Investment process: Buy good, don’t overpay, do ‘nothing’

The three building blocks of the strategy are:

1. Buy good companies: the team selects good companies with the following four characteristics:

•

Quality: high cash returns on operating capital employed;

•

Growth: driven from reinvestment of their cash flows at high rates of return;

•

Predictability: making money from a large number of everyday, small-ticket, repeat, predictable transactions; and

•

Sustainability: able to protect returns against competition.

2. Do not overpay: in terms of valuation, the team looks at the cash flow yield of a company and assesses it in the context of sustainability of the company’s competitive advantage and longevity of growth prospects. Competitive advantages could be represented by brand, market structure, distribution, logistics, regulation or scale.

3. Do nothing: FEET’s ideal holding period is ‘forever’.

The trust’s investment approach adds one extra dimension to the group’s global growth equity strategy: the companies invested in by FEET have the majority of their operations in, or revenue derived from, developing economies, providing direct exposure to the rise of the consumer classes in those countries.

Prior to the fund’s launch in 2014 the team identified about 120 companies with profiles fitting into their investment strategy. These formed the initial IU for FEET, which the team has refined to the currently maintained and regularly refreshed monitoring list of around 80 quoted businesses (the fund only invests in quoted businesses on recognised exchanges). The primary criterion for a company to remain in the universe is whether it continues to fit the remit of being a good company according to the fund managers’ investment process.

Since the handover of the fund to O’Brien and Patodia, the team has identified a growing range of investible listed opportunities that fit their criteria to broaden the portfolio beyond the direct consumer sector, but are driven by consumer themes. They have incorporated more companies from sectors outside direct consumer (staples and discretionary), particularly technology and healthcare. Backed by the house’s investment process, the managers avoid the financial sector and heavily cyclical areas such as construction and manufacturing, utilities, resources and transport, instead focusing on consumer-exposed businesses. The team may occasionally invest in IPOs.

O’Brien builds a concentrated portfolio of 35–40 holdings, with all the names coming from the IU. FEET’s mandate allows the managers to have 35–55 portfolio holdings and their target is to remain closer to the lower end of this range. As at end December 2020 the portfolio comprised 38 holdings.

Another evolution in the approach since O’Brien and Patodia took over has been the greater attention to the macroeconomic environment. The team assesses all countries eligible for the remit to evaluate their macro risks, in particular the currency risk. They also pay attention to these countries’ economic, political, social and business backdrop.

The active share has been consistently above 90%. The manager is index agnostic and buys good businesses regardless of index inclusion, believing every investee company should be a sound business on a standalone basis.

Exhibit 4 below illustrates that currently the portfolio companies’ characteristics are superior to those of the majority of MSCI EM & Frontier Markets index stocks. While FEET’s implied portfolio P/E of 37.2x is c 1.6x that of the index (22.8x), ROCE of 40% is nearly 4x that of the index. Other quality and growth ratios (gross and operating margins, free cash flow growth) also compare favourably with those of the index. If we use Fundsmith’s global portfolio (available to retail investors as the open-ended Fundsmith Equity Fund) as a proxy for global stocks, Exhibit 4 also highlights exposure to faster-growing and higher cash flow generative businesses than the global market or EM indices currently provide. FEET’s portfolio companies generate higher profits and cash flows compared to both the EM index and Fundsmith’s global portfolio.

Exhibit 4: Selected FEET portfolio metrics relative to the index and FEF

|

FEET |

MSCI EM & Frontier Markets Index |

Fundsmith Equity Fund (FEF) |

Quality |

|

|

|

ROCE |

40% |

11% |

25% |

Gross margin |

52% |

33% |

65% |

Operating margin |

18% |

11% |

23% |

Cash conversion |

93% |

82% |

101% |

Growth |

|

|

|

Free cash flow growth |

21% |

8% |

8% |

Valuation |

|

|

|

Implied P/E |

37.2x |

22.8x |

36.1x |

Free cash flow yield |

2.5% |

3.6% |

2.8% |

Portfolio dividend yield |

1.4% |

1.8% |

1.4% |

Source: Fundsmith, Edison Investment Research as at 31 December 2020.

