% |

7.4% |

3.9 |

13.8 |

3.7 |

12.6 |

EQS |

|

|

16.0% |

17.3% |

2.5 |

15.9 |

2.1 |

14.0 |

|

|

|

|

|

|

|

|

|

Discount to software comparatives (on average of relevant multiples) |

|

|

|

|

23.2% |

Discount to B2B media stocks (on average of relevant multiples) |

|

|

|

|

34.4% |

Discount to financial publishing stocks (on average of relevant multiples) |

|

|

|

|

23.0% |

Source: Bloomberg, Software Equity Group, Edison Investment Research. Note: TTM = trailing twelve months, Prices as at 4 April. 2017.

The market valuations of technology software and financial publishing companies are now broadly similar as tech valuations have retrenched. Both are now valued by the market at lower multiples than those for the B2B media stocks, which are dominated by the large exhibition companies.

All three groups, though, are trading at higher valuations than EQS, although its business model has elements common to all of them, particularly in communications and delivery mechanisms.

Obviously, EQS is less well known than the companies we are comparing it to, particularly outside its original home markets of Germany, Austria and Switzerland, with a shorter record of delivering against objectives. With less liquidity in its shares, applying a meaningful valuation discount is sensible. As shown above, when compared to average multiples of historical and prospective EV/revenue and EV/EBITDA, EQS currently trades on a 23% discount to relevant software and financial publishing stocks, and on a 34% discount to B2B media stocks.

There are a number of factors that will influence EQS’s financial performance, each of which may vary considerably across the operating territories. The three key elements of the growth strategy – digitisation, regulation and internationalisation – are themselves all important sensitivities for the future financial performance of the group, and are covered in the list of identified factors, below:

■

The number of listed companies (itself a factor of the environment for de-listings and/or IPOs).

■

The regulatory environment – the more complex the system and the greater the number and extent of changes to those systems, the greater the requirement for corporates to access relevant expertise. Introduction of additional regulation, such as the Market Abuse Regulations can breathe life back into markets that had looked dull at best.

■

Requirements for corporates to make information available in digital format, either through regulation or user demand.

■

The adoption of new channels of dissemination, such as the use of social media, where incumbents may have little expertise.

■

The relative health of corporate budgets.

■

The health of the corporate bond market.

■

Currency – the impact is obviously increasing as the group continues with its ambitions to internationalise the business. The bulk of the group overhead remains euro-denominated but revenues are increasingly generated in US dollars and US dollar-related currencies.

■

Events, such as 2015’s turbulence in Chinese markets (which led to a temporary suspension of new listings), may lead to further intervention to promote more professionalism in the market and a higher degree of institutional ownership, particularly from non-domestic investors. This could be helpful for EQS as local providers are less likely to have the relevant expertise to guide corporate clients.

Beyond these external factors, the group has internally generated sensitivities, which fall into the broad categories of system risk, personnel risk, geographic risk and acquisition risk.

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 245 Park Avenue, 39th Floor 10167, New York US |

Sydney +61 (0)2 8249 8342 Level 12, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Edison is an investment research and advisory company, with offices in North America, Europe, the Middle East and AsiaPac. The heart of Edison is our world renowned equity research platform and deep multi-sector expertise. At Edison Investment Research, our research is widely read by international investors, advisors and stakeholders. Edison Advisors leverages our core research platform to provide differentiated services including investor relations and strategic consulting. Edison is authorised and regulated by the Financial Conduct Authority. Edison Investment Research (NZ) Limited (Edison NZ) is the New Zealand subsidiary of Edison. Edison NZ is registered on the New Zealand Financial Service Providers Register (FSP number 247505) and is registered to provide wholesale and/or generic financial adviser services only. Edison Investment Research Inc (Edison US) is the US subsidiary of Edison and is regulated by the Securities and Exchange Commission. Edison Investment Research Limited (Edison Aus) [46085869] is the Australian subsidiary of Edison and is not regulated by the Australian Securities and Investment Commission. Edison Germany is a branch entity of Edison Investment Research Limited [4794244]. www.edisongroup.com DISCLAIMER

Any Information, data, analysis and opinions contained in this report do not constitute investment advice by Deutsche Börse AG or the Frankfurter Wertpapierbörse. Any investment decision should be solely based on a securities offering document or another document containing all information required to make such an investment decision, including risk factors. Copyright 2017 Edison Investment Research Limited. All rights reserved. This report has been commissioned by Deutsche Börse AG and prepared and issued by Edison for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Opinions contained in this report represent those of the research department of Edison at the time of publication. The securities described in the Investment Research may not be eligible for sale in all jurisdictions or to certain categories of investors. This research is issued in Australia by Edison Aus and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securities and Exchange Commission. Edison US relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. As such, Edison does not offer or provide personalised advice. We publish information about companies in which we believe our readers may be interested and this information reflects our sincere opinions. The information that we provide or that is derived from our website is not intended to be, and should not be construed in any manner whatsoever as, personalised advice. Also, our website and the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. This document is provided for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Edison has a restrictive policy relating to personal dealing. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report. Edison or its affiliates may perform services or solicit business from any of the companies mentioned in this report. The value of securities mentioned in this report can fall as well as rise and are subject to large and sudden swings. In addition it may be difficult or not possible to buy, sell or obtain accurate information about the value of securities mentioned in this report. Past performance is not necessarily a guide to future performance. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (ie without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision. To the maximum extent permitted by law, Edison, its affiliates and contractors, and their respective directors, officers and employees will not be liable for any loss or damage arising as a result of reliance being placed on any of the information contained in this report and do not guarantee the returns on investments in the products discussed in this publication. FTSE International Limited (“FTSE”) © FTSE 2017. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. |