Post the 2019 restructuring and in a steady state, the average annual portfolio turnover is likely to be fairly low. Turnover averaged c 30% between FY16 and FY20.

Corporate engagement is an integral part of the process. Before the COVID-19 pandemic, O’Brien travelled five or six weeks a year to meet companies on the ground. This year engagement with companies has shifted to online meetings and calls, with the team considering that access to companies has been excellent. About a third of the companies in which FEET may invest are quoted subsidiaries or franchisees of the multinational companies that may be held in Fundsmith Equity Fund. This helps the team to conduct due diligence and assess the corporate governance of these subsidiaries.

Governance and reporting standards are areas of careful consideration within the team’s investment process. Due diligence in corporate governance includes analysing board structure and control, whether there are differential voting rights, the ownership structure of the subsidiaries, minority rights protections, management incentivisation and the track record of managements. For example, one of the reasons the fund is less represented in China than peers is that a number of Chinese businesses fall down in the area of governance.

While Fundsmith does not dogmatically follow environmental, social and governance (ESG) approaches, the portfolios have favourable ESG characteristics, as they are composed of businesses with very strong ESG credentials. Firstly, the investment process leads the team away from investing in asset intensive businesses, which often have pollution issues (ie cement, oil and gas). Secondly, a brand element in most of FEET’s portfolio companies further strengthens their ESG credentials due to these companies’ own corporate efforts towards improving their ESG status.

FEET’s investment policy assumes the following limits of investments to gross assets:

■

5% (or 10% of up to 40% of gross assets) in a single company;

■

40% in any single country (at the time of investment);

■

20% can be in deposits held with a single bank or financial institution; and

■

20% can consist of shares and approved money market instruments or holdings in any combination of shares or deposits, issued by the same group.

The managers do not typically hedge their currency exposure.

The team believes that the closed-end structure fits well with the long-term nature of the fund. FEET’s portfolio companies are relatively illiquid and the closed-end fund structure allows the managers to maintain their conviction holding positions at times of depressed share prices, such as during the current pandemic, without being forced to sell them at a loss to fund redemptions.

Current portfolio positioning

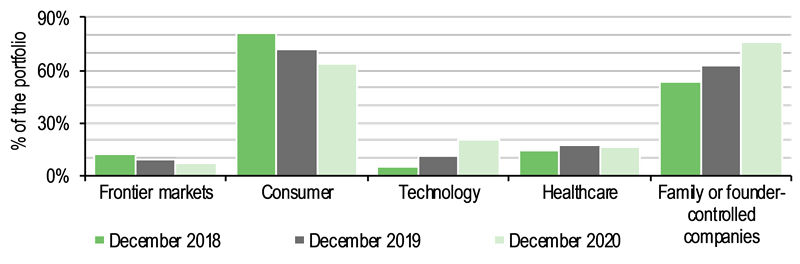

The portfolio had 38 holdings at 31 December 2020. The manager has adjusted the fund’s positioning over the past two years, making the portfolio more focused by number of holdings and more diversified by theme and sector. The number of holdings was reduced from 45 at December 2018. Exhibits 5 and 6 illustrate the transition of the portfolio by theme and sector. While frontier markets and consumer exposures have been reduced, technology, healthcare and family/founder-controlled businesses in all portfolio countries have increased.

Exhibit 5: Progress on portfolio themes in 2019 and 2020

|

Theme |

Portfolio item |

December 2018 |

December 2019 |

December 2020 |

1 |

Macro and political risk |

Frontier markets |

12% |

9% |

7% |

2 |

Sector diversity |

Consumer |

81% |

72% |

64% |

Technology |

5% |

11% |

20% |

Healthcare |

14% |

17% |

16% |

3 |

Ownership and governance |

Family or founder-controlled companies |

53% |

63% |

76% |

4 |

Portfolio concentration |

Number of holdings in the portfolio |

45 |

36 |

38 |

Source: Fundsmith, Edison Investment Research at end-December 2020

Exhibit 6: Progress on portfolio themes in 2019 and 2020

|

|

Source: Fundsmith, Edison Investment Research at end-December 2020

|

Exhibit 7 presents the portfolio by geography. Portfolio restructuring has resulted in a 4.6pp reduction of frontier markets exposure to 4.8% (at 31 December 2020), although they are still the third largest position geographically. The managers did not deliberately reduce their frontier markets exposure but sold out of companies with perceived weaker business models, and with a lesser ability to produce sustained investment returns due to the regulatory or macroeconomic risks of the countries in which they operate. India and China (including Hong Kong) remain in the top two positions, at 42.9% and 16.2%, respectively (at 31 December 2020). The managers sold two of their three South African holdings, Tiger Brands and Mr Price. Argentinian holdings were topped up by 4.3pp, while Egypt reduced by 3.4pp. Brazil’s weighting has increased 1.2pp to 4.8%.

The team primarily sold holdings in companies operating in macro and legislative environments perceived to be overly risky (even over the long term). Large currency swings, alongside the risk of potential post COVID-19 government levies over industries such as alcohol, beverages and tobacco, prompted the team to exit the exposed businesses. FEET’s exposure to these more challenged countries, including Sri Lanka, Bangladesh, Pakistan, Ghana, Nigeria, South Africa and Indonesia, has shrunk to five from 15 stocks over time. The portfolio remains radically different from the MSCI Emerging & Frontier Markets Index (Exhibit 7), as the index is not a consideration for the managers when building FEET’s portfolio. India is the largest overweight at 33.7pp, while China & Hong Kong is the largest underweight at -22.5pp. The geographic split, including being heavy in India and relatively light in China, reflects the identified IU and the manager’s bottom-up investment approach and stock selection. South Korea (index weight of 13.3%) is zero-weighted in the portfolio. The team has initiated a position in Taiwan (index weight 12.6%).

Exhibit 7: Portfolio split by geography (% unless stated) at end-December 2020

Country/region |

Portfolio weight 31 December 2020 |

Portfolio weight 31 December 2019 |

Change (pp) |

Benchmark 31 December 2020 |

Active weight vs index (pp) |

Trust/index

weight (x) |

India |

42.9 |

41.4 |

1.5 |

9.2 |

33.7 |

4.7 |

China & Hong King |

16.2 |

15.5 |

0.7 |

38.7 |

(22.5) |

0.4 |

Other Emerging Markets |

9.1 |

9.6 |

(0.5) |

14.0 |

(2.1) |

0.9 |

Argentina |

9.0 |

4.7 |

4.3 |

0.0 |

9.0 |

N/A |

Brazil |

4.8 |

3.6 |

1.2 |

5.1 |

(0.3) |

N/A |

Egypt |

4.8 |

9.4 |

(4.6) |

0.0 |

4.7 |

N/A |

Frontier Markets |

4.7 |

8.1 |

(3.4) |

7.1 |

(2.3) |

N/A |

Taiwan |

2.8 |

0.0 |

2.8 |

0.0 |

2.6 |

N/A |

Vietnam |

2.6 |

0.0 |

2.6 |

12.6 |

(12.6) |

0.0 |

South Korea |

0.0 |

0.0 |

0.0 |

13.3 |

(13.3) |

0.0 |

Philippines |

0.0 |

3.8 |

(3.8) |

0.0 |

0.0 |

|

Cash |

3.1 |

3.9 |

(0.8) |

0.0 |

3.1 |

N/A |

Total including cash |

100.0 |

100.0 |

|

100.0 |

|

|

Source: Fundsmith, Edison Investment Research. Note: end-December 2020 numbers are used, as provided by Fundsmith.

The active share is currently 93.7% (at 31 December 2020), slightly down from c 99% prior to the portfolio restructuring. The team continues to analyse some of the index constituents to see whether they develop into businesses they would be comfortable to invest in. The percentage overlap of the index with the IU is currently 13.3%, so the active share is likely to remain over 90%.

This high active share is better understood when looking at the sector split. Exhibits 8 and 9 present the split by Global Industry Classification Standard (GICS – MSCI classifications) and FEET’s defined sectors. FEET’s sector split reveals that the portfolio is concentrated within five key segments, fairly equally spread and together comprising 86% of the portfolio. These are food & beverage (25.3%), information technology (20.6%), healthcare (15.6%), fast-moving consumer goods (FMCG) (12.5%) and retail (12.1%). The team believes that categorising FEET’s sector exposure in this way allows investors to better understand the strategy and its sector/business diversification, compared to using GICS classification, where c 54% of the fund would be classified as consumer staples.

Exhibit 8: Portfolio breakdown by FEET sector*

|

Exhibit 9: Portfolio breakdown by GICS sector

|

|

|

Source: Fundsmith, Edison Investment Research. Note: Data at 31 December 2020, rebased for cash. *Based on the sector split by FEET’s team

|

Exhibit 8: Portfolio breakdown by FEET sector*

|

|

Exhibit 9: Portfolio breakdown by GICS sector

|

|

Source: Fundsmith, Edison Investment Research. Note: Data at 31 December 2020, rebased for cash. *Based on the sector split by FEET’s team

|

One of the top portfolio holdings is MercadoLibre (9.0% of the portfolio at 31 December 2020), the largest online retailer and payments business in Latin America, with a market cap of c $86bn, operating in 18 countries. Its compound revenue growth over the past five years is 37% (at September 2020). The team sees further growth potential in this retail business, as online penetration in the region grows from still-low levels. Around 5% of overall retail sales in both Mexico and Brazil are carried out online, compared with c 15% in the US and 23% in China. MercadoLibre uses cash generated by its e-commerce arm to invest into other growing business segments with high return potential. The company’s payments business serves digital sellers and also bricks-and-mortar stores. The FEET team expects to compound returns as MercadoLibre expands.

Another top 10 holding is Foshan Haitian Flavouring and Food company (8.0%), which produces and sells flavourings and food products in China. It provides soy sauce, oyster sauce, paste, vinegar, cooking wine, granulated chicken bouillon, fermented bean curd, seasoning extract, chicken powder seasoning, sesame oil, monosodium glutamate, pickle and grain products, as well as drinks and gift boxes. The company also exports its products to approximately 60 countries and regions worldwide. The FEET team expects high-paced growth and development as the company expands its product reach and offering within China and internationally.

Nestlé India (3.7%) is India’s largest standalone food company. The team describes it as a locally managed strong and growing business. Over the past 20 years its compound revenue growth rate has been around 12% pa. The company is a market leader for c 80% of the products in its portfolio, including everyday items such as noodles, instant coffee and infant cereals, with over 50% market share in all these segments. The team expects further nutritional product launches to contribute materially to the business’s growth and development, as increasingly sophisticated Indian consumers turn to quality-assured brands for their everyday food items. The company has around 200 million direct online consumers and around 40 million new consumers are added each year.

Looking at the ROCE of FEET’s top 10 holdings versus the top 10 constituents of the index (Exhibit 10), the superiority of ROCE of FEET’s investee companies is clear. The average ROCE of FEET’s top 10 holdings of 43% (31 December 2020) compares to an average of 10% for the 10 largest stocks in the index.

Exhibit 10: FEET’s top 10 holdings vs. MSCI EM top 10 constituents and their ROCE*

FEET Top 10 Company |

Country |

Industry (GICS) |

Portfolio weight % |

ROCE % |

Top 10 MSCI EM constituents Company |

Country |

Industry (GICS) |

Index weight |

ROCE % |

31-Dec-20 |

31-Dec-20 |

Mercadolibre |

US (Argentina) |

Consumer discretionary |

9.0 |

N/M** |

TSMC |

Taiwan |

Information technology |

5.8 |

27 |

Foshan Haitian |

China |

Consumer staples |

8.0 |

45 |

Alibaba |

China |

Consumer discretionary |

5.5 |

9 |

Asian Paints |

India |

Materials |

4.9 |

30 |

Tencent |

China |

Communication services |

5.3 |

18 |

Info Edge |

India |

Communication services |

4.7 |

15 |

Samsung Electronics |

South Korea |

Information technology |

4.5 |

11 |

Vitasoy |

Hong Kong |

Consumer staples |

4.4 |

24 |

Meituan Dianping |

China |

Consumer discretionary |

1.7 |

8 |

Havells |

India |

Industrials |

3.8 |

18 |

Naspers |

South Africa |

Communication services |

1.1 |

-2 |

Nestlé India |

India |

Consumer staples |

3.7 |

88 |

Reliance Industries |

India |

Energy |

1 |

10 |

Avenue Supermarkets |

India |

Consumer discretionary |

3.3 |

20 |

JD.com |

China |

Consumer discretionary |

1 |

8 |

Hindustan Unilever |

India |

Consumer staples |

3.3 |

109 |

China Construction Bank |

China |

Financials |

0.9 |

5 |

Metropolis Healthcare |

India |

Healthcare |

3.2 |

40 |

Ping An Insurance |

China |

Financials |

0.9 |

3 |

Top 10 (% of holdings) |

|

|

48.3 |

N/A |

|

|

|

27.7 |

N/A |

Average |

|

|

N/A |

43 |

|

|

|

N/A |

10 |

Source: Fundsmith Emerging Equities, Edison Investment Research, Bloomberg, MSCI. Note: *ROCE=return on capital employed; **NM – not measurable. End-December 2020 numbers are used, as provided by Fundsmith.

Since shortly after the trust’s launch, India has been and remains the largest overweight position (+33.7pp at end-December 2020) relative to the index. Seven of the top 10 holdings are Indian companies. Following the application of its four-factor analytical framework of quality, growth, predictability and sustainability of returns, the team concluded that India has a large number of some of the best companies to fit the fund’s remit. For example, the difficult operating environment, such as hard-to-set-up distribution and logistics channels, give established Indian businesses a strong competitive advantage.

The team considers the growth of e-commerce channels as a major opportunity for most portfolio companies, to enable them to grow, develop and maintain high ROCE. During the last few years, the team has reduced the number of listed FMCG companies in the portfolio, where it felt they had limited growth and return potential. Many of these were high return businesses, but in the team’s view lacked the scope for growth. Often they were replaced with businesses in sectors outside the fund’s traditional FMCG space (such as healthcare and technology), as there are far more of these businesses available for inclusion in the fund’s IU than there were in the early days of the fund, particularly those with highly developed e-commerce channels.

Following the sharp stock market corrections in March 2020, the team initiated four holdings, three in technology (XP Inc, Tencent and Taiwan Semiconductor (TSMC, bought in Q420) and one in the retail space (Lojas Renner). Two of those were acquired after material share price falls, with Tencent experiencing a more modest decline. Three were businesses familiar to the team for the last few years, while XP Inc was a 2019 IPO.

XP Inc, a business that was listed in late 2019, is the largest online investment platform for retail investors in Brazil and has a 4.5% share of the $2.1tn investment market in the country. XP has more than 1.5m retail clients on its platform (0.6% of Brazil’s population) who can invest in equity, fixed income and mutual funds. XP is 10 times larger than its nearest independent competitor in a market that is dominated by banks, and is aiming to grow its market share up to 25% between now and 2024. Only 10% of retail investment assets in Brazil are in equities, giving the group scope for growth, and the penetration level of brokerage accounts (c 1.0%) is well below that of the developed world.

Taking advantage of a sharp share price fall, the second new holding for FEET was Lojas Renner. Lojas Renner is the largest fashion retailer in Brazil, with over 600 stores. The team believes that the strength of its brand, online business and other competitive advantages will result in robust long-term growth, despite the challenging economic environment caused by COVID-19 disruptions and lockdowns. Barriers to entry are provided by a combination of consistent execution and investment in physical and digital infrastructure, all of which discourage international entrants. Efficiency is helped by having most of its supply chain within Brazil.

The third new holding, Tencent, is China’s largest social networking, gaming and music streaming company. Its social media platform (WeChat) has over 1.2 billion users, while its QQ messaging service has over 600 million users. Around the WeChat infrastructure are a number of other services such as payments, utilities, gaming, information and news. Some 98% of Chinese internet users access the internet through smartphones, supporting Tencent’s business model, which has focused on building a large user base with relatively low transaction values and a high proportion of revenues derived from subscriptions. Foreign entrants into the market are highly restricted by Chinese law. Tencent also has a strategic investment portfolio of considerable value.

The team considers TSMC – its first Taiwanese investment – as one of the best businesses it has ever come across. TSMC is the world’s largest semiconductor contract manufacturer with a market share of over 50%, which is expanding further. The managers highlight TSMC’s leading industry position, which is now an effective duopoly. It has focused on developing its own technologies in both products and the manufacturing process and has been successful in winning clients with its proposition. American and Japanese rivals have ceased developing the smaller chip sizes that TSMC manufactures and the managers believe China is several years behind in technology and implementation.

The managers believe the businesses of these new acquisitions will benefit from the trends that the COVID-19 pandemic is likely to accelerate, namely consolidation, formalisation and digitalisation. Exhibit 11 illustrates the portfolio’s large exposure to all three trends.

Exhibit 11: FEET top 15 holdings split by key investment themes

|

Consolidation |

Formalisation |

Digitalisation |

Mercadolibre |

|

|

+ |

Foshan Haitian |

+ |

+ |

|

Asian Paints |

+ |

+ |

|

Info Edge |

+ |

+ |

+ |

Vitasoy |

+ |

+ |

|

Havells |

+ |

+ |

+ |

Nestlé India |

|

+ |

+ |

Avenue Supermarts |

+ |

+ |

+ |

Hindustan Unilever |

+ |

+ |

+ |

Metropolis Healthcare |

+ |

+ |

+ |

Marico |

|

+ |

+ |

Dr Lal Pathlabs |

+ |

+ |

|

Vietnam Dairy |

+ |

+ |

|

Philippine Seven |

+ |

+ |

+ |

Godrej Consumer Products |

|

+ |

+ |

Source: Fundsmith at December 2020

Outside these purchases, the portfolio has seen little stock turnover in the year-to-date. The team exited only two stocks: Tiger Brands, a South African business, and TravelSky, a Chinese travel operator. The team initiated a position in TravelSky in 2017 as air passenger traffic was rapidly growing in China. At the time of investment, TravelSky enjoyed a government-enforced monopoly position and was a state-owned enterprise, with a combination of China’s central government and state-controlled airlines having majority control. The fund managers’ decision to exit the position in part reflected TravelSky allocating capital outside of the business, most notably setting up joint ventures in the insurance and telecom sectors.

The investment case for Tiger Brands was no longer there for O’Brien, as he believed the company’s management had lost their grip on the business. Also, the manager trimmed a few holdings of companies exposed to those countries that the team does not expect to recover in the short term from the adverse impact of reduced foreign worker remittances into the countries of operation, particularly in Asia.

over three years (%)")